Selloff in Euro remains the main theme in slow markets today. Return of risk appetite is also weighing down Dollar and Yen. On the other hand, commodity currencies are generally strong, with Aussie having an upper hand over Kiwi and Loonie. Sterling is mixed for now, partly supported by buying against European majors. While stocks are rebounding, major indexes are staying in familiar range. Traders would like to wait for tomorrow’s US NFP before taking a committed stance.

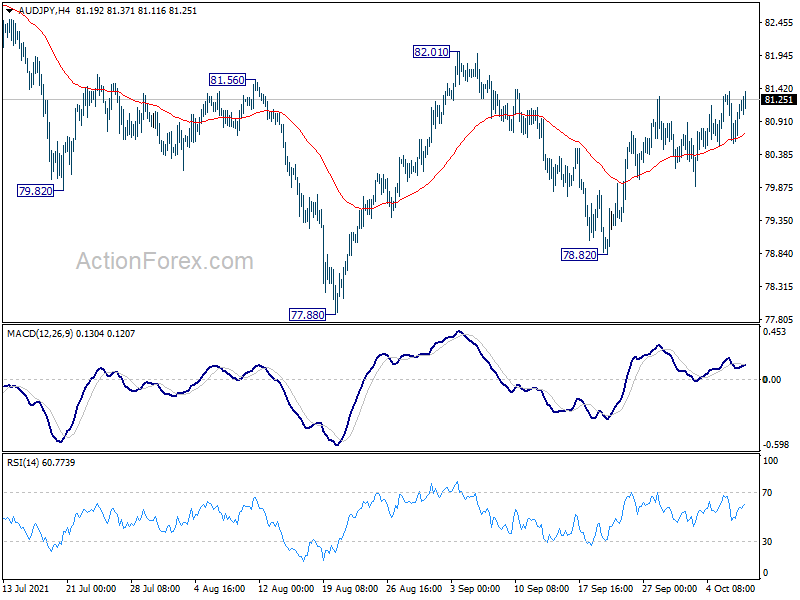

Technically, as EUR/AUD is breaking away from 1.5898 structural support cleanly, we’d also keep an eye on 0.7315 minor resistance in AUD/USD. Firm break there will argue that the pull back from 0.7477 has completed and further rise could be seen through this resistance to resume the whole rebound from 0.7105. AUD/JPY appears to be building a base for further rise with help from 4 hour 55 EMA. Break of 82.01 resistance will resume the rebound from 77.88.

{kind=link}

In Europe, at the time of writing, FTSE is up 1.20%. DAX is up 1.45%. CAC is up 1.63%. Germany 10-year yield is down -0.0016 at -0.191. Earlier in Asia, Nikkei rose 0.54%. Hong Kong HSI rose 3.07%. Singapore Strait Times rose 0.56%. 10 year JGB yield dropped -0.0071 to 0.078.

US initial jobless claims dropped to 326k, below expectations

US initial jobless claims dropped -38k to 326k in the week ending October 2, below expectation of 349k. Four-week moving average of initial claims rose 3.5k to 344k.

Continuing claims dropped -97k to 2714k in the week ending September 25, lowest since March 14, 2020. Four-week moving average of continuing claims dropped -34.5k to 2765k, lowest since March 21, 2020.

ECB Accounts: Support from sustained pace of net PEPP purchases deemed essential

In the accounts of ECB’s September 8-9 meeting, Governing Council members concurred with the assessment that “an accommodative monetary policy stance remained”. Also, “policy support from a sustained pace of net purchases under the PEPP, along with the other instruments and the recalibrated forward guidance, was deemed essential”.

Financing conditions had “had remained favourable or had loosened further” since June, and was “visible across a broad spectrum of indicators”. Inflation outlook had a “significant improvement over the course of the year”. However, the near-term increase in inflation was “largely driven by temporary factors that would fade in the medium term and not call for policy tightening.”

Regarding the reduction in PEPP purchase pace in Q4, on the one hand, it was argued that “a symmetric application of the PEPP framework would call for a more substantial reduction in the pace of purchases”. On the other hand, “reference was made to the recent repricing in nominal bond yields, which called for a prudent reduction in the pace of purchases”.

Also, it’s noted that “markets were already expecting an end to net asset purchases under the PEPP by March 2022”, but such expectation was “not showing a significant impact on financing conditions”.

Overall, all members agreed to “moderately scale down the pace of purchases under the PEPP”.

ECB Stournaras: Speculation of 2023 rate hike is not in accordance with our forward guidance

ECB Governing Council member Yannis Stournaras told Bloomberg TV that speculations for a first hike around mid-2023 are “not in accordance with our forward guidance”. He added that the central bank will try to avoid any disruption after the end of the PEPP.

“Asset purchases aim at favorable financing conditions, at smooth transition of monetary policy to prevent any kind of fragmentation in jurisdictions in the euro area,” Stournaras said. “I’m sure that the Governing Council will continue to aim at this.”

Stournaras also said Eurozone is “not in the same position” as the US on inflation. He said, “the inflation forecasts are lower for the euro zone than in the U.S. and in the U.K. It’s natural that we’re in a different phase of monetary policy.”

Separately, Governing Council member Francois Villeroy de Galhau said he expected inflation to fall back below 2% within a year.

Released in European session, Italy retail sales rose 0.4% mom in August versus expectation of 0.2% mom. France trade deficit narrowed to EUR -6.7B in August, versus expectation of EUR -6.8B. Germany industrial production dropped -4.0% mom in August, versus expectation of -0.5% mom. From Swiss, unemployment rate dropped to 2.8% in September while foreign currency reserves rose to CHF 940B.

BoE Pill: Risks to economic and inflation outlook becoming two-sided

In reply to a questionnaire by the Treasury Select Committee, BoE policymaker Huw Pill said he expected interest rates to “remain at relatively low levels for the coming years, even as the impact of the COVID-19 pandemic recede.”

But he acknowledged that “balance of risks is currently shifting towards great concerns about the inflation outlook.” Also, “current strength of inflation looks set to prove more long lasting than originally anticipated.” He emphasized that “risks to the economic and inflation outlook are again clearly becoming two-sided”.

On BoE’s balance sheet, Pill said, “at a time when financial markets appear to be functioning normally, a gradual and predictable reduction in the stock of asset purchases can be achieved without disrupting markets and/or creating an undesired abrupt tightening of financial and monetary conditions”.

Australia AiG services ticked up to 45.7 in Sep, mild upturn expected in Oct

Australia AiG Performance of Services Index rose slightly by 0.1 pts to 45.7 in September, marking a second month in contraction. Looking at some details, sales rose 1.4 to 41.4. Employment dropped -1.4 to 52.0. New orders dropped -7.6 to 39.8. Supplier deliveries rose 3.0 to 47.0. Finished stocks rose 15.8 to 53.5. Input prices dropped -.7.0 to 64.5. Selling prices dropped -1.4 to 53.9.

Ai Group Chief Executive, Innes Willox, said: “Restrictions associated with the delta outbreaks in south eastern Australia were the major contributor to the continued contraction of the Australian services sector in September… While predictions are highly conditional, we are expecting a mild upturn in October followed by further gains as restrictions are eased in line with higher levels of vaccination.”

BoJ Kuroda expects economy to recover as pandemic impact subsides

BoJ Governor Haruhiko Kuroda said Japan’s economy is expected to recover ahead as the impact of the pandemic gradually subsides. BoJ is closely watching the coronavirus impact. He pledged again that it “won’t hesitate to ease policy further if necessary”.

Kuroda also said that core CPI is expected to linger around 0% for the near term, but it would “pick up pace gradually”. Also, the financial system remains stable and financial conditions are accommodative overall.

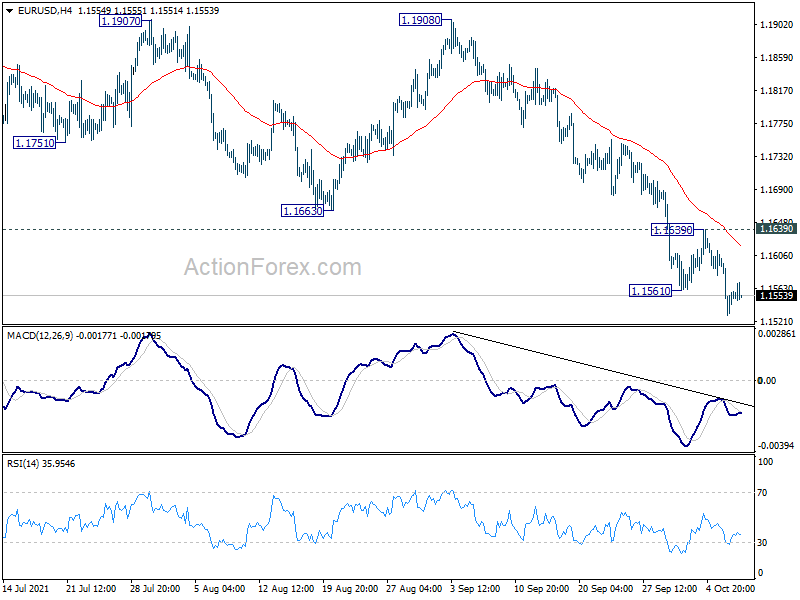

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1524; (P) 1.1563; (R1) 1.1595; More…

Intraday bias in EUR/USD remains on the downside for the moment. The decline from 1.2348 high is in progress and should target 1.1289 medium term fibonacci level. On the upside, break of 1.1639 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

{kind=link}

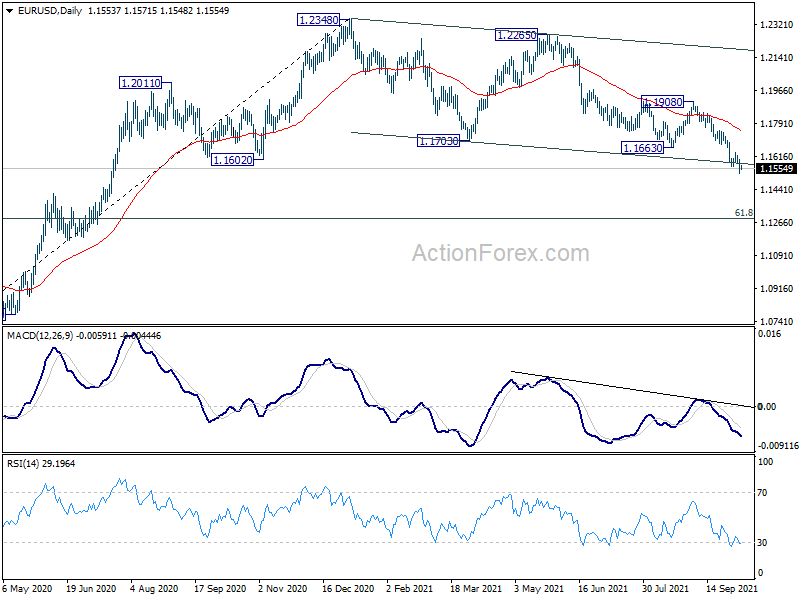

In the bigger picture, sustained break of 1.1602 will argue that rise from 1.0635 (2020 low) has completed at 1.2348. Deeper fall would be seen to 61.8% retracement of 1.0635 to 1.2348 at 1.1289. Note also that rejection by 55 week EMA (1.1830) also carries medium term bearish implication. Firm break of 1.1289 will pave the way to retest 1.0635 low. On the upside, though, break of 1.1908 resistance will revive medium term bullishness and turn focus back to 1.2348 high.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Services Index Sep | 45.7 | 45.6 | ||

| 05:00 | JPY | Leading Economic Index Aug P | 101.8 | 104.3 | 104.1 | |

| 05:45 | CHF | Unemployment Rate Sep | 2.80% | 2.80% | 2.90% | |

| 06:00 | EUR | Germany Industrial Production M/M Aug | -4.00% | -0.50% | 1.00% | 1.30% |

| 06:45 | EUR | France Trade Balance (EUR) Aug | -6.7B | -6.8B | -7.0B | -7.1B |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Sep | 940B | 929B | ||

| 08:00 | EUR | Italy Retail Sales M/M Aug | 0.40% | 0.20% | -0.40% | -0.30% |

| 11:30 | EUR | ECB Monetary Policy Accounts | ||||

| 11:30 | USD | Challenger Job Cuts Y/Y Sep | -84.90% | -86.40% | ||

| 12:30 | USD | Initial Jobless Claims (Oct 1) | 326K | 349K | 362K | 364K |

| 14:00 | CAD | Ivey PMI Sep | 60.7 | 66 | ||

| 14:30 | USD | Natural Gas Storage | 104B | 88B |