The global financial markets are finding their footing following the turmoil triggered by yesterday’s tech-driven selloff. European stocks have moved into positive territory, while US futures signal a flat start to trading. Nvidia, which lost a staggering -17% on Monday—erasing nearly USD 600B in market capitalization—is poised for a partial rebound. Meanwhile, investors appear to have shrugged off US durable goods orders data, which showed a sharp contraction, as the weakness was primarily attributed to volatile transportation equipment orders rather than broader economic concerns.

From a technical perspective, NASDAQ’s sharp decline appears to be merely a part of the ongoing consolidation from its record high of 20204.58. Volatility of this nature is not unusual during such phases. For now, more sideway trading is likely and deeper pull back might be seen. But downside should be contained by 38.2% retracement of 15708.53 to 20204.58 at 18787.09 to bring rebound, and then up trend resumption.

In the currency markets, Dollar is the day’s strongest performer so far, supported by ongoing tariff discussions. It is followed by Loonie and then Swiss Franc. On the other hand, Aussie is the weakest with anticipation ahead of critical inflation data. Kiwi and Euro are also under pressure, with the latter impacted by weak German business climate data and concerns about prolonged structural economic challenges in Europe. Sterling and the Swiss Franc are sitting in the middle of the pack.

Attention is now shifting to Australia’s CPI release in the upcoming Asian session, which could heavily influence expectations for RBA’s February 17-18 policy meeting. Quarterly inflation is forecast to slow from 2.8% yoy to 2.5%, while the monthly CPI reading is expected to show an uptick from 2.3% to 2.5%. Money markets currently assign an 80% probability to an RBA rate cut in February. However, a meaningful decline in trimmed mean CPI, from 3.5% to 3.3% or lower, should be needed to provide RBA with sufficient confidence to begin easing.

AUD/JPY will be a focal point for traders reacting to Australia’s inflation data. Repeated rejection by falling 55 D EMA is keeping near term outlook bearish. Break of 96.05 support will suggest that decline from 102.39, as the second leg of the corrective pattern from 90.10, is resuming. Next target is 61.8% retracement of 90.10 to 102.39 at 94.79.

US durable goods orders down -2.2% mom, driven by transportation equipment

US durable goods orders fell -2.2% mom to USD 276.1B, much worse than expectation of 0.8% mom. Transportation equipment, down four of the last five months, drove the decrease, down by -7.4% mom to USD 86.1B.

Ex-transport orders rose 0.3% mom to USD 189.9B, slightly below expectation of 0.4% mom. Ex-defense orders fell -3.1% om to USD 258.2B.

Germany faces deep economic crisis amid structural weakness, BDI Warns

Germany’s economic challenges were laid bare today as BDI President Peter Leibinger warned of a “deep economic crisis” during the annual press conference.

The country’s economic output is expected to shrink slightly this year, with Leibinger emphasizing that the situation reflects more than just short-term shocks like the pandemic or the war in Ukraine.

Instead, he highlighted long-term “structural” weaknesses that have plagued Germany as a business hub, particularly over the past six years.

Leibinger pointed to the “structural break” in industrial growth, with empty order books, idle machinery, and a marked decline in domestic investments.

His remark, “I cannot remember such a bad mood in industrial companies,” underscores the deep malaise gripping the sector.

German industry is not only struggling to compete globally against powers like the US and China but is also falling behind within the European Union.

Australia NAB business confidence rises to -2, price pressures persist

Australia’s NAB Business Confidence showed slight improvement in December, rising from -3 to -2, but remains below the long-term average since early 2023. Business Conditions, on the other hand, posted a stronger gain, climbing from 3 to 6.

Breaking down the details, trading conditions improved from 6 to 9, profitability rose from 0 to 4, and employment conditions ticked up from 3 to 4.

Price pressures continue to persist, with purchase cost growth rising slightly to 1.5% in quarterly equivalent terms. Labour cost growth edged lower to 1.4%, but output price growth increased by 0.3 percentage points to 0.9%. Retail prices also ticked up to 0.7%.

According to NAB Chief Economist Alan Oster, “The uptick in purchase cost growth and final product prices reminds us that businesses continue to face some price pressures.”

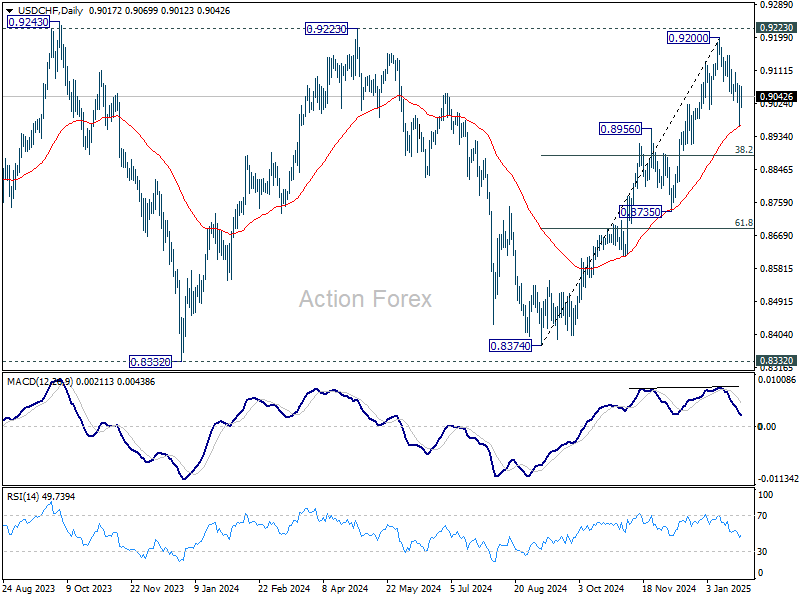

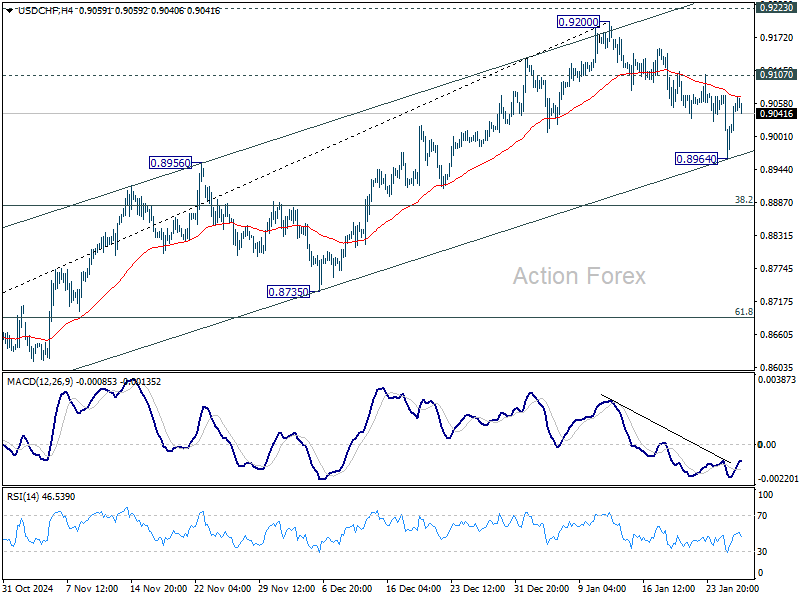

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8966; (P) 0.9019; (R1) 0.9074; More…

Intraday bias in USD/CHF remains neutral for the moment. Rise from 0.9374 remains intact so far with strong support support seen from near term rising channel. On the upside, break of 0.9107 will target 0.9200 and 0.9223 key resistance. On the downside, however, break of 0.8964 will resume the fall from 0.9200 to 38.2% retracement of 0.8374 to 0.9200 at 0.8884 next.

In the bigger picture, as long as 0.9223 resistance holds, price actions from 0.8332 (2023 low) are seen as a medium term corrective pattern. That is, long term down trend is in favor to resume through 0.8332 at a later stage. However, sustained break of 0.9223 will be an important sign of bullish trend reversal.