Forex markets have settled into quieter trading as the immediate impact of US President Donald Trump’s inauguration and initial executive orders fades. While Trump’s proposed tariffs remain a significant concern, their delayed implementation suggests a more calculated and strategic approach, tied to future negotiations. This tempered stance has brought a sense of cautious optimism to the markets, as the eventual impact may not be as severe as initially feared—especially if major agreements are reached with key allies like the EU.

Despite this relative calm, Canadian Dollar remains under significant pressure. As the most immediate target of Trump’s tariff agenda, with measures likely set to take effect on February 1. Loonie’s recovery struggled to gain traction. This weakness has been compounded by softer-than-expected Canadian CPI data for December. While energy prices saw a boost due to base effects, other areas of the economy, such as food and restaurant pricing, contributed to the overall deceleration in inflation. With inflation hovering near the 2% target, BoC is expected to continue easing monetary policy, albeit at a slower pace.

So far this week, Dollar has been the weakest performer, followed by Loonie and Yen. On the other side of the spectrum, Kiwi leads the gainers, followed by Euro and Sterling. Swiss Franc and Australian Dollar are positioned more neutrally, sitting in the middle of the performance table.

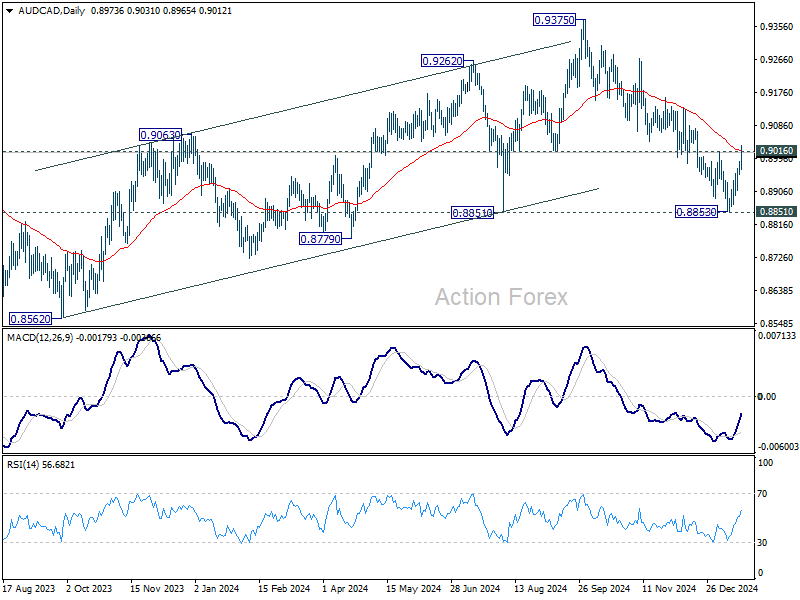

Technically, AUD/CAD’s rebound extended this week on Loonie’s weakness. It’s now pressing 0.9016 resistance and 55 D EMA. Sustained break there would argue that 0.8851 support was successfully defended, and corrective rally from 0.8562 (2023 low) remains intact. Further rise should then be seen back to retest 0.9375 high.

In Europe, at the time of writing, FTSE is up 0.09%. DAX is down -0.09%. CAC is up 0.18%. UK 10-year yield is down -0.053 at 4.610. Germany 10-year yield is down -0.011 at 2.518. Earlier in Asia, Nikkei rose 0.32%. Hong Kong HSI rose 0.91%. China Shanghai SSE fell -0.05%. Singapore Strait Times fell -0.33%. Japan 10-year JGB yield fell -0.0073 to 1.190.

Canada’s Inflation Slows to 1.8% in Dec Amid Food Price Decline

Canada’s annual inflation rate eased to 1.8% yoy in December, down from 1.9% yoy in November and slightly below expectations of 1.9% yoy. The deceleration was largely driven by declines in food prices and alcohol-related expenses.

Canadians paid 1.6% less for food purchased from restaurants on a year-over-year basis, marking the first annual decline in this index. Excluding food, CPI rose by 2.1% yoy.

Gasoline prices, for example, rose 3.5% yoy in December, reversing a -0.5% yoy decline in November. The increase was attributed to a base-year effect, as December 2023 saw a sharp -4.4% monthly decline due to concerns about oil demand amid high supply levels. However, on a month-over-month basis, gasoline prices edged down by -0.6% mom.

Looking at the core measures, CPI median slowed from 2.6% yoy to 2.4% yoy versus expectation of 2.5% yoy. CPI trimmed slowed from 2.6% yoy to 2.5% yoy, matched expectations. CPI common was unchanged at 2.0% yoy, above expectation 1.9% yoy.

German ZEW falls to 10.3 as Eurozone shows relative resilience

German ZEW Economic Sentiment fell sharply in January, dropping from 15.7 to 10.3 and missing market expectations of 15.1. In contrast, Current Situation Index showed slight improvement, rising from -93.1 to -90.4, slightly better than forecasts of -93.0.

Meanwhile, Eurozone ZEW Economic Sentiment painted a more optimistic picture, climbing from 17.0 to 18.0, exceeding expectations of 16.9. Current Situation Index for the Eurozone also rose, gaining 1.2 points to -53.8.

ZEW President Achim Wambach attributed the decline in Germany’s sentiment to persistent economic headwinds. He noted, “The second consecutive year of recession caused economic expectations in Germany to fall.”

Key factors include weak private household spending and low demand in the construction sector. Wambach warned that if these trends persist, “Germany will fall further behind the other countries of the Eurozone.”

Adding to the challenges, Wambach highlighted growing political uncertainty in Germany due to the complexities of coalition-building and the unpredictability of economic policies under the new Trump administration in the US.

UK payrolled employment falls -47k in Dec, unemployment rate rises to 4.4% in Nov

UK payrolled employment fell -47k or -0.2% mom in December. Median monthly pay rose 5.6% yoy, down from 6.4% yoy in November and 7.9% yoy in October. Claimant count rose 0.7k, below expectation of 10.3k.

In the three months to November, unemployment rate ticked up to 4.4%, above expectation of 4.3%. Average earnings excluding bonus rose 5.6% yoy, up from 5.2% yoy, and above expectation of 5.5% yoy. Average earnings including bonus rose 5.6% yoy, up from 5.2% yoy, matched expectations.

NZ BNZ services fall to 47.9, contracts for 10th month

New Zealand’s BNZ Performance of Services Index declined from 49.1 to 47.9 in December, well below historical average of 53.1. This also marks the 10th consecutive month of contraction.

The breakdown of the data highlights broad weakness: activity/sales fell from 48.3 to 46.2, and supplier deliveries dropped sharply from 52.5 to 47.7. New orders/business remained stagnant at 49.5, just below the threshold for expansion, while employment showed a marginal improvement, rising from 46.7 to 47.4. Stocks/inventories also slipped into contraction territory, falling from 52.0 to 48.8.

Negative sentiment among respondents increased to 57.5% in December, up from 53.6% in November, with cost-of-living pressures and concerns about the general economic climate dominating feedback.

BNZ’s Senior Economist Doug Steel remarked, “Comparing across our key trading partners, New Zealand has the only PSI in contraction. Our neighbour Australia is the closest comparison, but their equivalent PSI is sitting more comfortably at 50.8.”

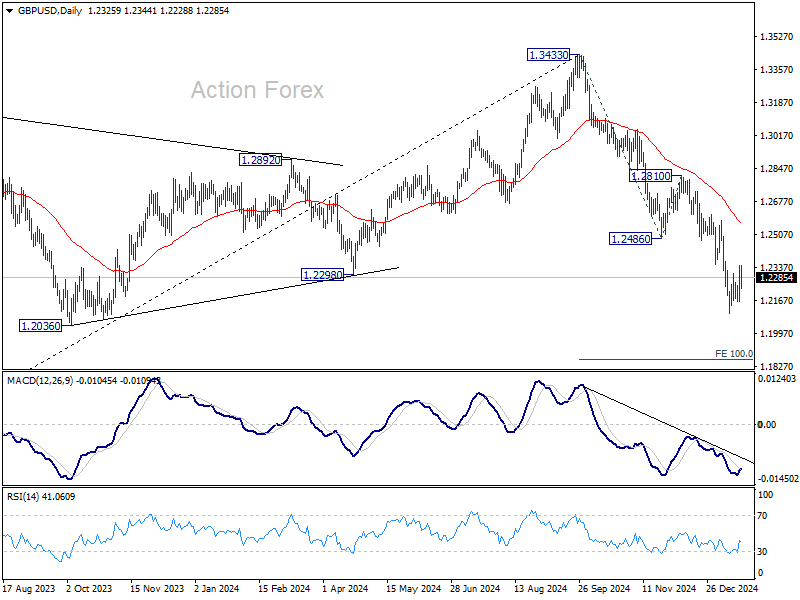

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2211; (P) 1.2278; (R1) 1.2395; More…

Intraday bias in GBP/USD remains neutral for the moment. Consolidations from 1.2099 could extend with stronger recovery But outlook will remain bearish as long as 12486 support turned resistance holds. On the downside, break of 1.2099 will resume the fall from 1.3433 to 100% projection of 1.3433 to 1.2486 from 1.2810 at 1.1863.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433, and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move.