Overall markets are relatively quiet today so far. Yen continues to reverse this week’s gain as risk sentiment appear to have stabilized. Dollar also softens while Sterling dips mildly after poor retail sales data. On the other hand, commodity currencies are recovering, as lead by Canadian, which is then supported as WTI oil price stays firm above 72 handle.

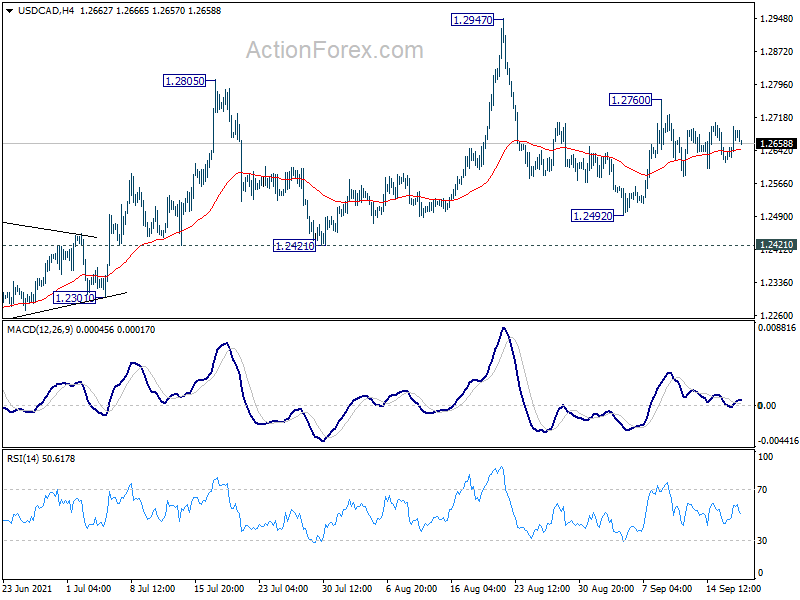

Technically, USD/CAD could be a focus today as it’s about time for a range break out. Break of 1.2760 will resume the rebound from 1.2492, to retest 1.2947 high. Also, as 1.2421 support was well defended below, larger rise from 1.2005 should still be in progress. Break of 1.2947 will confirm this bullish case. If that happens, we’d also see whether Dollar would also rise further elsewhere.

{kind=link}

In Asia, Nikkei closed up 0.58%. Hong Kong HSI is up 0.46%. China Shanghai SSE is up 0.05%. Singapore Strait Times is down -0.22%. Japan 10-year JGB yield is up 0.0057 at 0.051. Overnight, DOW dropped -0.18%. S&P 500 dropped -0.16%. NASDAQ rose 0.13%. 10-year yield rose 0.027 to 1.331.

UK retail sales dropped -0.9% mom in Aug, ex-fuel sales dropped -1.2% mom

UK retail sales dropped -0.9% mom in August, well below expectation of 0.5% mom rise. For the 12-month period, headline sales rose 0.0% yoy versus expectation of 2.6% yoy.

Overall sales volume were still up 0.3% in the three months to August, compared with the previous three months. It’s also 4.6% higher than their pre-pandemic levels in February 2020.

Ex-fuel sales dropped -1.2% mom, well below expectation of 0.7% mom rise too. For the 12-month period, ex-fuel sales dropped -0.9% yoy versus expectation of 2.5% yoy.

New Zealand BusinessNZ manufacturing dropped to 40.1, economic pain being felt

New Zealand BusinessNZ manufacturing index dropped to 40.1 in August, down from 62.6, back in contraction. Looking at some more details, production tumbled from 63.9 to 27.7. Employment dropped from 57.9 to 54.5. New orders dropped from 63.7 to 44.4. Finished stocks dropped from 56.8 to 46.1 Deliveries dropped from 56.3 to 33.6.

BNZ Senior Economist, Doug Steel stated that “while many anticipate a bounce in activity as the country progresses down alert levels (all going well on the Covid front), today’s PMI clearly demonstrates the economic pain being felt. This should not be underestimated, even if there is hope for the future. GDP and manufacturing output are expected to fall heavily in Q3. It is something of a reality check in the afterglow of yesterday’s very strong Q2 GDP outcome.”

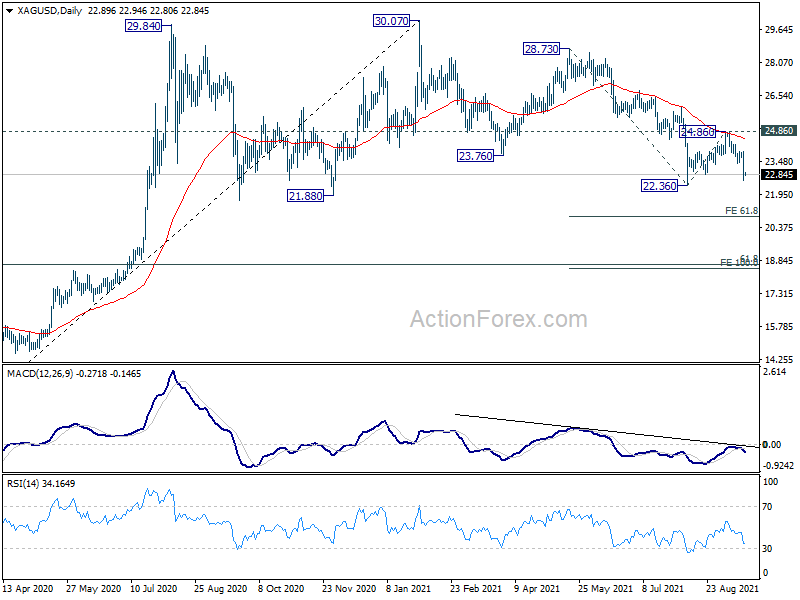

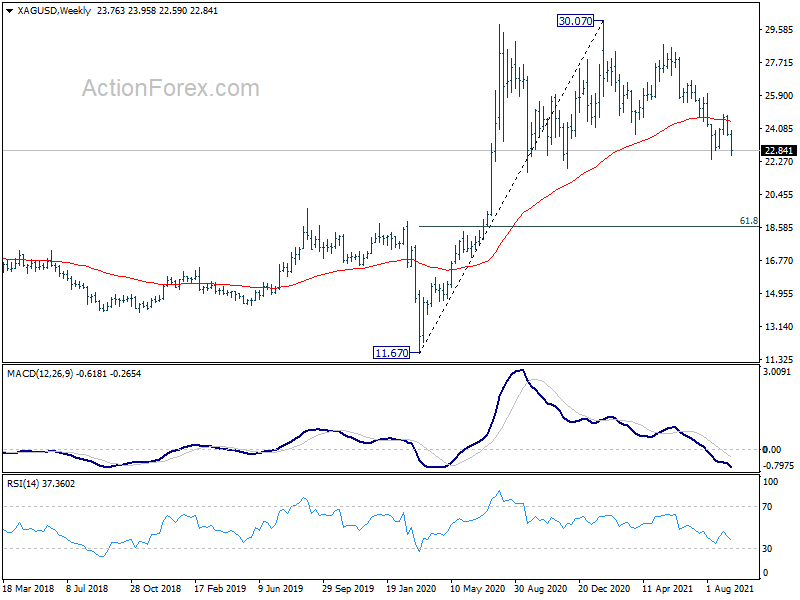

Silver heading to 22.36 support after rejection by 55 day EMA

Silver follows Gold and drops sharply this week. The development should confirm rejection by 55 day EMA and the bearish signal suggests that larger decline from 30.07 is ready to resume. Near term focus is now back on 22.36 support. Break there will target 61.8% projection of 28.73 to 22.36 from 24.86 at 20.92.

Also, the rejection by 55 week EMA also carries medium term bearish implication. The whole decline from 30.07 has the potential to drop to as low as 61.8% retracement of 11.67 to 30.07 at 18.69 before completion.

{kind=link}

{kind=link}

Looking ahead

Eurozone will release current account and CPI final. Later in the day, US will release Michigan consumer sentiment.

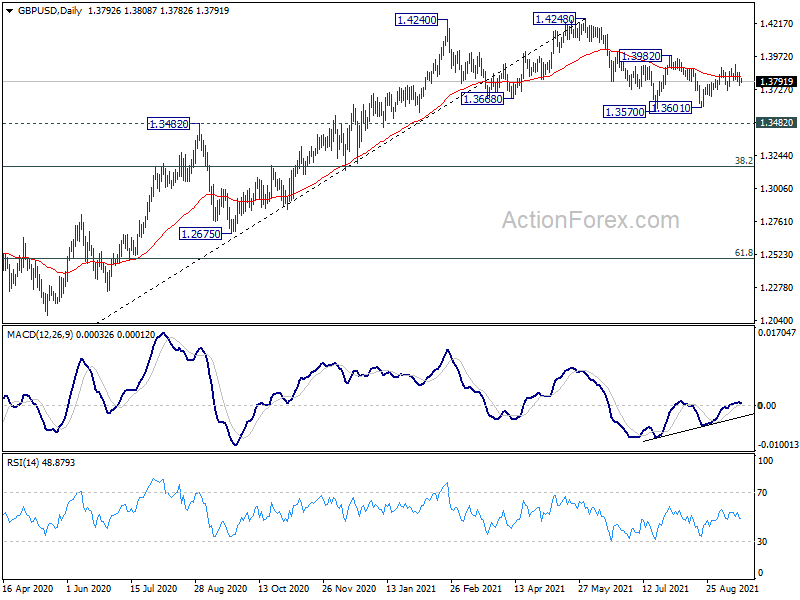

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3754; (P) 1.3804; (R1) 1.3842; More…

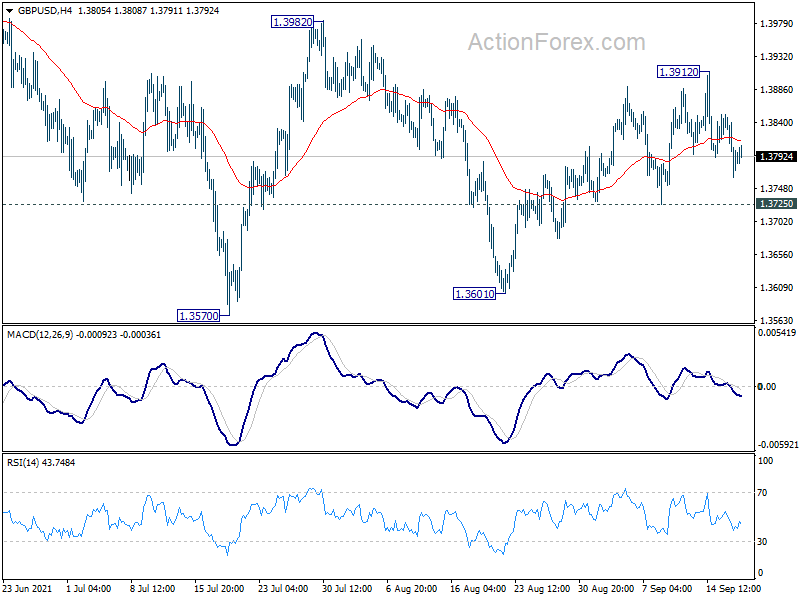

GBP/USD’s fall from 1.3912 is extending, but downside is contained by 1.3725 support so far. Intraday bias remains neutral first. On the upside, break of 1.3912 will target 1.3982 resistance next. Decisive break there will indicate that fall from 1.4248 has completed. Stronger rally would then be seen back to 1.4248 high. On the downside, however, break of 1.3725 support will turn bias back to the downside for retesting 1.3570/3601 support zone instead.

{kind=link}

In the bigger picture, as long as 1.3482 resistance turned support holds, we’d still treat price actions from 1.4248 as a corrective move. That is, up trend from 1.1409 (2020 low) is in favor to resume. Decisive break of 1.4376 key resistance (2018 high) would indeed carry long term bullish implications. However, sustained break of 1.3482 will at least bring deeper fall to 38.2% retracement of 1.1409 to 1.4248 at 1.3164, or even further to 61.8% retracement at 1.2493.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | BusinessNZ Manufacturing Index Aug | 40.1 | 62.6 | ||

| 06:00 | GBP | Retail Sales M/M Aug | -0.90% | 0.50% | -2.50% | -2.80% |

| 06:00 | GBP | Retail Sales Y/Y Aug | 0.00% | 2.60% | 2.40% | |

| 06:00 | GBP | Retail Sales ex-Fuel M/M Aug | -1.20% | 0.70% | -2.40% | |

| 06:00 | GBP | Retail Sales ex-Fuel Y/Y Aug | -0.90% | 2.60% | 1.80% | |

| 08:00 | EUR | Eurozone Current Account (EUR) Jul | 22.3B | 21.8B | ||

| 08:30 | GBP | Consumer Inflation Expectations | 2.40% | |||

| 09:00 | EUR | Eurozone CPI Y/Y Aug | 3.00% | 3% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Aug | 1.60% | 1.60% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Sep P | 70.2 | 70.3 |