Dollar is trying to rebound broadly in early US session, partly on strong inflation data, and partly on month end flow. But overall, the greenback is just mixed for the week. For week Aussie and Swiss Franc are the strongest ones, with the latter lifted by strong buying against Euro. Yen is now the weakest one and will likely remain so. Euro and Canadian Dollar are both weak too as respective central bank meeting didn’t produce sustainable buying in them.

In Europe, at the time of writing, FTSE is down -0.32%. DAC is down -0.53%. CAC is down -0.24%. Germany 10-year yield is up 0.0512 at -0.080. Earlier in Asia, Nikkei rose 0.25%. Hong Kong HSI dropped -0.70%. China Shanghai SSE rose 0.82%. Singapore Strait Times dropped -0.18%. Japan 10-year JGB yield rose 0.0114 to 0.100.

US personal income dropped -1.0% mom in Sep, spending rose 0.6% mom

US personal income dropped -1.0% mom or USD 216.2B in September, much worse than expectation of 0.1% mom rise. Personal spending rose 0.6% mom or USD 93.4B, matched expectations. Headline PCE inflation accelerated to 4.4% yoy, below expectation of 4.7% yoy. Core PCE price index was unchanged at 3.6% yoy, below expectation of 3.7% yoy.

Canada GDP grew 0.4% mom in Aug, to be flat in Sep

Canada GDP rose 0.4% mom in August, below expectation of 0.7% mom. Overall 15 of 20 industrial sectors were up. Services-producing industries rose 0.6%. Goods-producing industries dropped -0.1% Preliminary information suggests that real GDP was essentially unchanged in September. Advance estimate points to an approximate 0.5% rise in real GDP in Q3.

Eurozone CPI surged to 4.1% yoy in Oct, highest since 2008

Eurozone CPI surged to 4.1% yoy in October, up from 3.4% yoy, above expectation of 3.7% yoy. That’s also the fastest pace since July 2008. CPI core rose to 2.1% yoy, up from 1.9% yoy, above expectation of 1.9% yoy.

Looking at the main components, energy is expected to have the highest annual rate in October (23.5%, compared with 17.6% in September), followed by services (2.1%, compared with 1.7% in September), non-energy industrial goods (2.0%, compared with 2.1% in September) and food, alcohol & tobacco (2.0%, stable compared with September).

Eurozone GDP grew 2.2% qoq in Q3, EU up 2.1% qoq

Eurozone GDP grew 2.2% qoq in Q3, slightly above expectation of 2.1% qoq. EU GDP grew 2.1% qoq. Among the EU Member States for which data are available, Austria (+3.3%) recorded the highest increase compared to the previous quarter, followed by France (+3.0%) and Portugal (+2.9%). The lowest growth was recorded in Latvia (+0.3%) and GDP was stable in Lithuania (0.0%). The year on year growth rates were positive for all countries.

Germany GDP grew only 1.8% qoq in Q2, below expectation of 2.2% qoq. Overall GDP was still -1.1% lower (price-, seasonally and calendar-adjusted) than in the fourth quarter of 2019, the quarter before the coronavirus crisis began.

France GDP rose 3.0% qoq in Q3, above expectation of 2.4% qoq. GDP has almost returned to pre-crisis level, just -0.1% below Q4 2019 level.

Italy GDP grew 2.6% qoq, below expectation of 2.0% qoq.

Swiss KOF dropped slightly to 110.7, almost unchanged overall movement

Swiss KOF Economic Barometer dropped slightly from 111.0 to 110.7 in October, better than expectation of 108.0. KOF said: “Indicator bundles of the food and beverage industry have improved clearly and are contrasted by declines in indicator bundles of manufacturing, the economic sector other services, foreign demand and the financial and insurance services, resulting in an almost unchanged overall movement.”

Japan industrial production dropped -5.4% mom in Sep, but expected to bounce back strongly ahead

Japan industrial production dropped sharply by -5.4% mom in September, much worse than expectation of -2.4% mom. The seasonally adjusted index of production at factories and mines dropped for the third straight month to 89.5, against the 2015 100 base of 100.

But looking ahead, the Ministry of Economy, Trade and Industry said output would bounce back by 6.4% in October, and then 5.7% in November, based on a poll of manufacturers. An official said, “output may have hit bottom in September since economic activities have been returning to normal in countries such as Vietnam and Malaysia since late September, and a recovery is expected, mainly in the auto industry.”

Also released, unemployment was unchanged at 2.8% in September, matched expectations. Housing starts rose 4.3% yoy, versus expectation of 7.5% yoy. Consumer confidence dropped to 39.2, below expectation of 40.4. In October, Tokyo CPI core was unchanged at 0.10% yoy, below expectation of 0.3% yoy.

Australia retail sales rose 1.3% mom in Sep, vary by state

Australia retail sales rose 1.3% mom in September, much better than expectation of 0.2% mom. That’s the first monthly growth since May. For the 12-month, sales rose 1.7% yoy.

“Retail turnover continues to vary by state, based on whether restrictions were imposed, removed or extended. Queensland sales rose to their highest level ever, up 5.2 per cent, with no lockdowns in September,” Ben James, Director of Quarterly Economy Wide Statistics said.

“New South Wales also experienced a rise of 2.3 per cent despite having lockdowns, as some restrictions were eased or lifted. However, turnover for New South Wales remains 11.9 per cent lower than May 2021, the month before the most recent lockdown began.”

Also released, PPI came in at 1.1% qoq, 2.9% qoq in Q3, versus expectation of 0.6% qoq, 3.2% yoy. Price sector credit rose 0.6% mom in September, matched expectations.

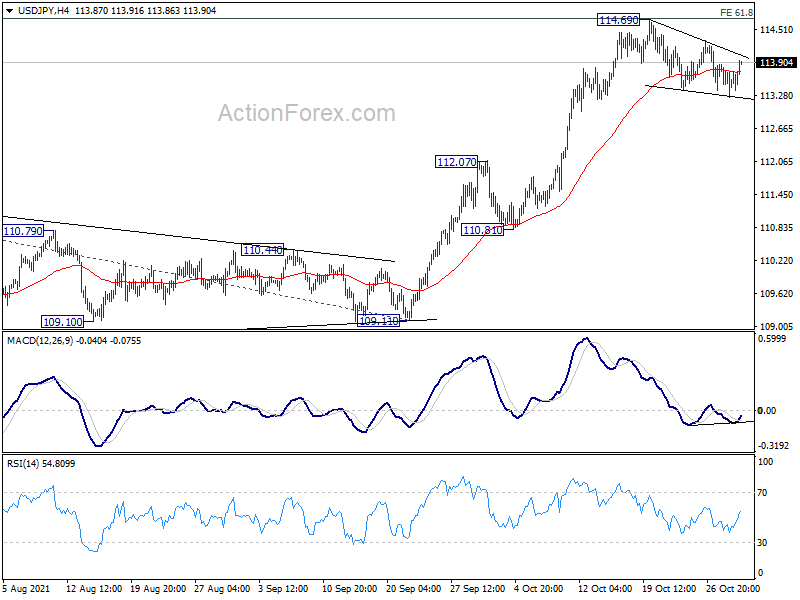

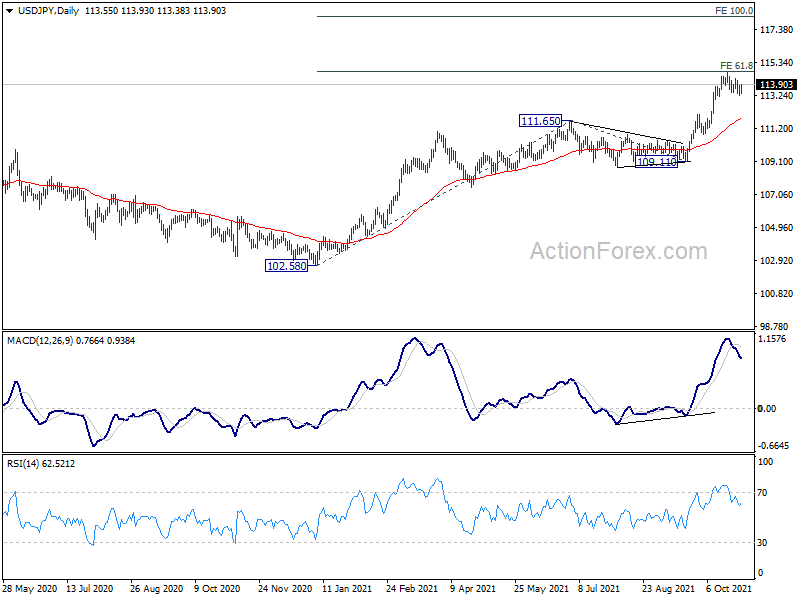

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.25; (P) 113.56; (R1) 113.86; More…

Intraday bias in USD/JPY is turned neutral again with current recovery. Corrective pattern from 114.69 might extend, but downside should be contained above 112.07 resistance turned support to bring rebound. On the upside, firm break of 114.69 will resume the larger up trend to 100% projection of 102.58 to 111.65 from 109.11 at 118.18 next.

{kind=link}

In the bigger picture, corrective decline from 118.65 (2016 high) should have completed at 101.18 already. Rise from the 102.58 is seen as the third leg of the up trend from 101.18. Next target is 114.54 resistance and then 118.65 high. This will now be the preferred case as long as 109.11 support hold, even in case of deep pull back.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Oct | 0.10% | 0.30% | 0.10% | |

| 23:30 | JPY | Unemployment Rate Sep | 2.80% | 2.80% | 2.80% | |

| 23:50 | JPY | Industrial Production M/M Sep P | -5.40% | -2.40% | -3.60% | |

| 00:30 | AUD | Private Sector Credit M/M Sep | 0.60% | 0.60% | 0.60% | |

| 00:30 | AUD | Retail Sales M/M Sep | 1.30% | 0.20% | -1.70% | |

| 00:30 | AUD | PPI Q/Q Q3 | 1.10% | 0.60% | 0.70% | |

| 00:30 | AUD | PPI Y/Y Q3 | 2.90% | 3.20% | 2.20% | |

| 05:00 | JPY | Housing Starts Y/Y Sep | 4.30% | 7.50% | 7.50% | |

| 05:30 | EUR | France Consumer Spending M/M Sep | -0.20% | 0.50% | 1.00% | 0.70% |

| 05:30 | EUR | France GDP Q/Q Q3 P | 3.00% | 2.40% | 1.10% | |

| 07:00 | CHF | KOF Leading Indicator Oct | 110.7 | 108 | 110.6 | 111 |

| 08:00 | EUR | Italy GDP Q/Q Q3 P | 2.60% | 2.00% | 2.70% | |

| 08:00 | EUR | Germany GDP Q/Q Q3 P | 1.80% | 2.20% | 1.60% | |

| 08:30 | GBP | Mortgage Approvals Sep | 73K | 73K | 74K | |

| 08:30 | GBP | M4 Money Supply M/M Sep | 0.60% | 0.50% | 0.50% | |

| 10:00 | EUR | Eurozone GDP Q/Q Q3 P | 2.20% | 2.10% | 2.20% | |

| 10:00 | EUR | Eurozone CPI Y/Y Oct P | 4.10% | 3.70% | 3.40% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Oct P | 2.10% | 1.90% | 1.90% | |

| 12:30 | CAD | GDP M/M Aug | 0.40% | 0.70% | -0.10% | |

| 12:30 | CAD | Industrial Product Price M/M Sep | 1.00% | 1.00% | -0.30% | |

| 12:30 | CAD | Raw Material Price Index Sep | 2.50% | 2.50% | -2.40% | |

| 12:30 | USD | Personal Income M/M Sep | -1.00% | 0.10% | 0.20% | |

| 12:30 | USD | Personal Spending M/M Sep | 0.60% | 0.60% | 0.80% | |

| 12:30 | USD | PCE Price Index M/M Sep | 0.30% | 0.30% | 0.40% | 0.30% |

| 12:30 | USD | PCE Price Index Y/Y Sep | 4.40% | 4.70% | 4.30% | 4.20% |

| 12:30 | USD | Core PCE Price Index M/M Sep | 0.20% | 0.20% | 0.30% | |

| 12:30 | USD | Core PCE Price Index Y/Y Sep | 3.60% | 3.70% | 3.60% | |

| 12:30 | USD | Employment Cost Index Q3 | 1.30% | 0.90% | 0.70% | |

| 13:45 | USD | Chicago PMI Oct | 63 | 64.7 | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Oct F | 71.4 | 71.4 |