Euro and Swiss Franc rise broadly as the markets are approaching the weekly close. On the other hand, Canadian Dollar is reversing some of this week’s gains, while Dollar is following as second weakest for the day. As for the week, the Loonie is still the strongest, followed by Kiwi Swiss Franc is the weakest followed by Sterling. But there are still a few more hours to change the picture.

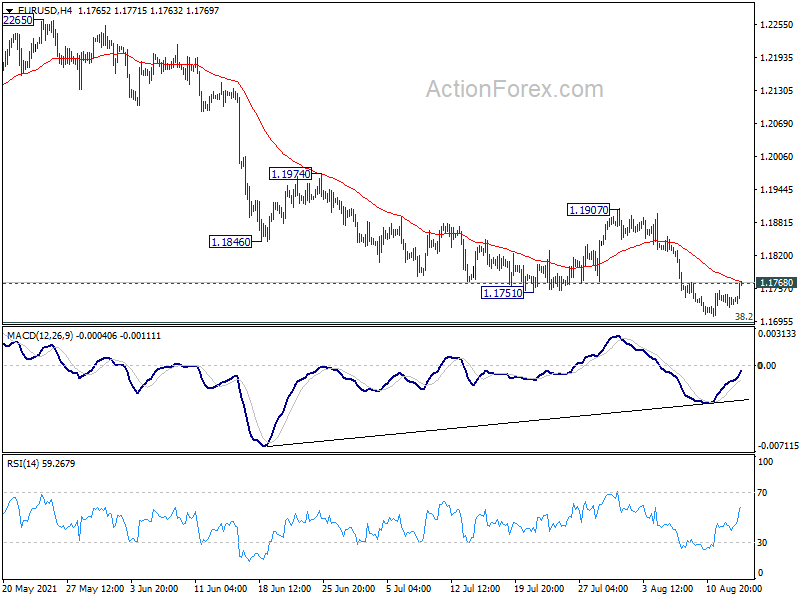

Technically, one major focus for the rest of the day and early next week is EUR/USD. Break of 1.1768 minor resistance will firstly indicate short term bottoming. More importantly, the could be an early sign of near term reversal, after drawing support from 1.1703 key near term support level. We’ll see if EUR/USD’s rebound would extend.

In Europe, at the time of writing, FTSE is up 0.40%. DAX is up 0.31%. CAC is up 0.27%. Germany 10-year yield is up 0.010 at -0.448. Earlier in Asia, Nikkei dropped -0.14%. Hong Kong HSI dropped -0.48%. China Shanghai SSE dropped -0.24%. Singapore Strait Times dropped -0.54%. Japan 10-year JGB yield dropped -0.0002 to 0.024.

Eurozone exports rose 23.8% yoy in Jun, imports rose 28.2% yoy

Eurozone exports to the rest of the world rose 23.8% yoy to EUR 209.9B in June. Imports from the reset of the world rose 28.2% yoy to EUR 191.8B. As a result, Eurozone record a EUR 18.1B surplus, comparing to EUR 20.0B a year ago. Intra-Eurozone trade rose 24.6% yoy to EUR 188.0B.

In seasonally adjusted terms, Eurozone exports dropped -0.1% mom to EUR 197.7B. Imports was nearly unchanged at EUR 185.3B. Trade surplus narrowed to EUR 12.4B, down from EUR 13.8B, above expectation of EUR 9.3B.

Also released in European session, Swiss PPI came in at 0.5% mom, 3.3% yoy, versus expectation of 0.3% mom, 2.8% yoy.

New Zealand BusinessNZ manufacturing rose to 62.6, second highest on record

New Zealand BusinessNZ Performance of Manufacturing Index rose from 60.9 to 62.6 in July. That’s the second highest reading after March’s 63.6. Looking at some details, production rose from 64.4 to 66.0.. Employment rose from 56.7 to 58.3, a new record. New orders rose from 63.6 to 65.0. Finished stocks dropped from 57.4 to 56.9. Deliveries rose from 55.2 to 57.9.

However, the position of negative comments (51.4%) still remained higher than positive ones (48.6%). Increased domestic and overseas orders was the common factor for positive comments. In contrast, tight labor market, supply chain issues and raw material costs were the negatives.

BNZ Senior Economist, Craig Ebert stated that “while New Zealand’s PMI is doing exceptionally well, we are also conscious of the headwinds happening for global manufacturing. This is on account of the resurgence of COVID19 in its delta strain.”

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1723; (P) 1.1735; (R1) 1.1747; More..

EUR/USD rebounds notably today and immediate focus is now on 1.1768 minor resistance. Firm break there will confirm short term bottoming and bring stronger rise to 1.1907 resistance. As by then, EUR/USD should have draw strong support from support from 1.1602/1703 support zone. Firm break of 1.1907 should indicate near term bullish reversal. Nevertheless, on the downside, sustained break of 1.1602 will argue that it’s already reversing the trend from 1.1603, and target 61.8% retracement of 1.1603 to 1.2348 at 1.1289.

{kind=link}

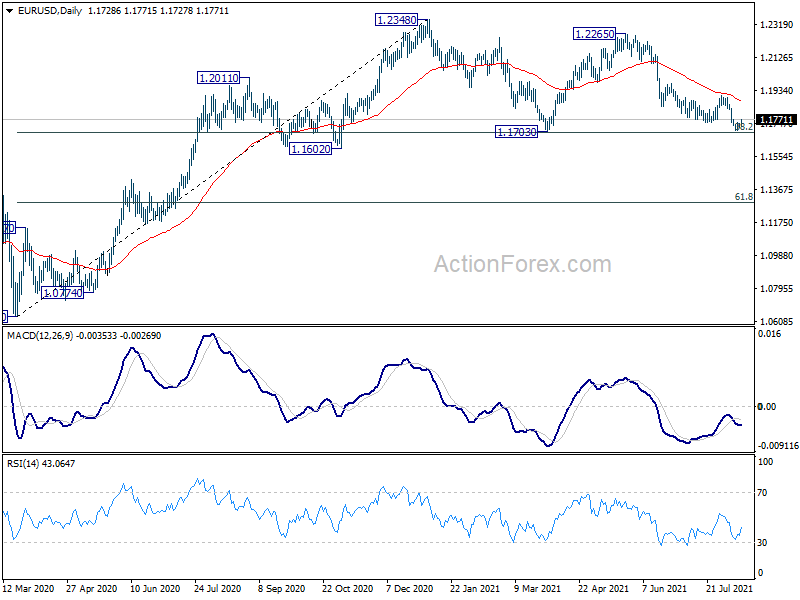

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally could be seen to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). This will remain the favored case as long as 1.1602 support holds. Reaction from 1.2555 should reveal underlying long term momentum in the pair. However sustained break of 1.1602 will argue that the rise from 1.0635 is over, and turn medium term outlook bearish again.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI Jul | 62.8 | 60.7 | 60.9 | |

| 06:30 | CHF | Producer and Import Prices M/M Jul | 0.50% | 0.30% | 0.30% | |

| 06:30 | CHF | Producer and Import Prices Y/Y Jul | 3.30% | 2.80% | 2.90% | |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Jun | 12.4B | 9.3B | 9.4B | 13.8B |

| 12:30 | USD | Import Price Index M/M Jul | 0.30% | 0.60% | 1.00% | |

| 14:00 | USD | Michigan Consumer Sentiment Index Aug P | 81.3 | 81.2 |