Dollar’s rally continues today and stays firm after much better than expected jobless claims data. Yen is following as second strongest on risk-off sentiment, as major European indexes and US futures are in red. On the other hand, New Zealand Dollar remains the worst performing one on post-RBNZ selloff, Aussie and Loonie are following.

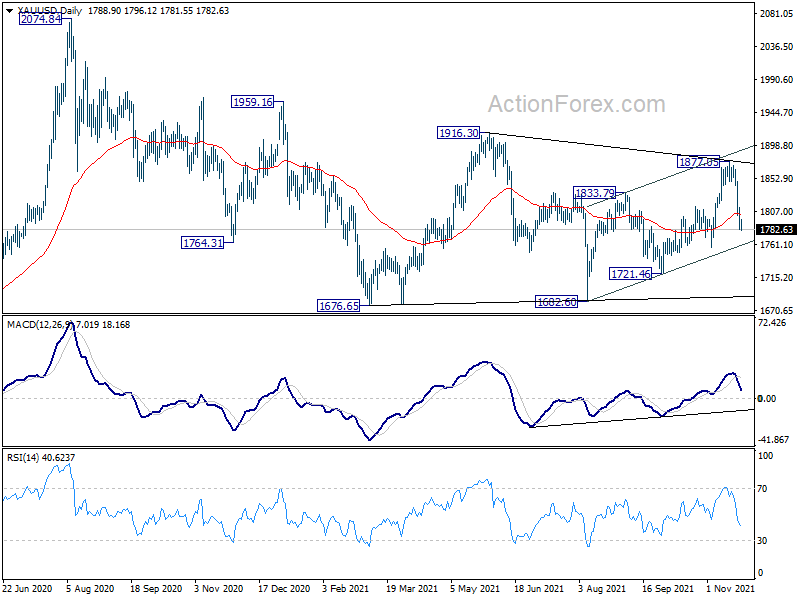

Technically, we’d keep an eye on Gold’s development. Fall from 1877.05 is in progress and sustained break of channel support (now at 1762.19) could bring deeper fall back to 1700 handle (just above 1676.65/1682.60 support zone). Such decline would also come with intensified buying in Dollar, in particular against Euro.

{kind=link}

In Europe, at the time of writing, FTSE is down -0.21%. DAX is down -1.11%. CAC is down -0.82%. Germany 10-year yield is up 0.0163 at -0.203. Earlier in Asia, Nikkei dropped -1.58%. Hong Kong HSI rose 0.14%. China Shanghai SSE rose 0.10%. Singapore Strait Times dropped -0.01%. Japan 10-year JGB yield rose 0.0012 to 0.086.

US initial jobless claims dropped to 199k, lowest since 1969

US initial jobless claims dropped -71k to 199k in the week ending November 20, well below expectation of 260k. That;s the lowest level since November 15, 1969. Four-week moving average of initial claims dropped -21k to 252k, lowest since March 14, 2020.

Continuing claims dropped -60k to 2049k in the week ending November 13, lowest since March 2020. Four-week moving average of continuing claims dropped -48k to 2117k, lowest since march 21, 2020.

US Q3 GDP growth revised slightly up to 2.1% annualized

According to the second estimate, US real GDP grew at annualized rate of 2.1% in Q3, comparing to Q2’s 6.7%. The upward revision from advance estimate of 2.0% primarily reflects upward revisions to personal consumption expenditures (PCE) and private inventory investment.

US durable goods orders dropped -0.5% in Oct, ex-transport orders rose 0.5%

US durable goods orders dropped -0.5%to USD 260.1B in October, below expectation of 0.2%. Ex-transport orders rose 0.5%, matched expectations. Ex-defense orders rose 0.8%. Transportation equipment dropped -2.6% to USD 75.3B.

Goods trade deficit narrowed to USD -82.9B in October, versus expectation of USD -94.7B.

ECB Panetta: Monetary policy should remain patient

ECB Executive Board member Fabio Panetta said, “the data suggest the current picture is dominated by a bout of ‘bad’ inflation generated outside the euro area, whereas we are far from seeing abnormally large domestic demand.” “Monetary policy should remain patient. A premature tightening would restrain spending before demand has returned to trend,” he added.

“We should not exacerbate the risk of supply shocks morphing into a demand shock and threatening the recovery by prematurely tightening monetary policy – or by passively tolerating an undesirable tightening in financing conditions,” Panetta warned.

Panetta also urged to continue with asset purchases. “First, the surge in the number of (COVID-19) infections and the renewed introduction of pandemic-related restrictions in some euro area countries mean that the pandemic is not over yet,” he said. “Second, an inappropriate, sharp reduction of purchases would be tantamount to a tightening of the policy stance.”

Separately, Governing Council member Robert Holzmann said, “the statements until now including of my colleagues on the Governing Council all suggest that net PEPP purchases will probably expire in March but that PEPP as such will not be done away with but perhaps be put in a waiting room.”

This will be in order to “save the advantages of flexibility in case they become necessary in the event of economic shocks, which are definitely possible, but we do not expect,” Holzmann said.

Germany Ifo dropped to 96.5, challenged by supply bottlenecks and 4th wave of coronavirus

Germany Ifo Business Climate dropped to 96.5 in November, down form 97.7, missed expectation of 96.7. Current Assessment index dropped to 99.0, down from 100.2, missed expectation of 100.3. Expectations index dropped to 94.2, down from 95.4, missed expectation of 96.3.

By sector, manufacturing dropped from 17.5 to 16.5. Service dropped sharply again from 16.6 to 11.5. Trade dropped from 3.7 to 2.6. Construction dropped from 12.8 to 12.0.

Ifo said: “Companies were less satisfied with their current business situation, and expectations became more pessimistic. Supply bottlenecks and the fourth wave of the coronavirus are challenging German companies.”

From Swiss, Credit Suisse Economic Expectations tumbled sharply from 15.6 to -10.8 in November.

RBNZ hikes OCR to 0.75%, maintains hawkish bias

RBNZ raised the Official Cash Rate to by 25bps to 0.75% as expected. It also maintained a hawkish bias, noting that ” further removal of monetary policy stimulus is expected over time given the medium term outlook for inflation and employment.”

The central bank also said that despite recent nationwide lockdown, “underlying economic strength remains supported by aggregate household and business balance sheet strength, fiscal policy support, and strong export returns.” Capacity pressured have “continued to tighten” with employment “above its sustainable level”. A broad range of economic indicators highlight the economy “continues to perform above its current level”.

Headline CPI is expected to be “above 5 percent in the near term” before returning towards 2% midpoint “over the next two years.

Japan PMI manufacturing rose to 54.2, services rose to 52.1

Japan PMI Manufacturing rose to 54.2 in November, up from 53.2, but missed expectation of 54.5. PMI Services rose to 52.1, up from 50.7. PMI Composite rose to 52.5, up from 50.7.

Usamah Bhatti, Economist at IHS Markit, said:

“Flash PMI data indicated that activity at Japanese private sector businesses rose for the second month running in November. Growth in output quickened from October and was the quickest recorded since October 2018. By sector, service providers noted the sharpest rise in activity since September 2019, while manufacturers indicated the fastest rate of growth for six months.

“Firms across the Japanese private sector reported intensifying price pressures. Input prices across the private sector rose at the fastest pace for over 13 years with businesses attributing the rise to higher raw material, freight and staff costs amid shortages and deteriorating supplier performance.

“As vaccination rates rose and economic restrictions eased, Japanese private sector companies were strongly optimistic that business activity would rise in the year ahead. Positive sentiment was the strongest on record and stemmed from hopes that the end of the pandemic and lifting of international restrictions would provide a broad-based boost to activity.”

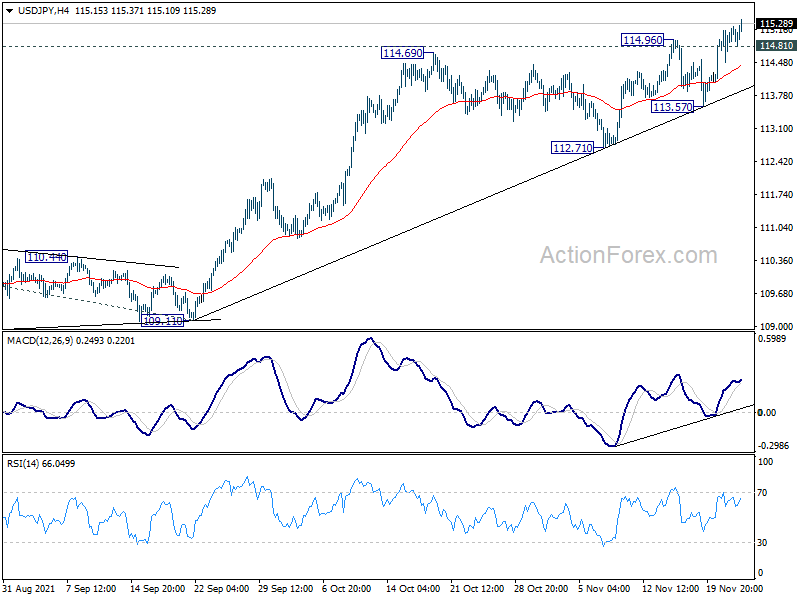

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 114.69; (P) 114.93; (R1) 115.37; More…

USD/JPY’s rally continues today and intraday bias remains on the upside. Current up trend from 102.58 should target 100% projection of 102.58 to 111.65 from 109.11 at 118.18 next. On the downside, below 114.81 minor support will turn intraday bias neutral first. But break of 113.57 support is needed to indicate short term topping. Otherwise, outlook will stay bullish in case of retreat.

{kind=link}

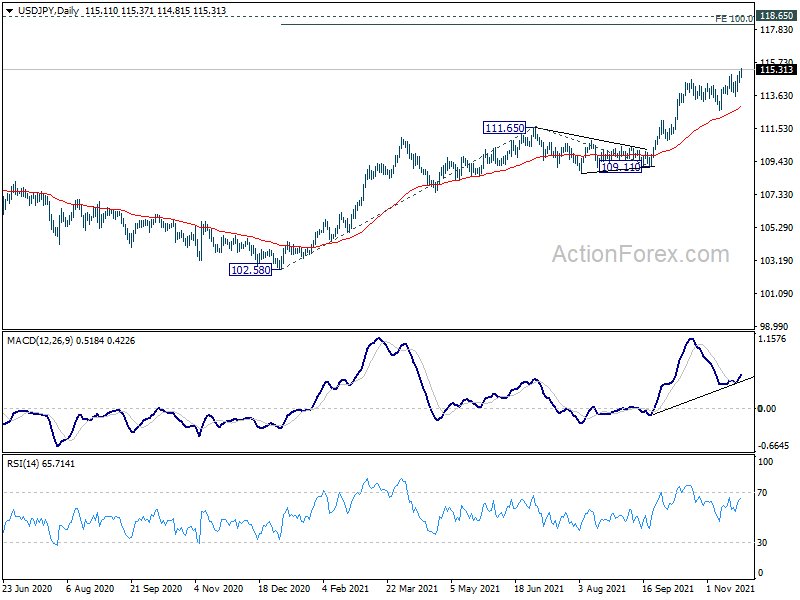

In the bigger picture, corrective decline from 118.65 (2016 high) should have completed at 101.18 already. Rise from the 102.58 is seen as the third leg of the up trend from 101.18. Next target is 118.65 high. This will now be the preferred case as long as 111.65 resistance turned support holds, even in case of deep pull back.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Construction Work Done Q3 | -0.30% | -3.10% | 0.80% | 2.20% |

| 00:30 | JPY | Manufacturing PMI Nov P | 54.2 | 54.5 | 53.2 | |

| 00:40 | AUD | RBA’s Bullock speech | ||||

| 01:00 | NZD | RBNZ Interest Rate Decision | 0.75% | 0.75% | 0.50% | |

| 02:00 | NZD | RBNZ Press Conference | ||||

| 09:00 | CHF | Credit Suisse Economic Expectations Nov | -10.8 | 15.6 | ||

| 09:00 | EUR | Germany IFO Business Climate Nov | 96.5 | 96.7 | 97.7 | |

| 09:00 | EUR | Germany IFO Current Assessment Nov | 99 | 100.3 | 100.1 | 100.2 |

| 09:00 | EUR | Germany IFO Expectations Nov | 94.2 | 96.3 | 95.4 | |

| 13:30 | USD | Initial Jobless Claims (Nov 19) | 199K | 260K | 268K | 270K |

| 13:30 | USD | GDP Annualized Q3 P | 2.10% | 2.20% | 2.00% | |

| 13:30 | USD | GDP Price Index Q3 P | 5.90% | 5.70% | 5.70% | |

| 13:30 | USD | Goods Trade Balance (USD) Oct P | -82.9B | -94.7B | -96.3B | |

| 13:30 | USD | Wholesale Inventories Oct P | 2.20% | 1.20% | 1.40% | |

| 13:30 | USD | Durable Goods Orders Oct | -0.50% | 0.20% | -0.30% | |

| 13:30 | USD | Durable Goods Orders ex Transportation Oct | 0.50% | 0.50% | 0.50% | |

| 15:00 | USD | Personal Income M/M Oct | 0.30% | -1.00% | ||

| 15:00 | USD | Personal Spending Oct | 0.90% | 0.60% | ||

| 15:00 | USD | PCE Price Index M/M Oct | 0.40% | 0.30% | ||

| 15:00 | USD | PCE Price Index Y/Y Oct | 4.60% | 4.40% | ||

| 15:00 | USD | Core PCE Price Index M/M Oct | 0.40% | 0.20% | ||

| 15:00 | USD | Core PCE Price Index Y/Y Oct | 4.10% | 3.60% | ||

| 15:00 | USD | New Home Sales Oct | 801K | 800K | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Nov F | 66.8 | 66.8 | ||

| 15:30 | USD | Crude Oil Inventories | -1.7M | -2.1M | ||

| 17:00 | USD | Natural Gas Storage | -23B | 26B | ||

| 19:00 | USD | FOMC Minutes |