Dollar drops broadly after data shows declining headline consumer inflation in the US, and even quicker fall in core CPI. It’s adding to the Fed’s case that prior surge in inflation was just transitory. DOW futures responde rather positively to the news. Strengthening risk appetite could put Yen under some pressure too. Meanwhile, Sterling is currently the strongest one for today, but there is prospect of a rebound in commodity currencies today.

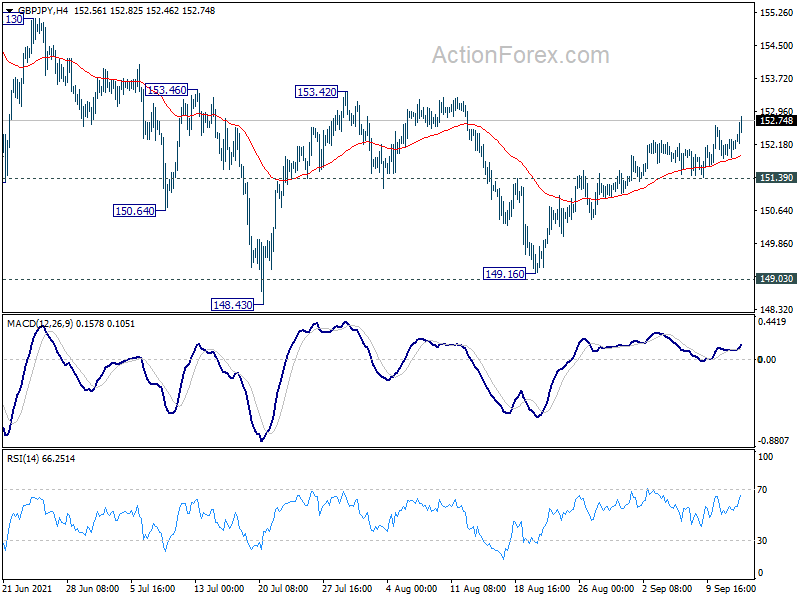

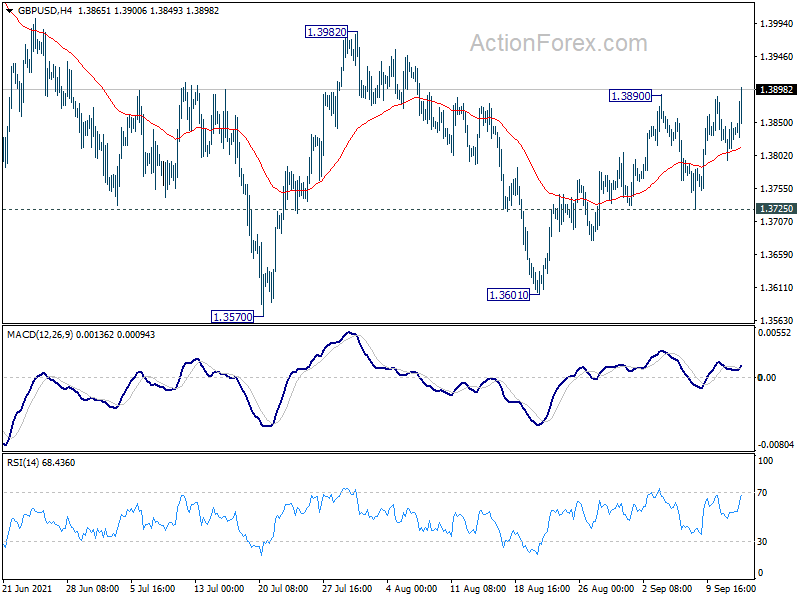

Technically, GBP/USD’s break of 1.3890 resistance suggests resumption of the rebound from 1.3601 for 1.3982. GBP/JPY is also extending the rise from 149.16 towards 153.42 resistance Break of these two levels will solidify near term bullishness for the Pound, and pave the way for further rally ahead.

{kind=link}

In Europe, at the time of writing, FTSE is down -0.16%. DAX is up 0.23%. CAC is down -0.31%. Germany 10-year yield is up 0.019 at -0.310. Earlier in Asia, Nikkei rose 0.73%. Hong Kong HSI dropped -1.21%. China Shanghai SSE dropped -1.42%. Singapore Strait Times rose 0.20%. Japan 10-year JGB yield dropped -0.0011 to 0.045.

US core CPI slowed for the second month to 4.0% yoy in Aug, missed expectations

US headline CPI rose 0.3% mom, in August, below expectation of 0.4% mom. CPI core rose 0.1% mom, below expectation of 0.3% mom. Over the 12 months, headline CPI slowed to 5.3% yoy, down from 5.4% yoy, matched expectations. CPI core slowed to 4.0% yoy, down from 4.3% yoy, missed expected of 4.2% yoy. That’s indeed the second straight month of decline in core CPI.

Canada manufacturing sales dropped -1.5% mom in July

Canada manufacturing sales dropped -1.5% mom to CAD 59.6b in July, worse than expectation of -1.0% mom. Sales were down in 12 of 21 industries, led by the wood product (-21.8%), aerospace product and parts (-19.0%), miscellaneous (-12.1%) and petroleum and coal product (-2.3%) industries.

The declines were partially offset by higher sales in the motor vehicles (+13.5%), primary metal (+3.9%) and motor vehicle parts (+7.6%) industries.

Bundesbank Weidmann: A gradual approach makes sense in digital Euro

Bundesbank President Jens Weidmann said a “gradual approach” might make sense in digital Euro given the risks involved. “That means a digital euro with a specific set of features and the option to add further functionalities later,” he added.

In particular, he warned that in times of crises, consumers could rush to covert bank deposits to central bank money. That would destabilize the financial system.

UK unemployment rate dropped to 4.7%, employment rate rose to 75.2%

UK unemployment rate dropped slightly from 4.7% to 4.6% in the three months to July. That’s still 0.6% higher than pre-pandemic level. Employment rate rose to 75.2% but remains -1.3% below pre-pandemic level. Average earnings including bonus rose 8.3% 3moy, below expectation of 8.6%. Average earnings excluding bonus rose 6.8% 3moy, also below expectation of 7.3%. Claimant count dropped -58.6k in August, versus expectation of -71.7k.

From Swiss, PPI came in at 0.7% mom, 4.4% yoy in August.

RBA Lowe explains tapering asset purchases while extending the program

In a speech, RBA Governor Philip Lowe said, “n the economy, our central message is that the Delta outbreak has delayed – but not derailed – the recovery of the Australian economy”. While the outbreak is a “significant setback”, there is a “clear path out of the current difficulties”.

Lowe provided some explanations to the decision to taper weekly asset purchases to AUD 4B, but extend the program till February next year. Firstly, give the delay in recovery, “we considered it appropriate that we delay any consideration of a further taper in our bond purchases until next year.” Continuing the with purchases will also “provide some additional insurance against downside scenarios.”

Secondly, fiscal policy is considered the “more effective policy instrument in responding to the Delta outbreak.” Public balance sheet can be used to “offset the hit to private incomes during the lockdown”. But monetary policy “works mainly on the demand side and the effects on income are felt with a lag”.

Thirdly, “by continuing to purchase government bonds at the rate of $4 billion a week we will be adding to the support provided to the economy during the recovery phase.”

Lowe also reiterated that the condition for lifting interest rate will “not be met before 2024”. A “tighter labor market” is needed to meet the condition, with wages growing by “at least 3 per cent”, comparing to the 1.7% yoy rate in Q2.

Australia NAB business confidence rose to -5, resilience and well positioned to rebound

Australia NAB business confidence rose slightly from -7 to -5 in August. Business conditions improved from 10 to 14. Looking at some details, trading condition rose from 12 to 19. Profitability condition rose from 5 to 15. Employment condition, however, dropped from 11 to 9.

NAB said, “while the sustained lockdowns now in place will cause a large hit to activity in the quarter, the resilience seen in the August survey results suggest that the supports in place, and lingering momentum from earlier in the year, are continuing to support the economy”.

“There are also signs that progress on the vaccine rollout and growing certainty that lockdowns will end in coming months are providing a reason for optimism. The economy remains well positioned to rebound once restrictions are eased.”

Also released, Australia house price index rose 6.7% qoq in Q2, above expectation of 6.2% qoq.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3808; (P) 1.3829; (R1) 1.3862; More…

GBP/USD’s break of 1.3890 suggests resumption of rise from 1.3601. Intraday bias is back on the upside for 1.3982 resistance next. Decisive break there will indicate that fall from 1.4248 has completed. Stronger rally would then be seen back to 1.4248 high. On the downside, however, break of 1.3725 support will turn bias back to the downside for retesting 1.3570/3601 support zone instead.

{kind=link}

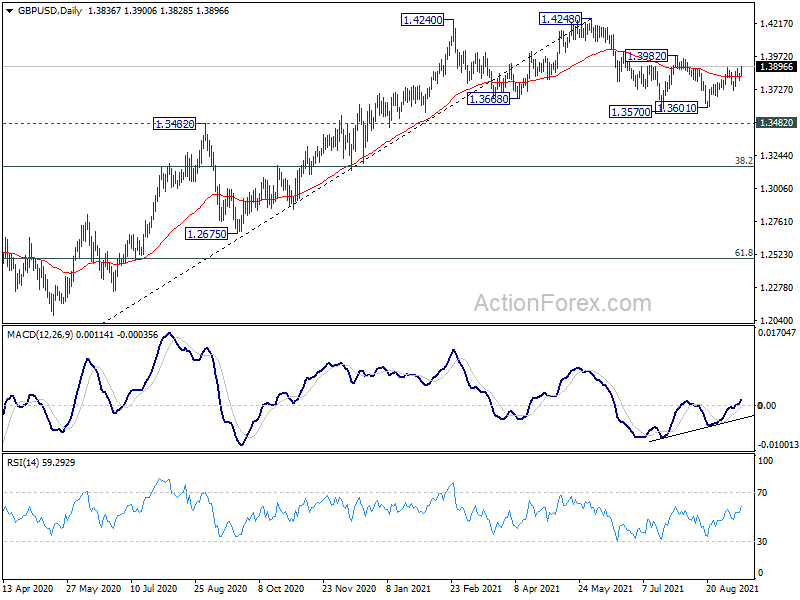

In the bigger picture, as long as 1.3482 resistance turned support holds, we’d still treat price actions from 1.4248 as a corrective move. That is, up trend from 1.1409 (2020 low) is in favor to resume. Decisive break of 1.4376 key resistance (2018 high) would indeed carry long term bullish implications. However, sustained break of 1.3482 will at least bring deeper fall to 38.2% retracement of 1.1409 to 1.4248 at 1.3164, or even further to 61.8% retracement at 1.2493.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | House Price Index Q/Q Q2 | 6.70% | 6.20% | 5.40% | |

| 01:30 | AUD | NAB Business Confidence Aug | -5 | -8 | -7 | |

| 01:30 | AUD | NAB Business Conditions Aug | 14 | 11 | 10 | |

| 04:30 | JPY | Industrial Production M/M Jul F | -1.50% | -1.50% | -1.50% | |

| 06:00 | GBP | Claimant Count Change Aug | -58.6K | -71.7K | -7.8K | |

| 06:00 | GBP | ILO Unemployment Rate (3M) Jul | 4.60% | 4.60% | 4.70% | |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Jul | 8.30% | 8.60% | 8.80% | |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jul | 6.80% | 7.30% | 7.40% | |

| 06:30 | CHF | Producer and Import Prices M/M Aug | 0.70% | 0.20% | 0.50% | |

| 06:30 | CHF | Producer and Import Prices Y/Y Aug | 4.40% | 3.30% | ||

| 10:00 | USD | NFIB Business Optimism Index Aug | 100.1 | 99 | 99.7 | |

| 12:30 | CAD | Manufacturing Sales M/M Jul | -1.50% | -1.00% | 2.10% | |

| 12:30 | USD | CPI M/M Aug | 0.30% | 0.40% | 0.50% | |

| 12:30 | USD | CPI Y/Y Aug | 5.30% | 5.30% | 5.40% | |

| 12:30 | USD | CPI Core M/M Aug | 0.10% | 0.30% | 0.30% | |

| 12:30 | USD | CPI Core Y/Y Aug | 4.00% | 4.20% | 4.30% |