The forex markets are rather quiet in Asian session today. Trading will probably remain subdued with US on holiday. The greenback remains the strongest one for the week on speculation that the “transitory” yet persistent strong inflation would eventually force Fed to raise interest rate earlier. Canadian Dollar is currently the second strongest for the week, as WTI oil price stabilized above 75 handle. New Zealand Dollar remains the worst performing one, with Yen a distant second.

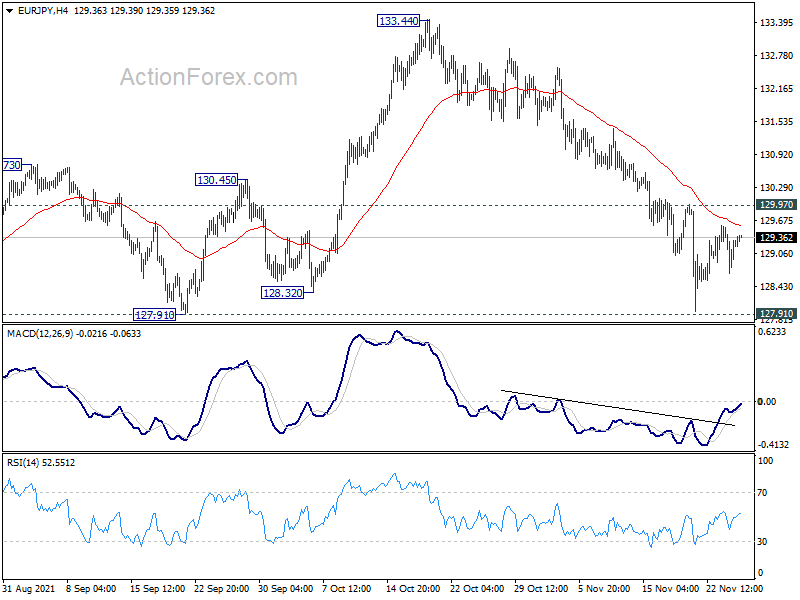

Technically, the next move in Sterling could be interesting, as both EUR/GBP and GBP/JPY are stuck in range, with near term bearish bias. That is both are in favor to extend recent decline, which is contrasting each other. But, downside breakout in both EUR/GBP and GBP/JPY would make sense, if that is also accompanied by EUR/JPY’s sharp fall through 127.91 near term support. We’ll see.

{kind=link}

In Asia, Nikkei rose 0.77%. Hong Kong HSI is up 0.22%. China Shanghai SSE is down -0.08%. Singapore Strait Times is down -0.09%. Japan 10-year JGB yield is down -0.0024 at 0.084. Overnight, DOW dropped -0.03%. S&P 500 rose 0.23%. NASDAQ rose 0.44%. 10-year yield dropped -0.0022 to 1.645.

Fed minutes: No hesitate to take actions to address inflation risks

In the minutes of November 2-3 FOMC meeting, various participants noted that the Committee should be prepared to “adjust the pace of asset purchases and raise the target range for the federal funds rate sooner than participants currently anticipated” if inflation continued to run higher than levels consistent with the Committee’s objectives. ”

At the same time, because of the continuing considerable uncertainty about developments in supply chains, production logistics, and the course of the virus, a number of participants stressed that a “patient attitude toward incoming data remained appropriate to allow for careful evaluation of evolving supply chain developments and their implications for the labor market and inflation.”

“That said, participants noted that the Committee would not hesitate to take appropriate actions to address inflation pressures that posed risks to its longer-run price stability and employment objectives.”

New Zealand imports rose 12% yoy in Oct, imports rose 26% yoy

New Zealand goods exports rose 12% yoy to NZD 5.3B in October. Goods imports rose 26% yoy to NZD 6.6B. Trade deficit came in at NZD -1.3B, versus expectation of NZD -1.6B.

Exports to China was up 20%, Australia down -6.5%, USA up 12%, Japan 30%, EU up 11%. Imports from China rose 29%, EU up 33%, Australia up 7.5%, USD up 13%, Japan up 52%.

Japan corporate service price rose 1% yoy to highest since 2001

Japan corporate service price index rose 1.0% yoy in October, slightly above expectation of 0.9% yoy. At 105.4, the services producer price index hit the highest level since November 2001. The key driver of the rise was transportation fee, with cost of ocean freight transportation up 52.0% yoy.

“Corporate services prices are recovering gradually, with some sectors showing demand picking up due to the lifting of curbs. But the move hasn’t broadened much on lingering caution over the pandemic,” Shigeru Shimizu, head of the BOJ’s price statistics division, told a briefing.

Looking ahead

Germany Gfk consumer sentiment and Q3 GDP final will be released in European session. ECB will also publish monetary policy meeting accounts.

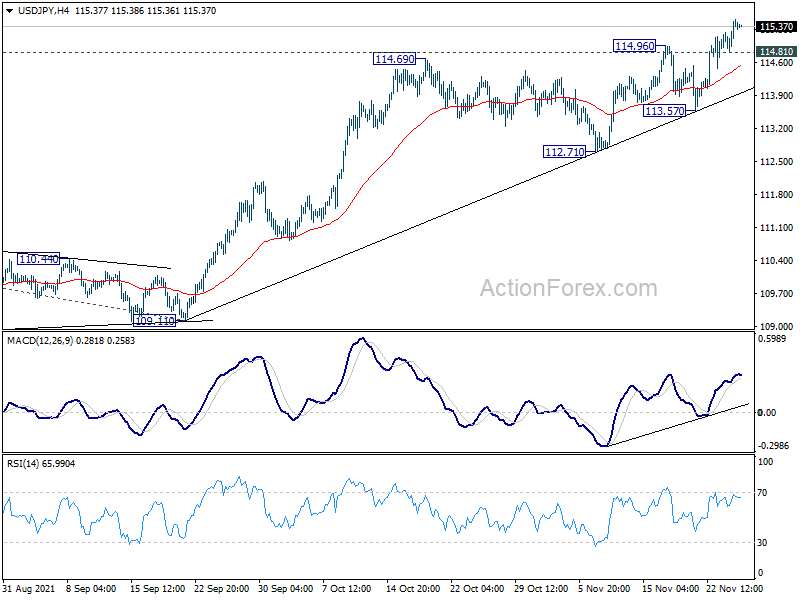

USD/JPY Daily Outlook

Daily Pivots: (S1) 114.99; (P) 115.26; (R1) 115.68; More…

Intraday bias in USD/JPY remains on the upside for the moment. Current up trend from 102.58 should target 100% projection of 102.58 to 111.65 from 109.11 at 118.18 next. On the downside, below 114.81 minor support will turn intraday bias neutral first. But break of 113.57 support is needed to indicate short term topping. Otherwise, outlook will stay bullish in case of retreat.

{kind=link}

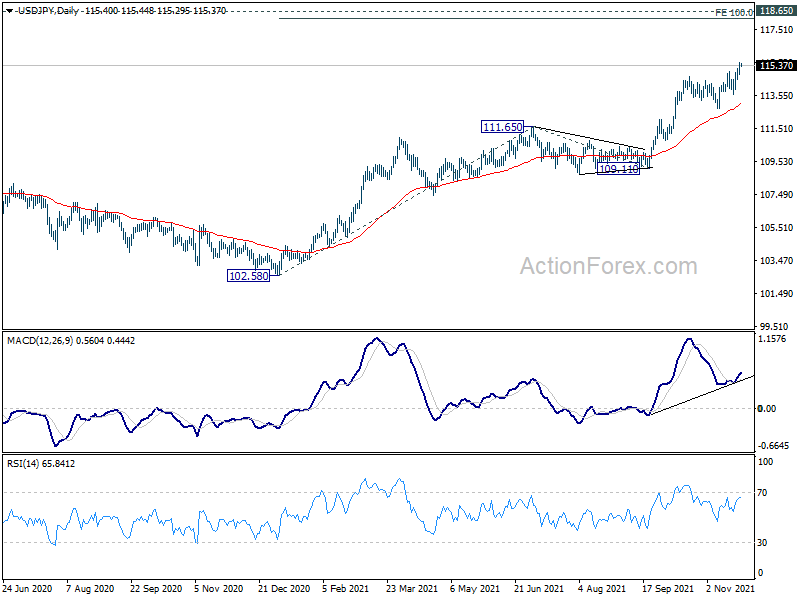

In the bigger picture, corrective decline from 118.65 (2016 high) should have completed at 101.18 already. Rise from the 102.58 is seen as the third leg of the up trend from 101.18. Next target is 118.65 high. This will now be the preferred case as long as 111.65 resistance turned support holds, even in case of deep pull back.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Oct | -1286M | -1575M | -2171M | -2206M |

| 23:50 | JPY | Corporate Service Price Index Y/Y Oct | 1.00% | 0.90% | 0.90% | |

| 00:30 | AUD | Private Capital Expenditure Q3 | -2.20% | -2.00% | 4.40% | 3.40% |

| 07:00 | EUR | Germany Gfk Consumer Confidence Dec | -0.3 | 0.9 | ||

| 07:00 | EUR | Germany GDP Q/Q Q3 F | 1.80% | 1.80% | ||

| 12:30 | EUR | ECB Monetary Policy Meeting Accounts |