The markets are back on risk-off mode again today, while major global treasury yields trade higher. Stronger than expected ADP job data provides little support to over sentiment. Yen is leading the way higher, followed by Dollar and Swiss Franc. On the other hand, despite RBNZ delivering the expected rate hike, New Zealand Dollar is leading commodity currencies lower. Euro is also weak together, as pressured by Dollar, Yen and other European majors.

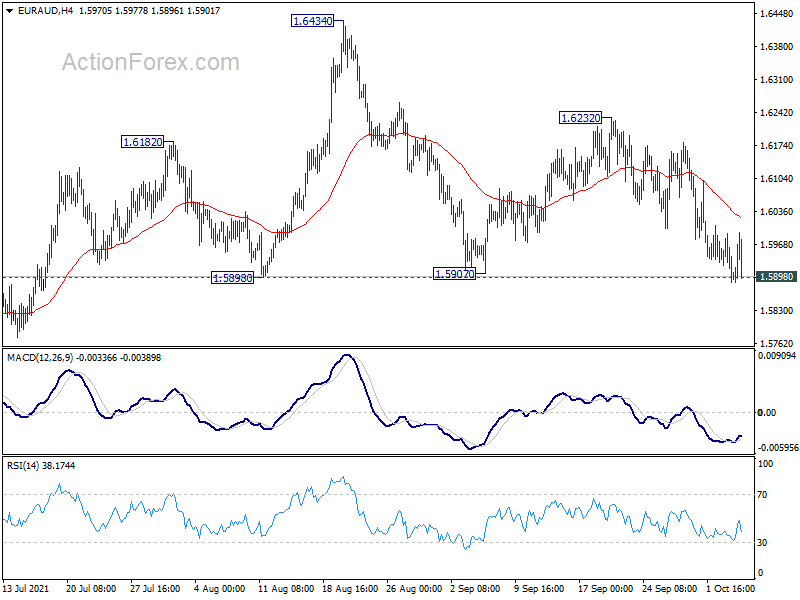

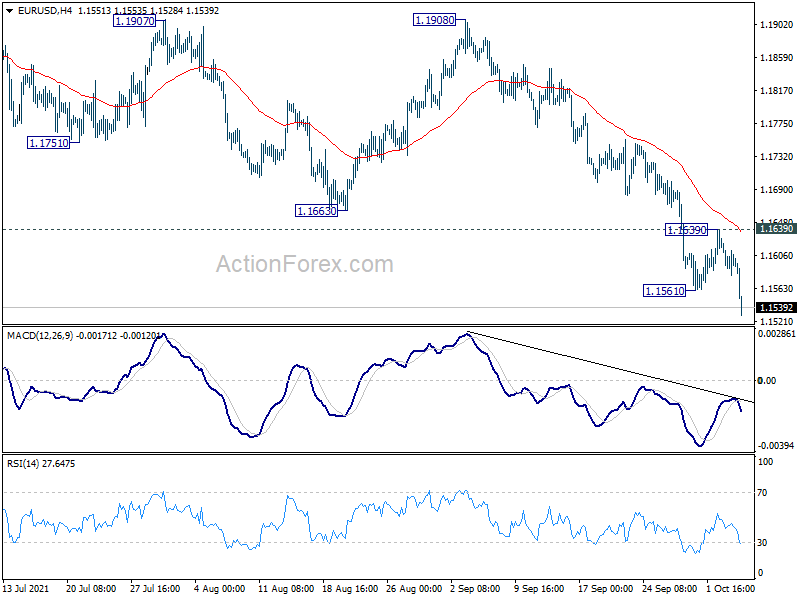

Technically, EUR/USD’s decline resumes by breaking 1.1561 temporary low. EUR/CHF hits as low as 1.0712 and it’s on track to retest 1.0694 low. EUR/GBP’s break of 0.8499 support should also set the stage for retesting 0.8448 low. A focus now is on whether EUR/AUD could sustain below 1.5898 structural support to indicate near term bearish reversal.

{kind=link}

In Europe, at the time of writing, FTSE is down -1.51%. DAX is down -1.70%. CAC is down -1.83%. Germany 10-year yield is up 0.005 at -0.179. Earlier in Asia, Nikkei dropped -1.05%. Hong Kong HSI dropped -0.57%. Singapore Strait Times rose 0.51%. Japan 10-year JGB yield rose 0.0275 to 0.085.

US ADP employment grew 568k in Sep, recovery continues to make progress

US ADP private sector employment grew 568k in September, above expectation of 475k. By company size, small businesses added 63k jobs, medium businesses added 115k, large businesses added 390k. By sector, goods-producing jobs grew 102k, and service-providing jobs rose 466k.

“The labor market recovery continues to make progress despite a marked slowdown from the 748,000 job pace in the second quarter,” said Nela Richardson, chief economist, ADP. “Leisure and hospitality remains one of the biggest beneficiaries to the recovery, yet hiring is still heavily impacted by the trajectory of the pandemic, especially for small firms. Current bottlenecks in hiring should fade as the health conditions tied to the COVID-19 variant continue to improve, setting the stage for solid job gains in the coming months.”

Eurozone retail sales rose 0.3% mom in Aug, EU up 0.3% mom

Eurozone retail sales rose 0.3% mom in August, well below expectation of 0.8% mom rise. Volume of retail trade increased by 1.8% for non-food products, while it fell by 0.1% for automotive fuels and by 1.7% for food, drinks and tobacco.

EU retail sales rose 0.3% mom. Among Member States for which data are available, the highest monthly increases in total retail trade were registered in Malta (+2.7%), Ireland (+2.5%) and Slovakia (+2.0%). The largest decreases were observed in Denmark (-1.4%), Estonia and France (both -1.2%).

UK PMI construction dropped to 52.6, severe loss of momentum

UK PMI Construction dropped to 52.6 in September, down from August’s 55.2, missed expectation of 53.9. Markit said output growth eased for the third month running. Sub-contractor charges increased at survey-record pace. Widespread supply shortages led to rapid cost inflation.

Tim Moore, Director at IHS Markit said: “September data highlighted a severe loss of momentum for the construction sector as labour shortages and the supply chain crisis combined to disrupt activity on site. The volatile price and supply environment has started to hinder new business intakes… Shortages of building materials and a lack of transport capacity led to another rapid increase in purchase prices… Measured overall, prices charged by sub-contractors increased at the fastest rate since the survey began in April 1997.”

BoJ Kuroda: No pressing need for firms to raise wages and selling prices

BoJ Governor Haruhiko Kuroda said in a speech, Japan’s economy has “picked up”, led by exports and the manufacturing sector. “If Japan can simultaneously protect public health and improve consumption activities through the use of vaccination certificates, for example, the economic recovery trend is very likely to become more pronounced, even in the services sector, also supported by the materialization of pent-up demand,” he added.

On the contrasting development in CPI compared with the US, Kuroda said demand in Japan “has not recovered as rapidly as that in the U.S”. Also, “many Japanese firms have essentially maintained their labor, supply-side constraints in Japan have not been as severe as in the U.S., and there has been no pressing need for firms to raise wages and selling prices.”

RBNZ hikes OCR to 0.50%, maintains hawkish bias

RBNZ raised the Official Cash Rate by 25bps to 0.50% as widely expected, as “it is appropriate to continue reducing the level of monetary stimulus so as to maintain low inflation and support maximum sustainable employment.” It maintains a hawkish bias and said, “further removal of monetary policy stimulus is expected over time, with future moves contingent on the medium-term outlook for inflation and employment.”

In the accompany statement, it’s noted that current COVID-19-related restrictions “have not materially changed the medium-term outlook” for inflation and employment. Capacity pressures “remain evident” and economic data highlighted that the economy “has been performing strongly in aggregate”. Headline CPI is expected to rise above 4% in the near term before returning towards 2% target midpoint over the medium term.

More on RBNZ:

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1579; (P) 1.1600; (R1) 1.1620; More…

EUR/USD’s decline resumes by breaking 1.1561 temporary low. Break of channel support also indicates downside acceleration. Intraday bias is back on the downside and deeper fall would be seen to 1.1289 medium term fibonacci level. On the upside, break of 1.1639 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

{kind=link}

In the bigger picture, sustained break of 1.1602 will argue that rise from 1.0635 (2020 low) has completed at 1.2348. Deeper fall would be seen to 61.8% retracement of 1.0635 to 1.2348 at 1.1289. Note also that rejection by 55 week EMA (1.1830) also carries medium term bearish implication. Firm break of 1.1289 will pave the way to retest 1.0635 low. On the upside, though, break of 1.1908 resistance will revive medium term bullishness and turn focus back to 1.2348 high.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:00 | NZD | RBNZ Rate Decision | 0.50% | 0.50% | 0.25% | |

| 01:00 | NZD | RBNZ Rate Statement | ||||

| 06:00 | EUR | Germany Factory Orders M/M Aug | -7.70% | -1.50% | 3.40% | |

| 08:30 | GBP | Construction PMI Sep | 52.6 | 53.9 | 55.2 | |

| 09:00 | EUR | Eurozone Retail Sales M/M Aug | 0.30% | 0.80% | -2.30% | -2.60% |

| 12:15 | USD | ADP Employment Change Sep | 568K | 475K | 374K | |

| 14:30 | USD | Crude Oil Inventories | 0.8M | 4.6M |