Swiss Franc drops sharply today, as pressured by selling against Euro, and rising treasury yields. Dollar once again tries to recover, but there is no committed buying yet. The greenback traders will carefully scrutinize the comments from Fed officials coming out today and tomorrow, as the annual Jackson Hole Symposium goes along. Meanwhile, commodity currencies will look into stocks’ reaction and overall market sentiment.

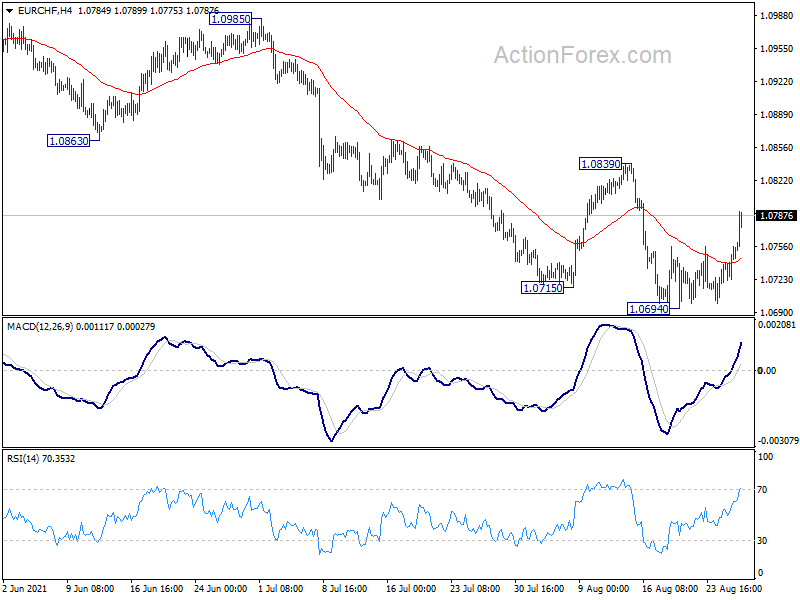

Technically, EUR/CHF’s strong rebound today raises the possibility that 1.0694 is already a short term bottom. Focus is now turning to 1.0839 resistance. Break there will bring stronger rally back towards 1.0985 resistance. If that happens, we’ll see if EUR/USD would follow and break through 1.1804 resistance. Or, USD/CHF would break through 0.9241 resistance instead.

{kind=link}

In Europe, at the time of writing, FTSE is down -0.28%. DAX is down -0.51%. CAC is down -0.25%. Germany 10-year yield is up 0.0179 at -0.402. Earlier in Asia, Nikkei rose 0.06%. Hong Kong HSI dropped -1.08%. China Shanghai SSE dropped -1.09%. Singapore Strait Times rose 0.06%. Japan 10-year JGB yield rose 0.0005 to 0.021.

Fed George maintained it’s a point to begin to ease up accommodation

Kansas City Fed President Esther George told Bloomberg that the spike in Covid is a “risk to the outlook”, but her contacts in the region said the economy “continues to grow at a strong rate”, consumers are “still spending” and labor markets is “continuing to heal”. The outlook “remains a positive one”. The virus is not expected to derail the economy”.

George also maintained that the progress the economy has made suggests “we’ve come to a point where we can begin to ease up on the amount of accommodation”. It’s “time to begin to make those adjustments” on asset purchases.

As policymakers are coming into the September meeting, she said, we will continue to talk about how the economy has unfolded and the timing for adjustments to those asset purchases”.

US initial jobless claims rose to 353k, slightly below expectation

US initial jobless claims rose 4k to 353k in the week ending August 21, slightly below expectation of 355k. Four-week moving average of initial claims dropped -11.5k to 366.5k, lowest since March 14.

Continuing claims dropped -3k to 2862k in the week ending August 14, lowest since March 14, 2020. Four-week moving average of continuing claims dropped -108.5k to 2901.5k, lowest since March 21, 2020.

US GDP grew 6.6% annualized in Q2, revised slightly up

According to the second estimate, US GDP grew an annual rate of 6.6% in Q2, revised up from 6.5%. The update reflects upward revisions to nonresidential fixed investment and exports that were partly offset by downward revisions to private inventory investment, residential fixed investment, and state and local government spending. Imports, which are a subtraction in the calculation of GDP, were revised down.

ECB accounts: Large majority of members see new forward guidance a fine balance

In the accounts of July 21-22 meeting, ECB said a “large majority” of the council members supported the forward guidance proposal, which was “widely seen as providing a fine balance between greater emphasis on outcome-based elements in the forward guidance and a more flexible, forward-looking perspective.”

However, “a few members upheld their reservations, as the amended formulation did not sufficiently address their concerns.”. This related in particular to the “implied likelihood and persistence of overshooting, and being seen as promising to keep interest rates at their present or lower levels for a very long time period without an explicit escape clause.”

ECB also said, the new forward guidance “underscored the Governing Council’s commitment to achieving its new inflation target”. It indicated that ECB would “wait until it was confident about the path of inflation before raising the key policy rates.” Nevertheless, the guidance is “not a rule” but “an indication to financial markets and the broader public” for aligning their inflation expectations.

Germany Gfk consumer sentiment dropped to -1.2, fear of tightened restrictions again

Germany Gfk consumer sentiment for September dropped from -0.4 to -1.2. In August, economic expectations dropped from 54.6 to 40.8. Income expectations rose from 29.0 to 30.5. Propensity to buy dropped from 14.8 to 10.3.

Rolf Bürkl, a GfK consumer expert, commented on this observation: “Significant higher incidence values, a slowdown in vaccination momentum, and discussions about how to deal with unvaccinated individuals in the future have caused noticeable uncertainty among consumers in Germany. They fear that restrictions could even be tightened again. This is obviously depressing consumer sentiment right now.”

Japan corporate services price rose 1.1% yoy in Jul, on transportation fees

Japan corporate services price index rose 1.1% yoy in July, below expectation of 1.3% yoy. The increase was driven by 1.4% rise in transportation fees, and in particular, with international freight costs up 24.6%. Meanwhile, hotel service fees rose 10.8%, highest in six years, reflecting the impact of the Tokyo Olympics.

“The recent increase in infections will weigh on services producer prices, though we could see service demand perk up if progress in vaccinations help re-open the economy,” said Shigeru Shimizu, head of the BoJ’s price statistics division.

Bank of Korea raises interest rate, embarking normalization process

Bank of Korea raised interest rate by 0.25% to 0.75% today, becoming the first major Asian economy to hike. “The Board will gradually adjust the degree of monetary policy accommodation as the Korean economy is expected to continue its sound growth and inflation to run above 2% for some time, despite ongoing uncertainties over the virus,” the BOK said in its monetary policy statement.

Governor Lee Ju-yeol said, “we’ve decided to put the focus on reducing financial imbalances, and as we raise the rate, we are embarking on a process of normalizing policy in line with economic recovery.”

BoK maintained its forecast of 4% GDP growth this year. Consumer inflation forecast was, however, upgraded from 1.8% to 2.1%.

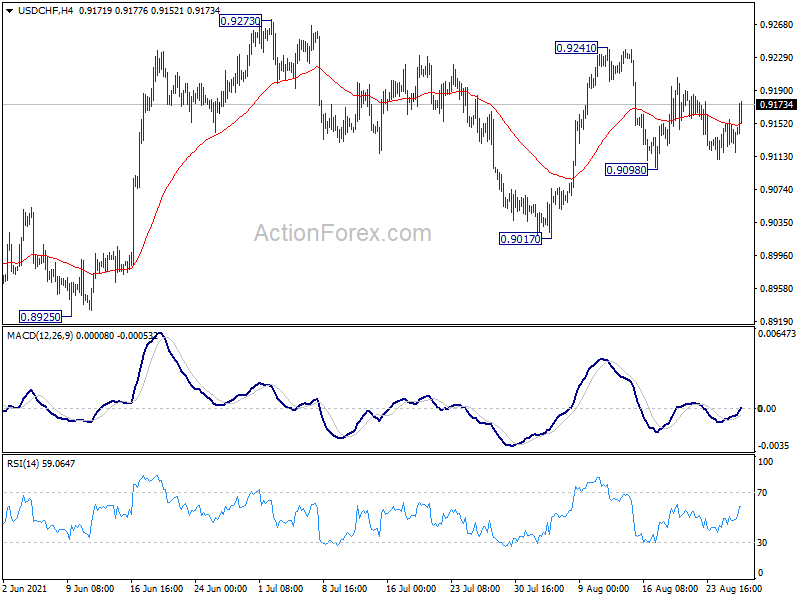

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9123; (P) 0.9140; (R1) 0.9156; More….

USD/CHF recovers today but stays well inside range of 0.9098/9241. Intraday bias remains neutral first. On the upside, break of 0.9241 resistance should resume the rise from 0.8925 through 0.9273. On the downside, break of 0.9098 will target 0.9017 support first. Further break there will likely resume the decline from 0.9471 through 0.8925 low.

{kind=link}

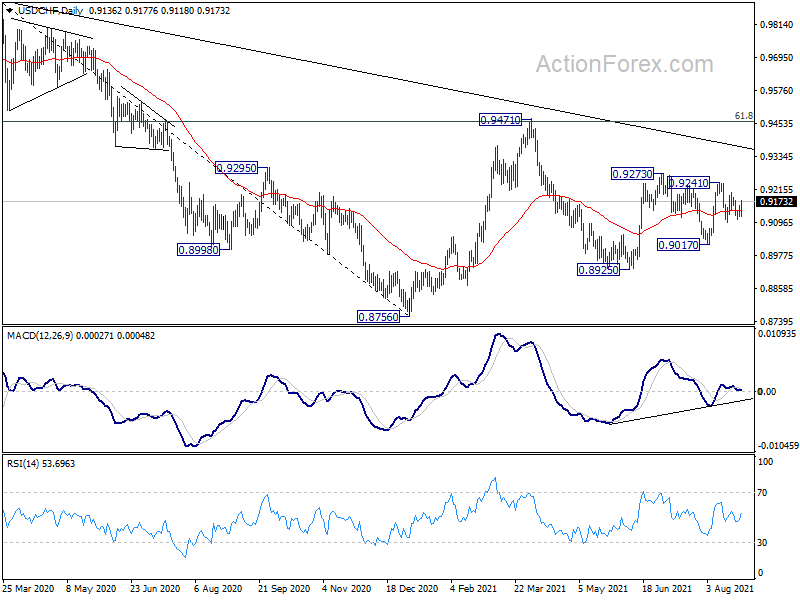

In the bigger picture, the failure to sustain above 55 week EMA (now at 0.9180) retains medium term bearishness in USD/CHF. Break of 0.8925 support should resume the whole decline form 1.0342 (2016 high) through 0.8756 low. However, break of 0.9273 resistance and sustained trading above 55 week EMA will be an early sign of bullish trend reversal. Focus will then turn to 0.9471 resistance for confirmation.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Jul | 1.10% | 1.30% | 1.40% | 1.30% |

| 01:30 | AUD | Private Capital Expenditure Q2 | 4.40% | 2.50% | 6.30% | 6.00% |

| 06:00 | EUR | Germany Gfk Consumer Confidence Sep | -1.2 | -1 | -0.3 | |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Jul | 7.60% | 7.60% | 8.30% | |

| 11:30 | EUR | ECB Monetary Policy Accounts | ||||

| 12:30 | USD | Initial Jobless Claims (Aug 20) | 353K | 355K | 348K | 349K |

| 12:30 | USD | GDP Annualized Q2 P | 6.60% | 6.70% | 6.50% | |

| 12:30 | USD | GDP Price Index Q2 P | 6.10% | 6.00% | 6.10% | |

| 14:30 | USD | Natural Gas Storage | 40B | 46B |