Dollar’s decline continues and accelerates a little in early US session after weak economic data. Gold is also accelerating upwards, in tandem with the greenback’s movements. Yen is following as second worst for now, following recovery in European stocks and US futures. Commodity currencies and Sterling are currently the stronger ones for today.

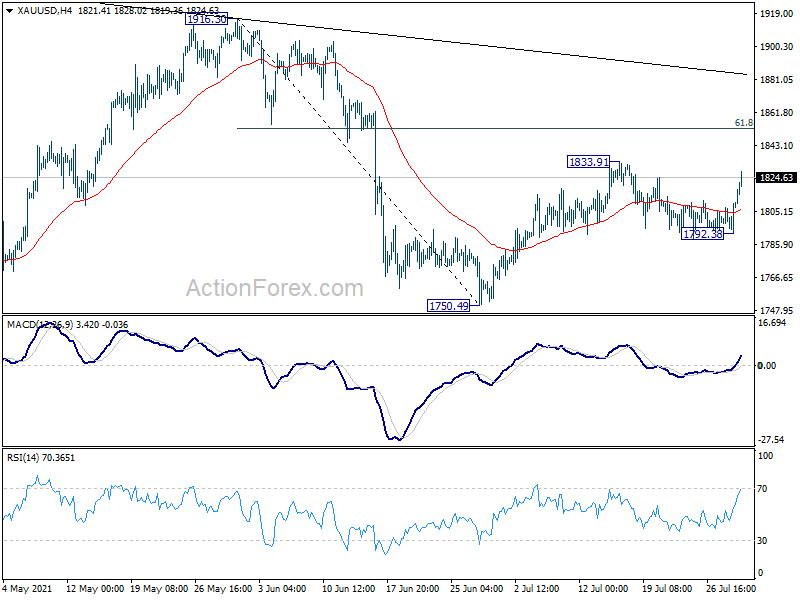

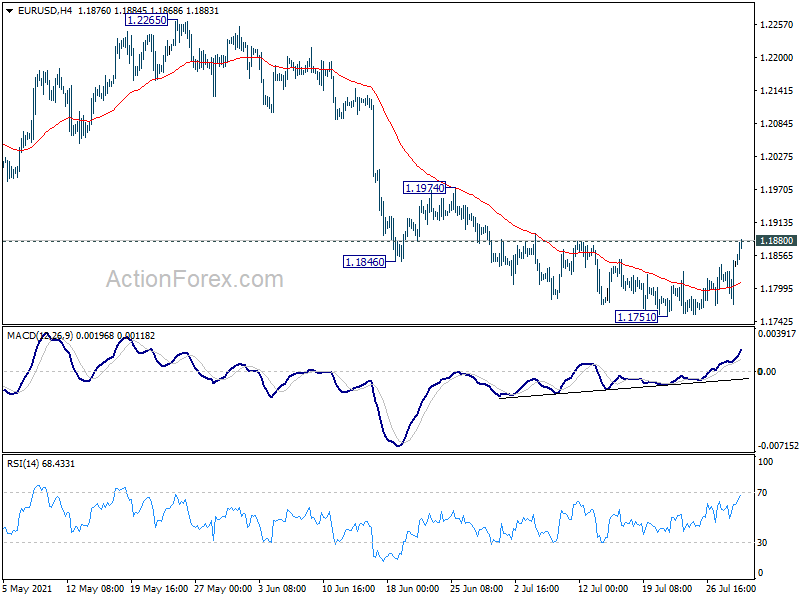

Technically, immediate focus is now on 1.1880 resistance in EUR/USD. Sustained break there should confirm short term bottoming at 1.1751. Further break of 1.1974 resistance will likely pave the way back to retest 1.2265/2348 resistance zone. At the same time, break of 1833.91 resistance in Gold will resume the rise from 1750.49 to 61.8% retracement of 1916.30 to 1750.49 at 1852.96 next. Both developments, if happen, will double confirm Dollar’s weakness.

{kind=link}

In Europe, at the time of writing, FTSE is up 0.92%. DAX is up 0.43%. CAC is up 0.72%. Germany 10-year yield is up 0.018 at -0.430. Earlier in Asia, Nikkei rose 0.73%. Hong Kong HSI rose 3.30%. China Shanghai SSE rose 1.49%. Singapore Strait Times rose 1.24%. Japan 10-year JGB yield rose 0.0057 to 0.022.

US GDP grew 6.5% annualized in Q2, missed expectations

US GDP grew at annual rate of 6.5% in Q2, well below expectation of 8.2%. BEA said: “The increase in real GDP in the second quarter reflected increases in personal consumption expenditures (PCE), nonresidential fixed investment, exports, and state and local government spending that were partly offset by decreases in private inventory investment, residential fixed investment, and federal government spending. Imports, which are a subtraction in the calculation of GDP, increased”.

US initial jobless claims dropped to 400k, worse than expected

US initial jobless claims dropped -24k to 400k in the week ending July 24, above expectation of 365k. Four-week moving average of initial claims rose 8k to 394.5k.

Continuing claims rose 7k to 3269k in the week ending July 17. Four-week moving average of continuing claims dropped -54k to 3291k, lowest since March 21, 2020.

Eurozone economic sentiment rose to record 119.0, strong industrial and services confidence

Eurozone Economic Sentiment Indicator rose to 119.0 in July, up from 11.79, above expectation of 118.8. That’s the highest level on record since 1985. Employment Expectations Indicator was flat at 111.7, well above pre-pandemic level.

Looking at some more details, Eurozone industrial confidence rose from 12.8 to 14.6, eighth straight month of improvement and an all-time high. Services confidence rose from 17.9 to 19.3, highest since 2007. Consumer confidence dropped from -3.3 to -4.4. Retail trade confidence dropped from 4.7 to 4.6. Construction confidence dropped from 5.2 to 4.0.

EU ESI rose 0.9 pts to 118.0. EEI was unchanged at 111.6. Amongst the largest EU economies, the ESI rose sharply in France (+4.0) and, to a lesser extent, in Italy (+1.7) and Spain (+1.7). Sentiment in Germany (+0.3) and the Netherlands (-0.3) stayed virtually unchanged, while it deteriorated mildly in Poland (-0.7).

New Zealand ANZ business confidence dropped to -3.8, time to start normalizing monetary conditions

New Zealand ANZ business confidence dropped from -0.6 to -3.8 in July. Own activity outlook also dropped from 31.6 to 26.3. Looking at some more details, expect intentions dropped from 13.4 to 7.6. Investment intentions dropped from 25.5 to 17.4. Employment intentions rose from 19.7 to 21.4. Cost expectations rose from 86.2 to 88.2. Pricing intentions dropped slightly from 62.8 to 61.3. Inflation expectations rebounded from 2.41 to 2.70.

ANZ said, “the combination of clear upside for the activity and inflation starting point, but downside risks in the (quite possibly not far off) future, do, on the face of it, present a conundrum for the Reserve Bank… “If they raise rates now, the odds are indeed uncomfortably high that they’ll end up reversing course before long… Inflation pressures provide an excellent reason to raise interest rates now, despite downside risks… inaction comes with risks too. It’s time to start normalising monetary conditions, even if trouble might lie closer ahead than we hope.”

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1795; (P) 1.1823; (R1) 1.1871; More…

Immediate focus is now on 1.1880 resistance in EUR/USD. Firm break there will firstly indicate short term bottoming at 1.1751, on bullish convergence condition in 4 hour MACD. Intraday bias will be turned back to the upside for 1.1974 resistance first. Sustained break there will argue that whole corrective pattern from 1.2348 has completed, and bring stronger rise back to 1.2265/2348 resistance zone. On the downside, break of 1.1751 will resume the fall from 1.2265, as the third leg of correction from 1.2348, to 1.1703 support.

{kind=link}

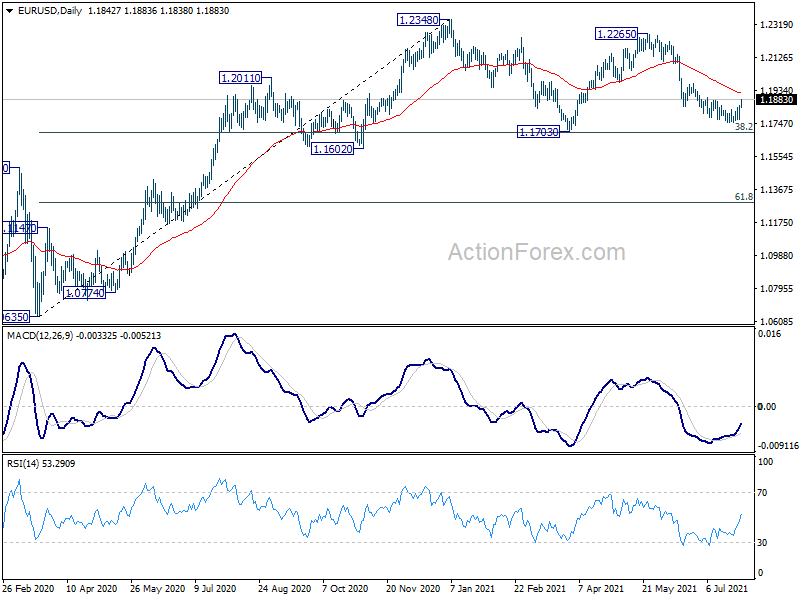

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally could be seen to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). This will remain the favored case as long as 1.1602 support holds. Reaction from 1.2555 should reveal underlying long term momentum in the pair. However sustained break of 1.1602 will argue that the rise from 1.0635 is over, and turn medium term outlook bearish again.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:00 | NZD | ANZ Business Confidence Jul | -3.8 | -0.6 | ||

| 01:30 | AUD | Import Price Index Q/Q Q2 | 1.90% | 0.20% | 0.20% | |

| 07:55 | EUR | Germany Unemployment Rate Jul | 5.70% | 5.80% | 5.90% | |

| 07:55 | EUR | Germany Unemployment Change Jul | -91K | -25K | -38K | |

| 08:30 | GBP | Net Lending to Individuals (GBP) Jun | 18.2B | 6.8B | 6.9B | 7.2B |

| 08:30 | GBP | Mortgage Approvals Jun | 81K | 85K | 88K | |

| 08:30 | GBP | M4 Money Supply M/M Jun | 0.50% | 0.30% | 0.40% | |

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Jul | 119 | 118.8 | 117.9 | |

| 09:00 | EUR | Eurozone Services Sentiment Jul | 19.3 | 19.5 | 17.9 | |

| 09:00 | EUR | Eurozone Industrial Confidence Jul | 14.6 | 13 | 12.7 | 12.8 |

| 09:00 | EUR | Eurozone Consumer Confidence Jul F | -4.4 | -4.4 | -4.4 | -3.3 |

| 12:00 | EUR | Germany CPI M/M Jul P | 0.90% | 0.50% | 0.40% | |

| 12:00 | EUR | Germany CPI Y/Y Jul P | 3.80% | 3.20% | 2.30% | |

| 12:30 | USD | Initial Jobless Claims (Jul 23) | 400K | 365K | 419K | 424K |

| 12:30 | USD | GDP Annualized Q2 P | 6.50% | 8.20% | 6.40% | |

| 12:30 | USD | GDP Price Index Q2 P | 6.10% | 5.40% | 4.30% | |

| 14:00 | USD | Pending Home Sales M/M Jun | 0.80% | 8.00% | ||

| 14:30 | USD | Natural Gas Storage | 41B | 49B |