Dollar regained some ground in European session, as assisted by mild pull back in stocks. The greenbacks stay firmer into US session as jobless claims data showed continuing improvement. Sterling is also stronger today after BoE policymaker Michael Saunders’ hawkish comments. On the other hand, commodity currencies are trading lower, as led by pull back in New Zealand Dollar. But overall, most pairs are just range bound, while a firm direction is awaited.

Technically, developments remain rather indecisive. We’ll keep an eye on commodity currencies today. USD/CAD might be trying to retest 1.2589 resistance as Dollar rebounds elsewhere. Break will resume whole rebound from 1.2005. Also, AUD/USD looks set to retest 0.7408 low. Firm break there will resume whole fall from 0.8006.

In Europe, at the time of writing, FTSE is down -0.69%. DAX is down -0.88%. CAC is down -0.74%. Germany 10-year yield is down -0.0068 at -0.326. Earlier in Asia, Nikkei dropped -1.15%. Hong Kong HSI rose 0.75%. China Shanghai SSE rose 1.02%. Singapore Strait Times dropped -0.42%. Japan 10-year JGB yield dropped -0.0061 to 0.014.

US initial jobless claims dropped to 360k, matched expectations

US initial jobless claims dropped -26k to 360k in the week ending July 10, matched expectations. That’s the lowest level since March 14, 2020. Four-week moving average of initial claims dropped -14.5k to 382.5k, lowest since March 14, 2020.

Continuing claims dropped -126k to 2341k in the week ending July 3, lowest since March 21, 2020. Four-week moving average of continuing claims dropped -72k to 3376k, lowest since March 21, 2020 too.

Also released, Empire State manufacturing index jumped to 43 in July, up from 17.4, above expectation of 19.2. But Philly Fed manufacturing survey dropped to 21.9, down from 30.7, missed expectation of 28.3.

BoE Saunders: Clear evidence that guidance conditions have been met

BoE MPC member Michael Saunders reiterated in a speech, “The Committee does not intend to tighten monetary policy at least until there is clear evidence that significant progress is being made in eliminating spare capacity and achieving the 2% inflation target sustainably.”

He added that these guidance conditions “have now been met”. There is “clear evidence” that GDP has “regained most of the lost ground in recent months”. Spare capacity in the labor market is “declining”. And the economy “continues to grow rapidly”. GDP is likely to regain pre-pandemic peak in the “next few months”.

Also, there is “clear evidence” that core inflation is “no longer below a target-consistent pace”, and it’s “likely to rise further in coming months”. This back drop meets the test of “significant progress in eliminating spare capacity and achieving the 2% inflation target sustainably.”

Even though the phrase “at least until” indicates these conditions are necessary but not sufficient for tightening. He said, “the guidance no longer rules out tightening.” Also, “the question of whether to curtail our current asset purchase program early will be under consideration at our forthcoming meetings”.

BoE Bailey won’t be rushed into rate hike despite higher inflation

BoE Governor Andrew Bailey admitted in an interview that yesterday’s inflation numbers were “higher than we thought it would be”. But the central bank won’t be rushed in to raising interest rates.

“What we will have to do, again, is go through all the evidence and assess to what extent we think the sorts of things that underlie that are likely to be transitory,” he added. “And to what extent is it going to cause second round effects – so it starts to get embedded in expectations and it gets into wage negotiations and it’s difficult to get out (of an inflationary cycle).”

In reaction to people who said that BoE is being “casual” about the surge in inflation, he emphasized, “we’re not at all actually.” “The committee has been very clear – if we think the case is made, then of course, we will respond and use the policy tools. We must do that.”

UK employment back above pre-pandemic levels in some regions

UK employment rose another 356k in June to 28.9m, but remains -206k below pre-pandemic levels. Nevertheless, employment in some regions, including North East, North West, East Midlands and Norther Ireland, were already back above pre-pandemic levels. Claimant count dropped -114.7k in June.

Employment rate was at 74.8%, -1.8% below pre-pandemic levels. unemployment rate edged up to 4.8% in May, above expectation of 4.7%. That’s also still 0.9% higher than before the pandemic.

Average earnings including bonus rose 7.3% 3moy in May, above expectation of 7.2% 3moy. Average earnings excluding bonus rose 6.6% 3moy, matched expectations.

ECB Visco: No tapering before the time comes

ECB Governing Council member Ignazio Visco told Bloomberg that, “we have to avoid tapering before the time comes that we’re really confident we’re back where we should.” He emphasized, “we really have to show to be determined”.

“Financial conditions are to remain favorable even if we have signs of some price increases that are above the target that the central banks have set,” he said.

“I don’t expect monetary policy to be tightened for a long period,” Visco added, as there is still “substantial slack” in the economy. Also, there are risks of another wave of coronavirus infections. Nevertheless, there is no discussion on extending the PEPP beyond end date in March.

Australia unemployment rate dropped to 4.9%, lowest since 2010

Australia employment grew 29.1k in June, or 0.2% mom, above expectation of 20.3k. Full time jobs grew 51.6k while part-time jobs dropped -22.5k. Over the year, employment grew 777.9k, or 6.3% yoy. Unemployment rate dropped -0.2% to 4.9%, better than expectation of 5.0%. Participation rate was unchanged at 66.2%.

Bjorn Jarvis, head of labour statistics at the ABS, said June saw the eighth consecutive monthly fall in the unemployment rate. “The unemployment rate fell to 4.9 per cent in June. This was 0.4 percentage points below March 2020 (5.3 per cent) and the lowest it has been since December 2010. The declining unemployment rate continues to coincide with employers reporting high levels of job vacancies and difficulties in finding suitable people for them,” Jarvis said.

China recovery slowed in June, but momentum still strong

China GDP grew 1.3% qoq in Q2, matched expectations. Industrial production growth slowed to 8.3% yoy in June, but beat expectation of 7.9% yoy. Retail sales growth slowed to 12.1% yoy, above expectation of 11.0% yoy. Fixed asset investment growth slowed to 12.6% ytd yoy, above expectation of 12.5% yoy. While growth momentum appears to be slowing, recovery is still very strong.

Hong Kong HSI rises in response to the solid data from China, and it’s trading up more than 1% at the time of writing. Notable support was seen from 26782.61 resistance turned support after last week’s spike low. Focus is back on 55 day EMA (now at 28484.00). Sustained break there will argue that correction from 31183.35 has completed and would bring retest of this high.

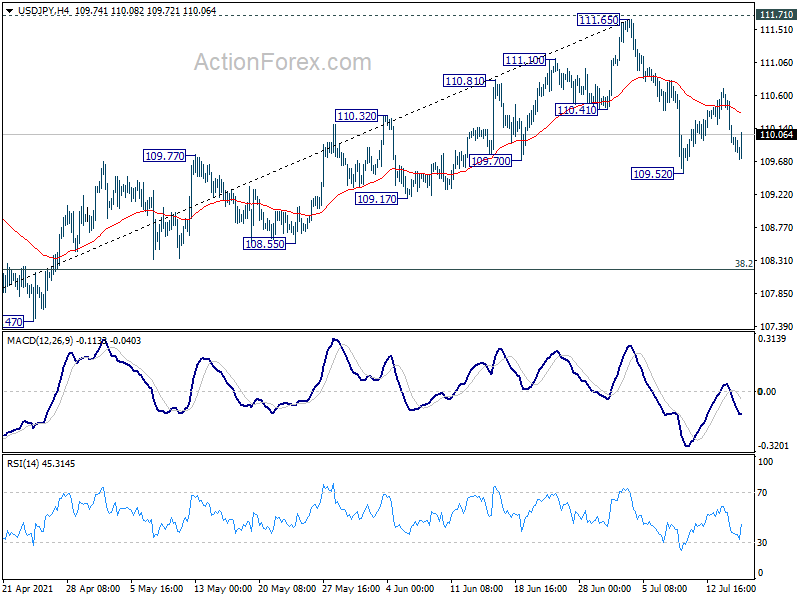

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.69; (P) 110.19; (R1) 110.45; More…

USD/JPY recovers mildly but stays in established range. Intraday bias remains neutral first. Also, risk stays mildly on the downside with 111.65 resistance intact. On the downside, break of 109.52, and sustained trading below 55 day EMA (now at 109.85) will suggest that it’s at least correcting the rise from 102.58. Deeper fall would be seen to 38.2% retracement of 102.58 to 111.65 at 108.18 next.

{kind=link}

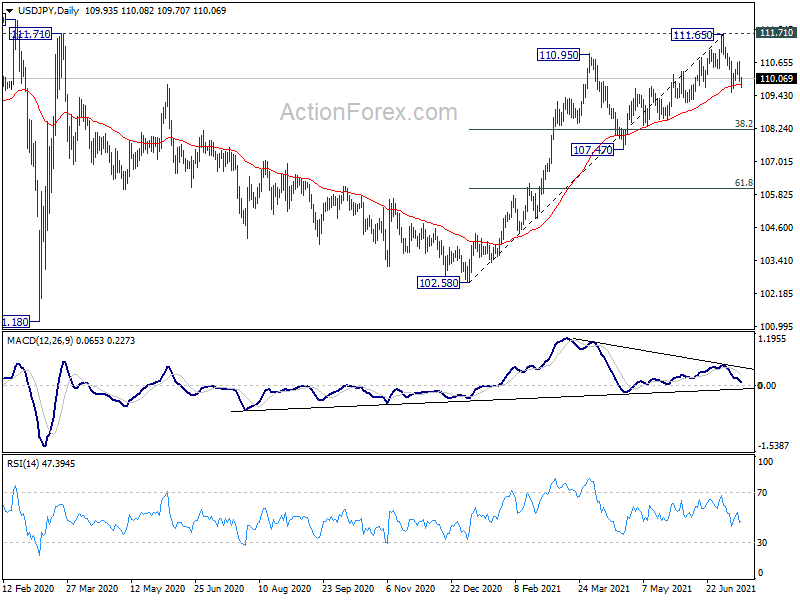

In the bigger picture, medium term outlook is staying neutral with 111.71 resistance intact. Though, as notable support was seen from 55 day EMA, rise from 102.58 is mildly in favor to extend higher. Decisive break of 111.71/112.22 resistance will suggest long term bullish reversal. Rise from 101.18 could then target 118.65 resistance (Dec 2016) and above. However, sustained break of 55 day EMA would revive some medium term bearishness, and open up deep fall back towards 102.58 support.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:00 | AUD | Consumer Inflation Expectations Jul | 3.70% | 4.40% | ||

| 01:30 | AUD | Employment Change Jun | 29.1K | 20.3K | 115.2K | |

| 01:30 | AUD | Unemployment Rate Jun | 4.90% | 5.00% | 5.10% | |

| 02:00 | CNY | Retail Sales Y/Y Jun | 12.10% | 11.00% | 12.40% | |

| 02:00 | CNY | Industrial Production Y/Y Jun | 8.30% | 7.90% | 8.80% | |

| 02:00 | CNY | Fixed Asset Investment (YTD) Y/Y Jun | 12.60% | 12.50% | 15.40% | |

| 02:00 | CNY | GDP Q/Q Q2 | 1.30% | 1.30% | 0.60% | |

| 02:00 | CNY | GDP Y/Y Q2 | 7.90% | 8.10% | 18.30% | |

| 04:30 | JPY | Tertiary Industry Index M/M May | -2.70% | -0.90% | -0.70% | |

| 06:00 | GBP | Claimant Count Change Jun | -114.7K | -92.6K | -151.4K | |

| 06:00 | GBP | ILO Unemployment Rate (3M) May | 4.80% | 4.70% | 4.70% | |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y May | 7.30% | 7.20% | 5.60% | 5.70% |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y May | 6.60% | 6.60% | 5.60% | 5.70% |

| 12:30 | CAD | ADP Employment Change Jun | -294.2K | 101.6K | -318.7K | |

| 12:30 | USD | Initial Jobless Claims (Jul 9) | 360K | 360K | 373K | 386K |

| 12:30 | USD | Import Price Index M/M Jun | 1.00% | 1.00% | 1.10% | |

| 12:30 | USD | Empire State Manufacturing Index Jul | 43 | 19.2 | 17.4 | |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Jul | 21.9 | 28.3 | 30.7 | |

| 13:15 | USD | Industrial Production M/M Jun | 0.70% | 0.80% | ||

| 14:30 | USD | Natural Gas Storage | 45B | 16B |