Canadian Dollar is steady after BoC delivered its sixth consecutive rate cut, lowering its policy rate by 25bps to 3.00% as expected. The pace of easing has slowed from December’s 50bps reduction, reflecting a more measured approach as interest rate sits inside neutral zone. BoC explicitly warned of risks stemming from potential US tariffs, noting that a prolonged trade conflict could weigh on economic growth while simultaneously exerting upward pressure on inflation.

Governor Tiff Macklem reinforced this concern in his press conference, describing US trade policy as a “major source of uncertainty,” with multiple possible outcomes. He also noted that tariffs reduce economic efficiency and cannot be offset by monetary policy alone, adding that with only one policy tool—the interest rate—the BoC cannot simultaneously combat “weaker output and higher inflation.”

Attention now shifts to Fed, which is widely expected to hold its policy rate steady at 4.25–4.50% today. The key question is whether Fed will signal an extended pause in its rate-cutting cycle, either through its statement or Chair Jerome Powell’s press conference. Powell’s tone will be crucial in shaping market expectations—any indication of a prolonged pause could bolster the Dollar and weigh on risk assets, while a more dovish stance could encourage renewed risk-taking.

In equities, DOW’s response to FOMC decision will be closely watched. The index has remained resilient despite this week’s tech sector volatility and is now approaching the record high of 45073.63.

Decisive break above this level would confirm long-term uptrend resumption, and target 61.8% projection of 38499.27 to 45073.63 from 41844.89 at 45907.85. In this bullish scenario, risk-on sentiment could spread to other sectors and take S&P 500 and NASDAQ higher too.

However, break of 44026.27 support will delay the bullish case and bring another fall to extend the consolidation from 45073.63 instead.

Overall in the currency markets, Yen is trading as the strongest for the week so far, followed by Dollar and then Swiss Franc. Aussie is the worst, followed by Kiwi, and then Euro. Sterling and Loonie are positioning in the middle.

BoC cuts rates to 3.00%, flags trade risks and ends QT

BoC lowered its overnight rate target by 25bps to 3.00% as widely expected. In accompanying statement, the central bank warned that a prolonged trade conflict with the US could strain economic growth and drive inflation higher.

BoC noted that “if broad-based and significant tariffs were imposed, the resilience of Canada’s economy would be tested.” Policymakers emphasized that they will closely monitor trade developments and assess their impact on economic activity, inflation, and future policy decisions.

The updated projections suggest a modest recovery in economic growth. Following an estimated 1.3% expansion in 2024, GDP is now expected to grow by 1.8% in both 2025 and 2026, slightly exceeding potential growth. Inflation is projected to remain near the 2% target over the next two years, reinforcing expectations that BoC will maintain a cautious approach to policy easing.

The central bank also announced plans to complete the normalization of its balance sheet by ending quantitative tightening. BoC will restart asset purchases in early March, adopting a gradual pace to ensure balance sheet stabilization while aligning with economic growth.

German Gfk consumer sentiment falls to -22.4, recovery hopes fade

Germany’s GfK Consumer Sentiment Index for February fell to -22.4, down from -21.4 and missing expectations of -20.5.

In January, economic expectations dropped by 1.9 points to -1.6, while income expectations declined by 2.5 points to -1.1. The most concerning development came from willingness to buy, which fell 3 points to -8.4, its lowest level since August 2024,.

Rolf Bürkl, consumer expert at NIM, noted that “the Consumer Climate has suffered another setback and starts gloomy into the new year.”

The moderate optimism seen in late 2024 has faded, with Bürkl adding that the trend since mid-2024 has been stagnation at best. A key concern is inflation, which has recently picked up again, limiting prospects for a meaningful rebound in consumer demand.

Australia’s CPI slows to 2.4% in Q4, trimmed mean CPI down to 3.2%

Australia’s Q4 CPI rose just 0.2% qoq, same as the prior quarter, falling short of expectations of 0.4% yoy. Trimmed mean CPI also undershot forecasts, rising 0.5% qoq versus the expected 0.6% qoq.

On an annual basis, headline CPI slowed from 2.8% yoy to 2.4% yoy, slightly below 2.5% yoy consensus. Trimmed mean CPI fell from 3.6% yoy to 3.2% yoy, missing 3.3% yoy estimate.

These weaker inflation prints reinforce expectations that RBA may begin easing policy as early as its February 17-18 meeting.

The decline in annual inflation was largely driven by steep drops in electricity prices (-25.2%) and automotive fuel (-7.9%). Goods inflation slowed sharply to 0.8% yoy, down from 1.4% yoy in Q3. Meanwhile, services inflation remained elevated at 4.3% yoy, though slightly lower than the 4.6% yoy in the previous quarter.

In December, monthly CPI rebounded from 2.3% yoy to 2.5% yoy, matched expectations.

RBNZ’s Conway sees cautious OCR path to neutral

RBNZ Chief Economist Paul Conway stated in a speech today that Official Cash Rate at 4.25% remains “north of neutral”. The central bank estimates the neutral rate between 2.5% and 3.5%.

“Easing domestic pricing intentions and the recent drop in inflation expectations help open the way for some further easing,” Conway added.

However, Conway emphasized a cautious approach, noting that policymakers will “feel our way” as rates approach neutral. RBNZ will continuously reassess its neutral rate estimate, adjusting based on economic conditions.

If neutral is underestimated, stronger-than-expected activity and inflation would signal a less restrictive policy than intended, prompting recalibration, he added.

The central bank expects potential output growth to range between 1.5% and 2% annually over the next three years, reflecting a lower economic “speed limit.” This weaker outlook stems from sluggish productivity and reduced net immigration, limiting long-term economic capacity.

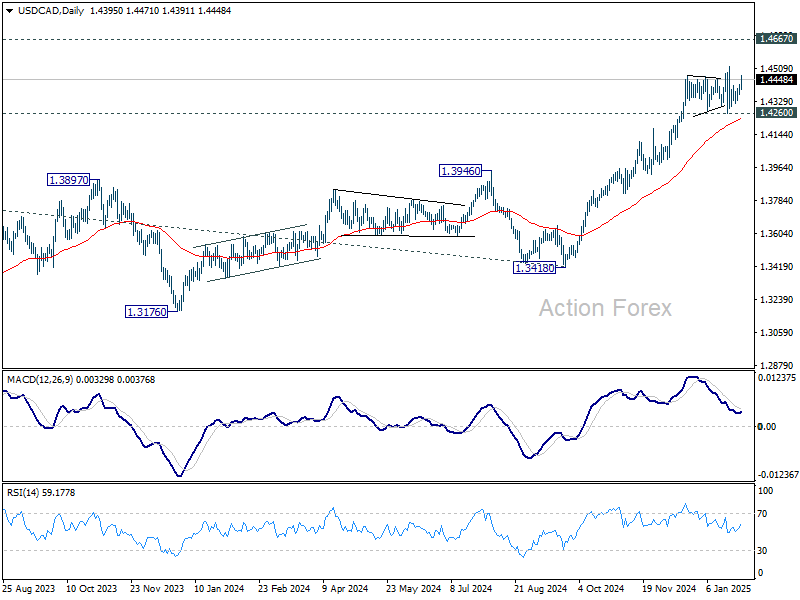

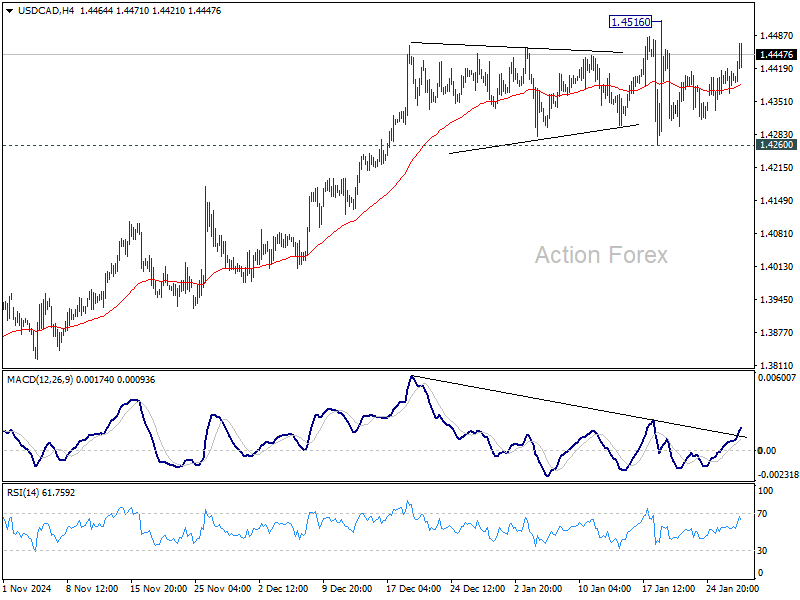

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.4367; (P) 1.4394; (R1) 1.4428; More…

USD/CAD rebounded notably today but stays in range below 1.4516 short term top. Intraday bias remains neutral and more consolidations could be seen. Further rally is expected as long as 1.4260 support holds. On the upside, firm break of 1.4516 will resume larger up trend to 1.4667/89 key resistance zone. Nevertheless, firm break of 1.4260 will turn bias to the downside for deeper pullback to 55 D EMA (now at 1.4235) and below.

In the bigger picture, up trend from 1.2005 (2021) is in progress for retesting 1.4667/89 key resistance zone (2020/2015 highs). Decisive break there will confirm long term up trend resumption. Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. Medium term outlook will remain bullish as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.