New Zealand Dollar trades mildly higher today, after an RBNZ survey shows firm expectation of more rate hike ahead. On the other hand, Canadian Dollar weakens broadly as WTI crude oil’s pull back extends below a near term support level. Overall, Sterling and Dollar remain the strongest ones for the week. Euro is recovering slightly but remains the worst weekly performer, followed by Aussie.

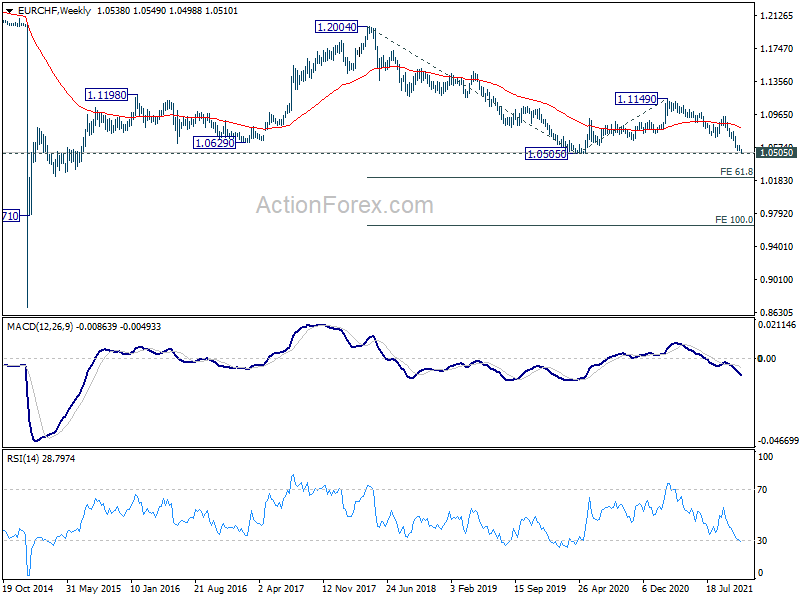

Technically, major focus remains on 1.1289 long term fibonacci support in EUR/USD. Sustained break of this will carry larger bearish implication and would bring even deeper down trend to 1.0635 (2020 low). At the same time, EUR/CHF is also pressing 1.0505 low. Sustained break there will resume the larger down trend from 1.2004 to 61.8% projection of 1.2004 to 1.0505 to 1.1149 at 1.0223 next. We’ll see if Euro’s selloff would intensify ahead, or rebound from here.

{kind=link}

In Asia, at the time of writing, Nikkei is down -0.80%. Hong Kong HSI is down -1.44%. China Shanghai SSE is down -0.33%. Singapore Strait Times is up 0.06%. Japan 10-year JGB yield is up 0.0006 at 0.075. Overnight, DOW dropped -0.58%. S&P 500 dropped -0.26%. NASDAQ dropped -0.33%. 10-year yield dropped -0.030 to 1.604.

RBNZ survey: Four rate hikes over next seven meetings

In the latest RBNZ survey for Q4, 2-year ahead inflation expectations rose from 2.27% to 2.96%, highest since June 2011. 5-year inflation inflation expectation rose from 2.03 to 2.17%, highest since September 2017.

Currently, the OCR is standing at 0.50%, after a rate hike of 25bps in October 6. Survey respondents expect Oct. to rise further to 0.75% by the end of the current quarter. Mean estimate for OCR one year ahead was 1.53%, translating to four 25bps hike over the next seven RBNZ meetings. Two year-head expectations stands at 1.83%, with more respondents expecting OCR to be either at 1.50% or 2.0)% by the end of September 2023.

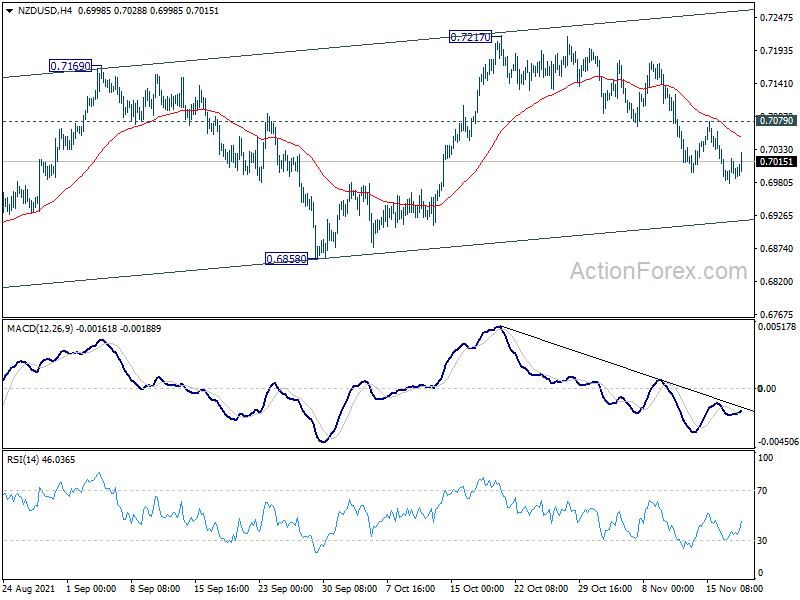

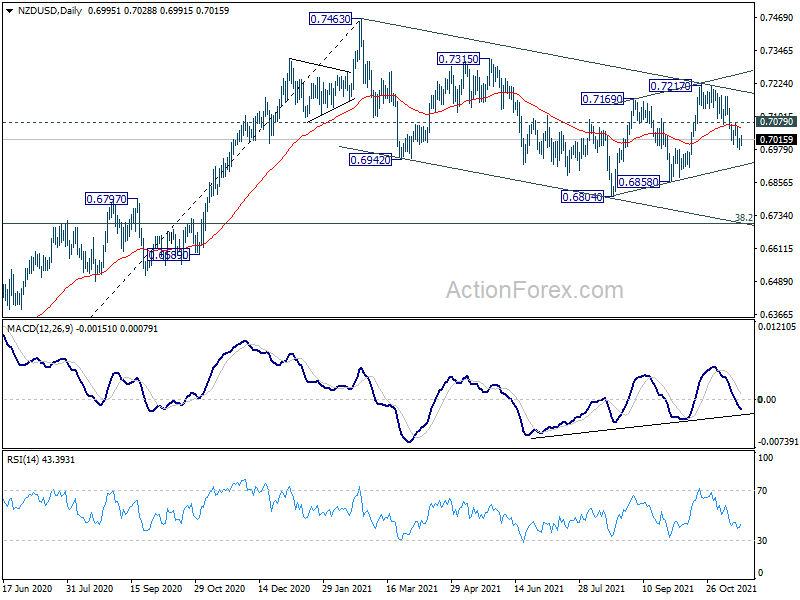

NZD/USD recovers mildly, but outlook stays bearish

NZD/USD recovers mildly today but overall outlook is unchanged. Further decline will remain in favor as long as 0.7079 minor resistance holds. Current development suggests that rebound from 0.6804 is complete with three waves up to 0.7217. In other words, larger decline from 0.7463 is not over.

Fall from 0.7271 should target 0.6858 support next. Firm break there will solidify this bearish case, and extend the corrective pattern from 0.7463 through 0.6804 low, to 38.2% retracement of 0.5467 to 0.7463 at 0.6701.

{kind=link}

{kind=link}

Fed Evans: Going to take us until the middle of next year to complete tapering

Chicago Fed President Charles Evans said in a virtual conference, “we learned back in 2013 that tapering these asset purchases was preferable for financial market functioning; that if we did a sudden stop on our purchases that wasn’t well received. It’s going to take us until the middle of next year to complete that”.

“It’s going to take us until the middle of next year to complete that; we are going to be mindful of inflation; we’re going to be looking to see how much additional accommodation is boosting inflation; if indeed that is the case, we’ll be thinking about when the right time to start raising rates will be,” he added.

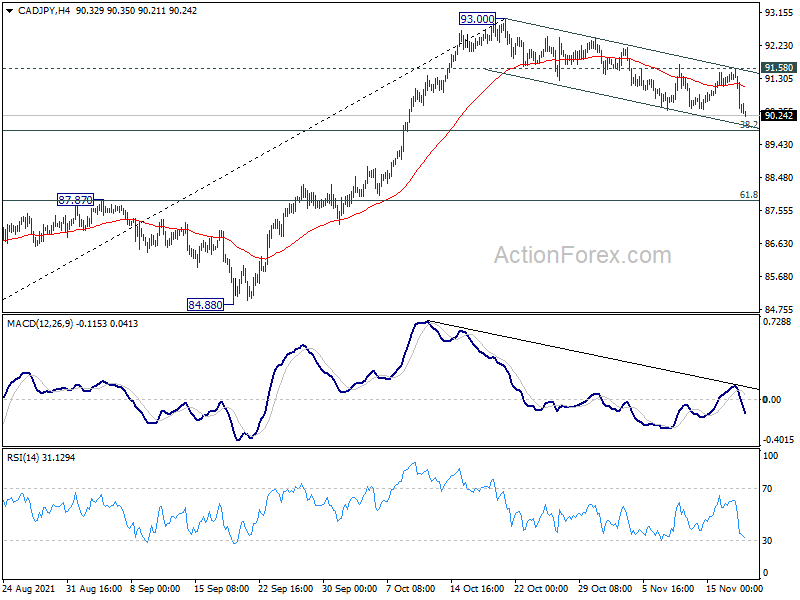

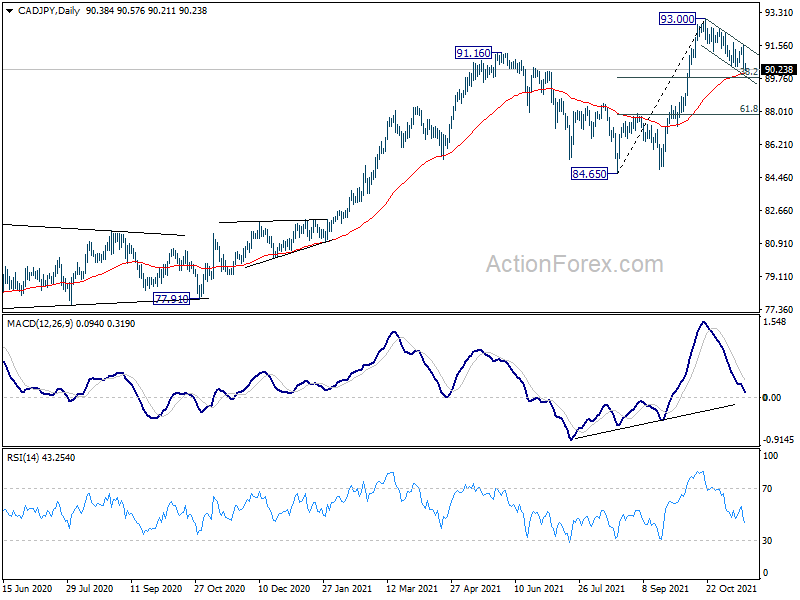

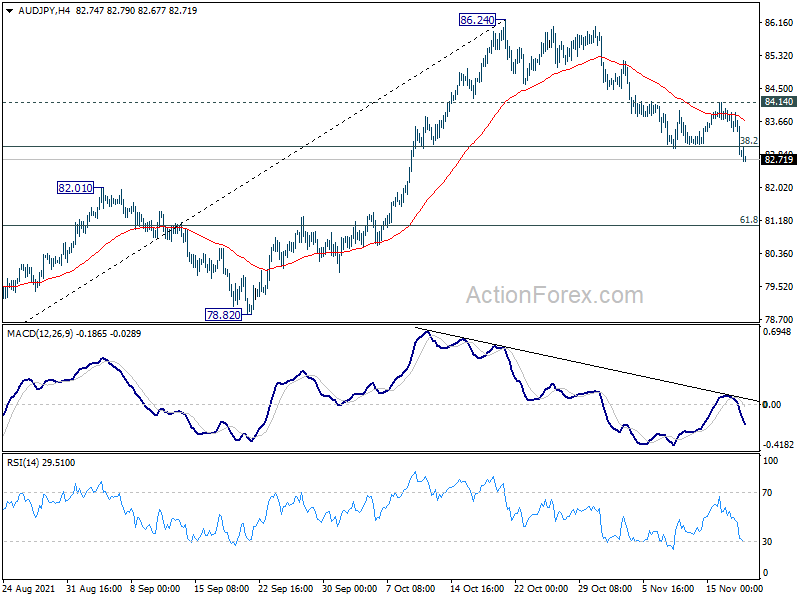

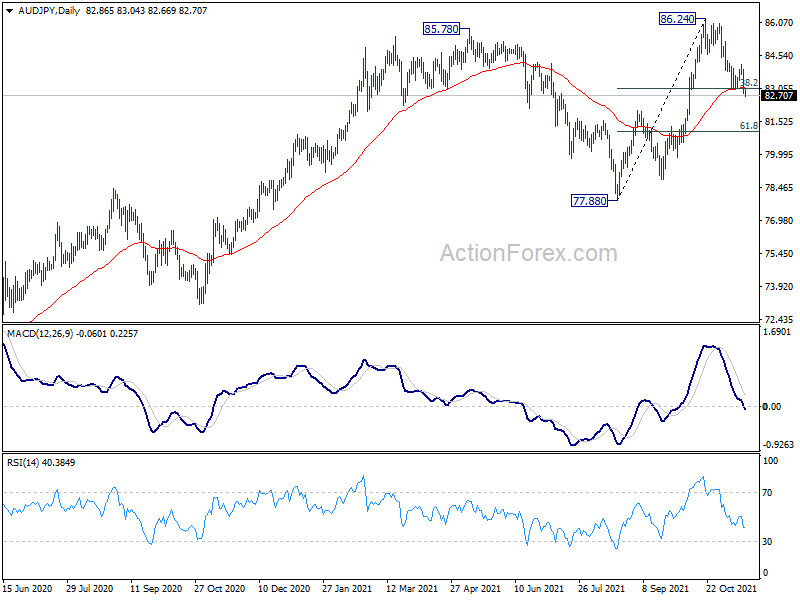

CAD/JPY and AUD/JPY resume corrective decline

Following the pullback in US stocks overnight, Yen crosses are trading generally lower. In particular, CAD/JPY resumed the decline from 93.00 by breaking through 90.40 temporary low. Judging from the development in Yen pairs elsewhere, there is prospect of deeper decline even if such fall is still a corrective more.

For now, further decline is expected in CAD/JPY as long as 91.58 minor resistance holds. 38.2% retracement of 84.65 to 93.00 at 89.81 might provide some initial support. But firm break there will bring deeper fall to 61.8% retracement at 87.83.

{kind=link}

{kind=link}

Development in AUD/JPY is slightly more bearish, as 55 day EMA and 38.2% retracement of 77.88 to 86.24 at 83.04 are both taken out. Fall from 86.24 has just resumed. Deeper decline is expected as long as 84.14 resistance holds, for 61.8% retracement at 81.07 and possibly below.

{kind=link}

{kind=link}

Swiss trade balance will be released in European session. Later in the day, Canada will release ADP employment and foreign securities purchases. US will release jobless claims and Philly Fed survey.

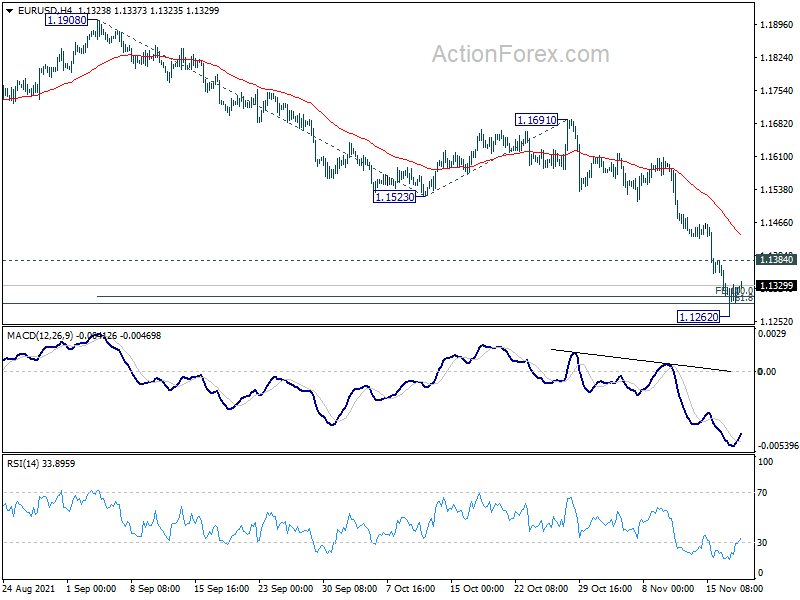

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1281; (P) 1.1306; (R1) 1.1349; More…

Intraday bias in EUR/USD is turned neutral first as it recovered after hitting 1.1262. Focus remains on 1.1289 long term fibonacci level. Sustained break there will carry larger bearish implication, and extend the fall from 1.2348 to 161.8% projection of 1.1908 to 1.1523 from 1.1691 at 1.1068. On the upside, above 1.1384 indicate short term bottoming and turn bias back to the upside for stronger rebound.

{kind=link}

In the bigger picture, there are various ways of interpreting the fall from 1.2348 (2021 high). It could be a correction to rise from 1.0635 (2020 low), the fourth leg of a sideway pattern from 1.0339 (2017 low), or resuming long term down trend. In any case, outlook will now stay bearish as long as 1.1703 support turned resistance holds. Sustained break of 61.8% retracement of 1.0635 to 1.2348 at 1.1289 would pave the way back to 1.0635.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 02:00 | NZD | RBNZ Inflation Expectations Q4 | 2.96% | 2.27% | ||

| 07:00 | CHF | Trade Balance(CHF) Oct | 4.90B | 5.05B | ||

| 13:30 | CAD | ADP Employment Change Oct | 9.6K | |||

| 13:30 | CAD | Foreign Securities Purchases (CAD) Sep | 20.05B | 26.30B | ||

| 13:30 | USD | Initial Jobless Claims (Nov 12) | 260K | 267K | ||

| 13:30 | USD | Philadelphia Fed Manufacturing Nov | 21.5 | 23.8 | ||

| 15:30 | USD | Natural Gas Storage | 25B | 7B |