Commodity currencies rise broadly today on the back on risk-on sentiments. Major European indexes are trading up while US futures also point to higher open. Yen is extending recent broad based decline since though treasury yields are in retreat. Dollar and Euro are following as next weakest. Sterling and Swiss Franc are mixed, helped by buying against Euro, Dollar and Yen.

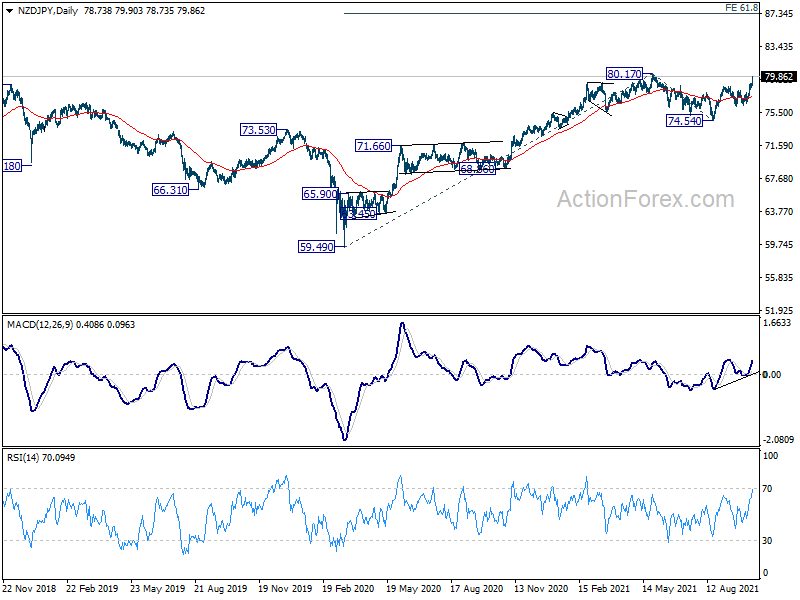

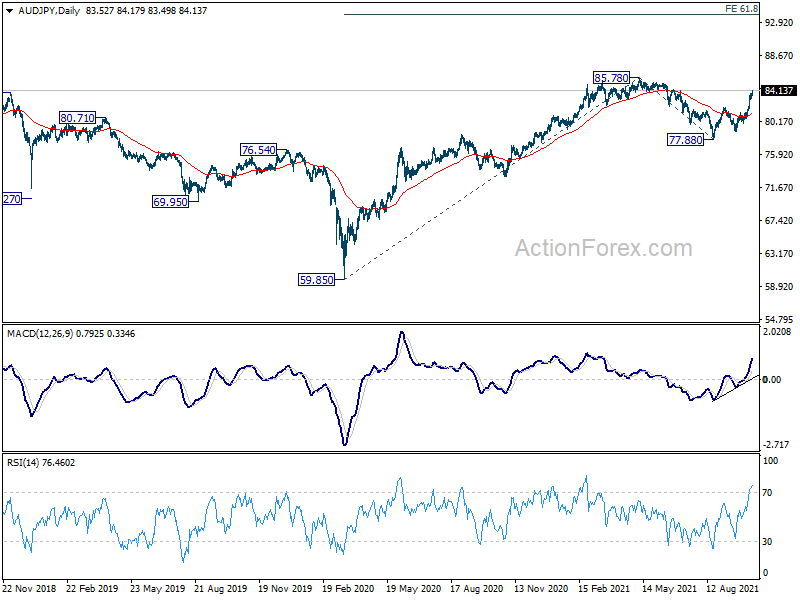

Technically, CAD/JPY has taken out 91.16 resistance earlier this week to resume medium term up trend from 73.80. Now, it’s NZD/JPY turn to take on 80.17 resistance. Break there will resume the up trend form 59.49 for 61.8 projection of 59.49 to 80.17 from 74.54 at 87.32. AUD/JPY is lagging behind, but firm break of 85.78 will also resume the up trend form 59.85 to 61.8% projection of 59.85 to 85.78 from 77.88 at 93.90 in the medium term.

{kind=link}

{kind=link}

In Europe, at the time of writing, FTSE is up 0.82%. DAX is up 1.23%. CAC is up 1.15%. Germany 10-year yield is down -0.046. Earlier in Asia, Nikkei rose 1.46%. China Shanghai SSE dropped -0.10%. Singapore Strait Times rose 0.27%. Japan 10-year JGB yield dropped -0.0048 to 0.085.

US initial jobless claims dropped to 293k, continuing claims blow 2.6m

US initial jobless claims dropped -36k to 293k in the week ending October 9, much better than expectation of 325k. That’s the lowest level since March 14, 2020. Four-week moving average of initial claims dropped -10.5k to 334k, lowest since March 14, 2020.

Continuing claims dropped -134k to 2593k, lowest since March 14, 2020. Four-week moving average of continuing claims dropped -30.5k to 2738k, lowest since March 21, 2020.

US PPI jumped to 8.6% yoy in Sep, highest on record

US PPI for final demand rose 0.5% mom in September, matched expectations. For the 12-month, PPI accelerated to 8.6% yoy, up from 8.3% yoy, below expectation of 8.8% yoy. But that’s still the largest 12-month advance on record since 2010. PPI core rose 0.2% mom, 6.8% yoy, versus expectation of 0.4% mom, 7.1% yoy.

ECB Lagarde: No evidence of significant second-round effects of inflation

ECB President Christine Lagarde repeated today, “we continue to view this upswing as being largely driven by temporary factors. The impact of these factors should fade out of annual rates of price changes in the course of next year, dampening annual inflation.”

“So far, there is no evidence of significant second-round effects through wages and inflation expectations in the euro area remain anchored, but we continue to monitor risks to the inflation outlook carefully,” she added.

On the other hand, Governing Council Member Olli Rehn said, “due to persistent production bottlenecks, it is possible that an increase in energy prices has a longer-lasting impact on consumer price. We analyze this development carefully at the Governing Council and at the Bank of Finland.” He noted that medium-term inflation expectations have increased to around 1.9%, which is in line with the European Central Bank’s strategy.

BoE Tenreyro: Self-defeating to try to respond to short-lived effects on inflation

BoE MPC member Silvana Tenreyro said, “part of increasing inflation we have seen so far is arithmetic base effects compared to a low level of prices last year.” And that in part has seen “driven by global prices in energy and other commodities which push up on inflation”. And, “these effects in general tend to be short-lived.

Additionally, there were “temporary supply disruptions caused by the various imbalances in the global economy as it recovers from Covid”, with some countries still in lockdown. Demand was also boosted “far more by fiscal stimulus in some countries than others”, like the US.

“So typically, for short-lived effects on inflation, such as the big rises in the prices of semiconductors or energy prices, it would be self-defeating to try to respond to their direct effects,” she said. “By the time interest rates were having a major effect on inflation the effects of energy prices would already be dropping out of the inflation calculation. If some effects were to prove more persistent it would be important to balance the risks from a period of above target inflation with the cost of weaker demand.”

BoJ Noguchi: Economic recovery will become clearer at the end of year

BoJ board member Asahi Noguchi said the central bank should continue with the currency easing “patiently” because it takes a long time to achieve the 2% inflation target. But he’s optimistic that economic recovery will become clearer at the end of the year and onwards, as vaccinations help to ease the pandemic impacts.

Separately, Governor Haruhiko Kuroda said in a G20 finance meeting that some emerging economies are still facing downward pressure form the pandemic. But the overall impact on the global economy will “gradually subside”.

Australia employment dropped -138k in Sep, back below pre-pandemic levels

Australia employment dropped -138k in September, worse than expectation of -120k. Full-time jobs grew 26.7k while part-time jobs lost -164.7. Unemployment rate rose 0.1% to 4.6%, better than expectation of 4.8%. Participation rate dropped sharply by -0.7% to 64.5%.

Bjorn Jarvis, head of labour statistics at the ABS, said: “Extended lockdowns in New South Wales, Victoria and the Australian Capital Territory have seen employment and hours worked both drop back below their pre-pandemic levels.

“There were large falls in employment in Victoria (123,000 people) and New South Wales (25,000 people, following the 173,000 decline in August). This was partly offset by a 31,000 increase in Queensland, as conditions there recovered from the lockdown in early August.”

“The low national unemployment rate continues to reflect reduced participation during the recent lockdowns, rather than strong labour market conditions.”

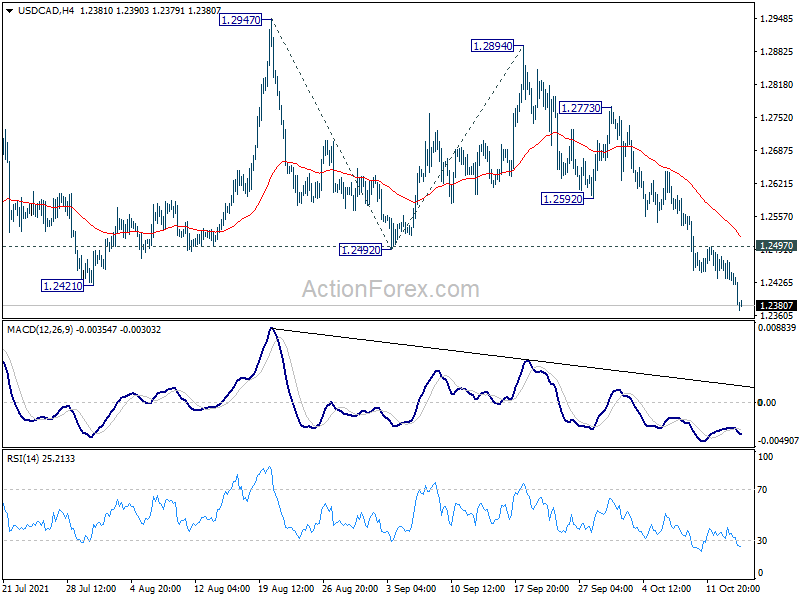

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2424; (P) 1.2451; (R1) 1.2472; More…

USD/CAD dropped further to as low as 1.2371 so far today. The break of 1.2421 key structural support suggests that larger rise from 1.2005 has completed at 1.2947 already. Intraday bias is now on the downside for 161.8% projection of 1.2947 to 1.2492 from 1.2894 at 1.2158 next. On the upside, above 1.2497 minor resistance will turn intraday bias neutral and bring consolidations. But risk will now remain on the downside as long as 1.2592 support turned resistance holds.

{kind=link}

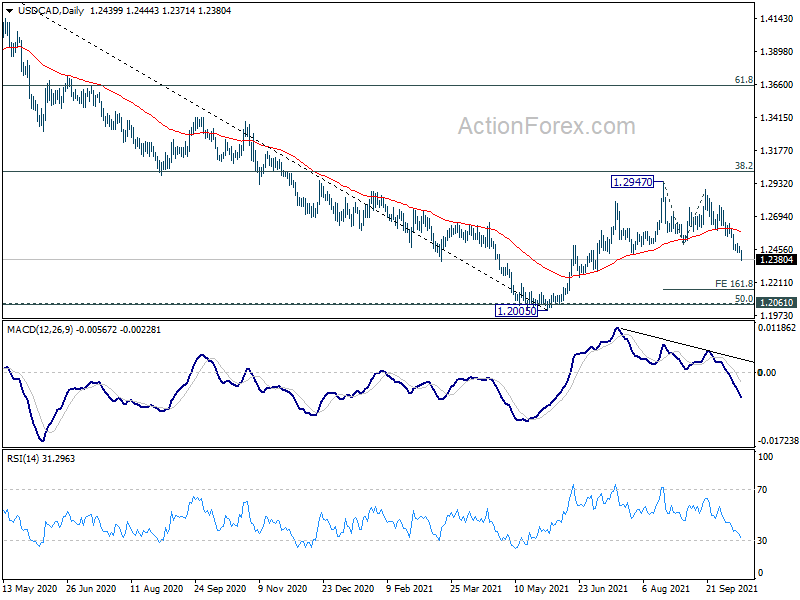

In the bigger picture, current development suggests that rebound from 1.2005 has already completed after rejection by 38.2% retracement of 1.4667 to 1.2005 at 1.3022. That in turn argues that down trend form 1.4667 (2020 high) is not completed. Medium term bearishness is also affirmed by the failure to sustain above 55 week EMA. Break of 1.2005 will resume the down trend to next long term fibonacci level at 61.8% retracement of 0.9406 to 1.4689 at 1.1424

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS Housing Price Balance Sep | 68% | 70% | 73% | 72% |

| 00:00 | AUD | Consumer Inflation Expectations Oct | 3.60% | 4.40% | ||

| 00:30 | AUD | Employment Change Sep | -138.0K | -120.0K | -146.3K | |

| 00:30 | AUD | Unemployment Rate Sep | 4.60% | 4.80% | 4.50% | |

| 01:30 | CNY | CPI Y/Y Sep | 0.70% | 0.90% | 0.80% | |

| 01:30 | CNY | PPI Y/Y Sep | 10.70% | 10.50% | 9.50% | |

| 04:30 | JPY | Industrial Production M/M Aug F | -3.60% | -3.20% | -3.20% | |

| 06:30 | CHF | Producer and Import Prices M/M Sep | 0.20% | 0.90% | 0.70% | |

| 06:30 | CHF | Producer and Import Prices Y/Y Sep | 4.50% | 4.40% | 4.40% | |

| 12:30 | CAD | Manufacturing Sales M/M Aug | 0.50% | 0.40% | -1.50% | -1.20% |

| 12:30 | USD | PPI M/M Sep | 0.50% | 0.50% | 0.70% | |

| 12:30 | USD | PPI Y/Y Sep | 8.60% | 8.80% | 8.30% | |

| 12:30 | USD | PPI Core M/M Sep | 0.20% | 0.40% | 0.60% | |

| 12:30 | USD | PPI Core Y/Y Sep | 6.80% | 7.10% | 6.70% | |

| 12:30 | USD | Initial Jobless Claims (Oct 8) | 293K | 325K | 326K | 326K |

| 14:30 | USD | Natural Gas Storage | 97B | 118B | ||

| 15:00 | USD | Crude Oil Inventories | 1.1M | 2.3M |