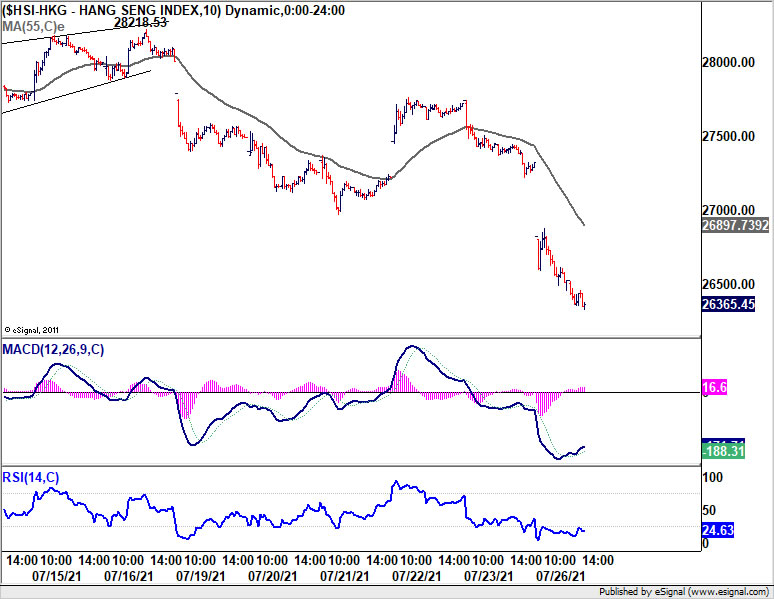

Yen and Swiss Franc are trading mildly higher as the week starts. Heavy selling is seen in stock markets in Hong Kong and China. Yet, Japan came back from holiday with mild gains. Commodity currencies are generally soft, with Aussie leading the way down. Dollar and Euro are mixed for the moment. A focus today is whether the selloff in Hong Kong would spillover to European and US markets later in the day.

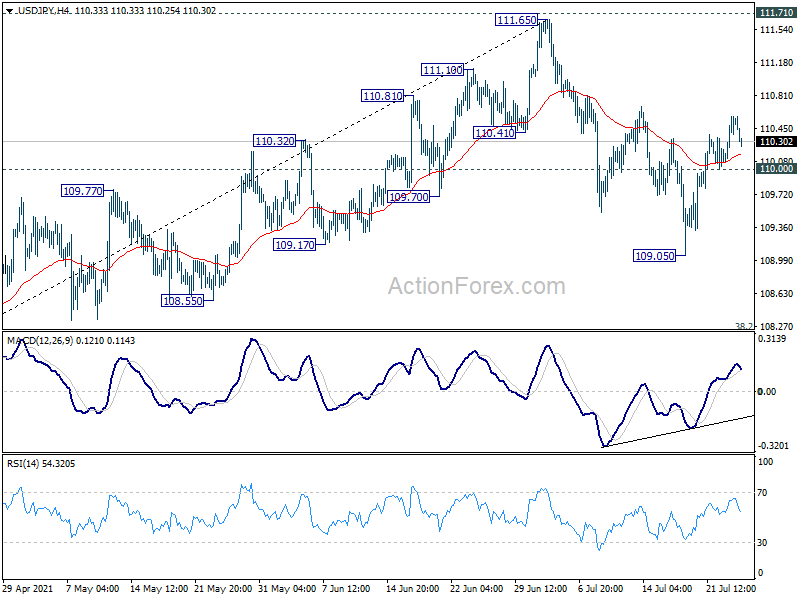

Technically, USD/JPY’s recovery form 109.05 is losing some upside momentum. But further rise is still likely as long as 110.00 minor support holds. However, break of 110.00 could be an indication of risk-aversion, which could be reflected in selling in other Yen crosses. We’ll keep an eye on it if happens.

{kind=link}

In Asia, Nikkei closed up 0.95%. Hong Kong HSI is down -3.22%. China Shanghai SSE is down -2.34%. Singapore Strait Times is down -0.57%. Japan 10-year JGB yield is down -0.0031 at 0.013.

{kind=link}

New Zealand goods exports rose 17% yoy in June, imports rose 24% yoy

New Zealand goods exports rose 17% yoy to NZD 6.0B in June. Goods imports rose 24% yoy to NZD 5.7B. Monthly trade balance reported NZD 261m surplus, slightly below expectation of NZD 297m.

Exports to all top trading partners were up, including China (40%), EU (21%), Australia (9.5%), Japan (13%) and US (2.9%). Imports from all top trading partners were up too, including EU (51%), China (17%), Japan (69%), USA (52%) and AU (18%).

Japan PMI manufacturing dropped to 52.2, services dropped to 46.4

Japan PMI Manufacturing dropped slightly from 52.4 to 52.2 in July, below expectation of 53.1. PMI Services dropped from 48.0 to 46.4. PMI Composite dropped from 48.9 to 47.7.

Usamah Bhatti, Economist at IHS Markit, said: “Flash PMI data indicated that Japanese private sector businesses saw a faster reduction in activity during July. Output fell at the quickest pace for six months, while the contraction in new business inflows was the fastest since February. Survey members attributed the deterioration in business conditions to persistent rises in COVID-19 cases and state of emergency measures which dampened activity and demand.”

Fed unlikely to hint on tapering schedule, lots of data to watch

FOMC meeting is a major highlight of the week. Just less than two week ago, Chair Jerome Powell told Congress that the economy is still “ways off” the substantial progress to start tapering asset purchases. Calls for stimulus withdrawal has somewhat eased too with fall in treasury yields and surge in delta variant infections. Powell could wait for the annual Jackson Hole symposium on August 26-28 to give more hints on Fed’s schedule. Or, that could be pushed even further to September meeting when new economic projections are available.

While Fed might turn out to be a non-mover to the markets, economic calendars are likely not. US GDP is another focus while durable goods orders, consumer confidence and PCE inflation could also trigger some volatility. Elsewhere, Japan PMI manufacturing and industrial production, Germany Ifo, Eurozone inflation and GDP, Canada GDP and CPI, Australia CPI, and New Zealand business confidence could also prompt some movements in respective currencies.

Here are some highlights for the week:

- Monday: New Zealand trade balance; Japan PMI manufacturing; Germany Ifo business climate; US new home sales.

- Tuesday: Japan corporate services prices; Eurozone M3 money supply; US durable goods orders, house price index, consumer confidence.

- Wednesday: BoJ summary of opinions; Australia CPI; Germany Gfk consumer confidence; Swiss ZEW expectations; US goods trade balance, FOMC rate decision; Canada CPI.

- Thursday: New Zealand ANZ business confidence; Australia import price; Germany unemployment, CPI flash; Eurozone economic sentiment; UK mortgage approvals, M4 money supply; US Q2 GDP, pending home sales.

- Friday: Japan unemployment rate, industrial production, retail sales, housing starts; Australia private sector credit, PPI; France consumer spending, GDP; Germany GDP; Italy GDP, CPI flash, unemployment rate; Swiss KOF economic barometer; Canada GDP, IPPI and RMPI; US personal income and spending, PCE inflation, employment cost index, Chicago PMI.

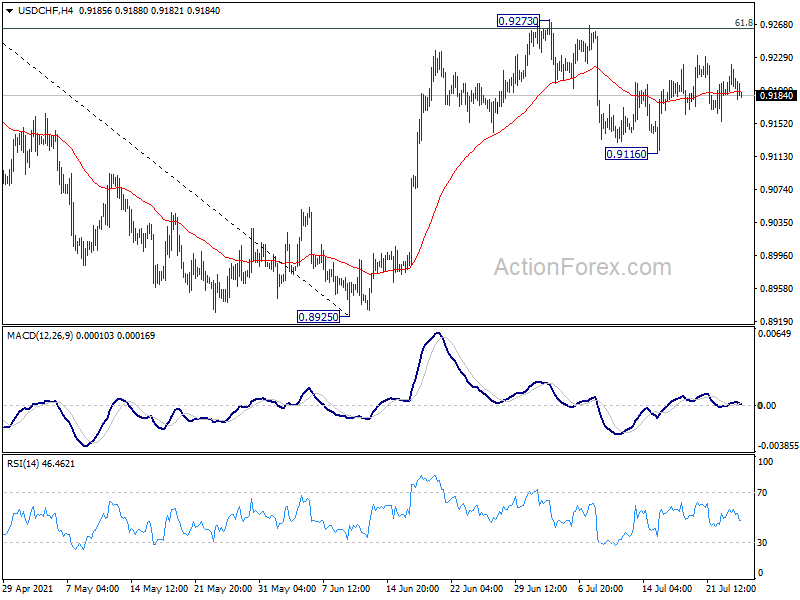

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9182; (P) 0.9202; (R1) 0.9217; More….

USD/CHF drops slightly today but stays in range of 0.9116/9273 and intraday bias remains neutral first. On the downside, break of 0.9116 support will affirm the case that rebound from 0.8925 has completed at 0.9273. Deeper fall would then be seen back to retest 0.8925 low. On the upside, however, break of 0.9273 and sustained trading above 61.8% retracement of 0.9471 to 0.8925 at 0.9262 will target 0.9471 resistance next.

{kind=link}

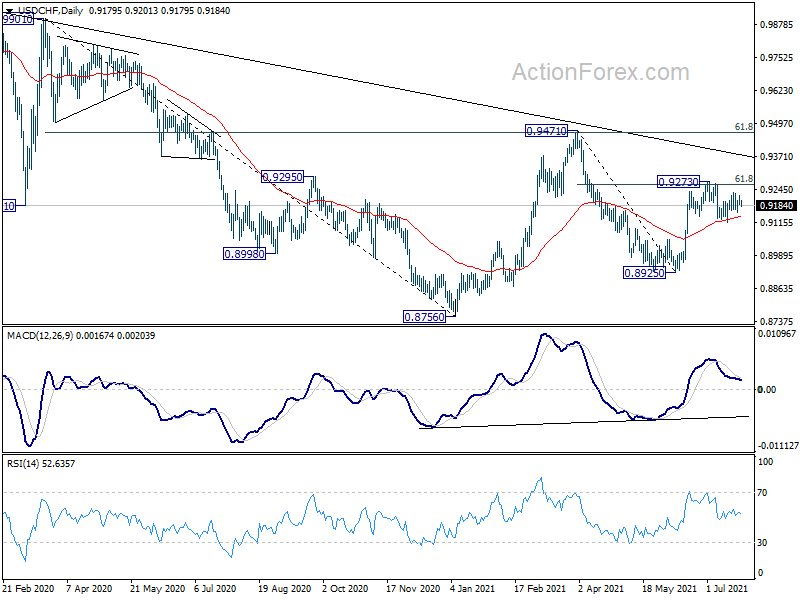

In the bigger picture, medium term outlook is currently neutral with focus on 0.9471 resistance. Sustained break there will indicate completion of whole decline from 1.0342 (2016 high). Medium term outlook will be turned bullish for a test on 1.0342 high. But, rejection by 0.9471 again will revive bearishness for another fall through 0.8756 low.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Jun | 261M | 469M | 489M | |

| 0:30 | JPY | Manufacturing PMI Jul P | 52.2 | 53.1 | 52.4 | |

| 8:00 | EUR | Germany IFO Business Climate Jul | 102.1 | 101.8 | ||

| 8:00 | EUR | Germany IFO Current Assessment Jul | 101.6 | 99.6 | ||

| 8:00 | EUR | Germany IFO Expectations Jul | 103.3 | 104 | ||

| 14:00 | USD | New Home Sales Jun | 800K | 769K |