Volatility soared across markets today as reports of emergency trade measures by President-elect Donald Trump overshadowed the day’s economic data. According to CNN, which cited four unnamed sources, Trump is weighing the option of declaring a national economic emergency to justify widespread tariffs on all trade partners, including allies and adversaries.

The plan would rely on the International Economic Emergency Powers Act, a law granting broad authority for a president to manage imports during national emergencies. Trump previously leveraged IEEPA in 2019, when he threatened escalating tariffs on Mexican imports if Mexico failed to curb migrant flows into the United States.

While no final decision on the new measures has been reached, the speculation alone fueled strong rally in Dollar, propelling it to the top spot among major currencies and pushing the 10-year Treasury yield above 4.7%.

Among the majors, Canadian Dollar and Yen followed Dollar’s lead, while Sterling, Kiwi, and Aussie struggled at the bottom of the performance table. Euro and Swiss Franc traded in middle.

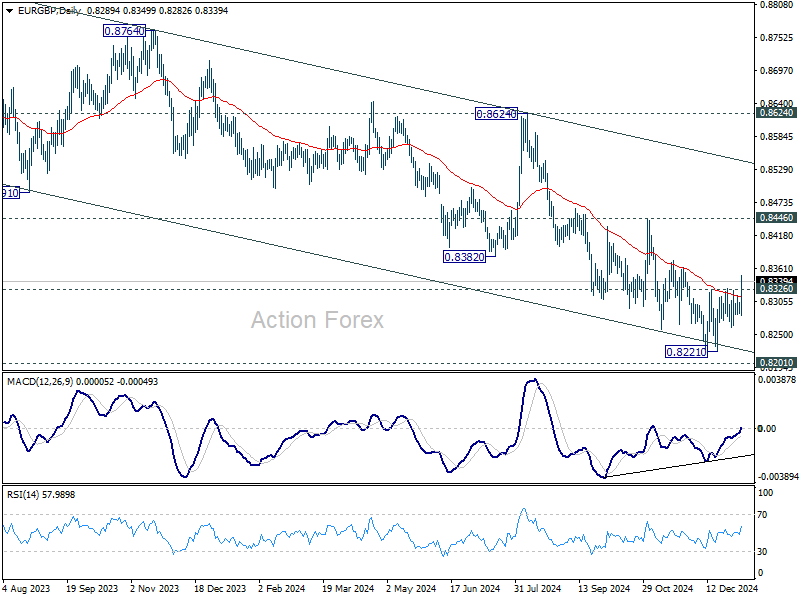

Technically, EUR/GBP’s strong break of 0.8326 resistance today confirms that a short term bottom was at least formed at 0.8221. Considering bullish convergence condition in D MACD, and the notable support from 0.8201 key level, current rebound should likely sustain to 0.8446 resistance, even though it’s still early to declare medium term bullish reversal.

US initial jobless claims fall to 201k vs exp 218k

US initial jobless claims fell -10k to 201k in the week ending January 4, below expectation of 218k. That’s also the slowest number since February 2024. Four-week moving average of initial claims fell -10k to 223k.

Continuing claims rose 33k to 1867k in the week ending December 28. Four-week moving average of continuing claims fell -3k to 1866k.

US ADP employment rises 122k, growth slows in Dec

US ADP private employment data revealed a slowdown in job creation for December, with 122k jobs added, missing market expectations of 143k, and prior month’s 146k.

Breaking down the numbers, goods-producing sectors added 10k jobs, while service-providing industries contributed 112k. Among these, healthcare emerged as a standout performer, leading job creation across sectors in the latter half of 2024.

By establishment size, large companies drove the gains with 97k new hires, while medium-sized businesses added 9k, and small firms contributed a modest 5k.

Wage growth continued to decelerate, with year-over-year pay increases for job-stayers at 4.6%, the slowest since July 2021. Job-changers saw slightly better gains at 7.1%, though this marked a decline from November.

Commenting on the results, Nela Richardson, Chief Economist at ADP, noted, “The labor market downshifted to a more modest pace of growth in the final month of 2024, with a slowdown in both hiring and pay gains.”

Eurozone PPI rises 1.6% mom, energy prices drive monthly gains

Eurozone producer prices rebounded more than expected in November, with PPI rising 1.6% mom, surpassing market forecasts of 1.5% mom. On an annual basis, PPI improved to -1.2% yoy from -3.3% in October, slightly better than the anticipated -1.3% yoy. The data highlights the ongoing influence of energy price volatility on the region’s industrial sector.

Breaking down the monthly changes, Eurozone’s energy prices surged by 5.4% mom, providing the largest contribution to the overall increase. Intermediate goods saw a modest decline of -0.1% mom, while prices for capital goods and non-durable consumer goods remained stable. Durable consumer goods recorded a slight decline of -0.2% mom.

At the EU level, industrial producer prices climbed by 1.7% mom but fell -1.1% yoy. Among member states, Bulgaria (+4.9%), Ireland (+4.5%), and Sweden (+4.2%) posted the highest monthly gains in producer prices, reflecting the energy-driven rise. Conversely, Estonia, Cyprus (-1.4% each), Slovakia (-0.5%), and Luxembourg (-0.4%) saw the sharpest declines, highlighting regional disparities.

Australian monthly CPI rises to 2.3%, but easing core pressures offer RBA relief

Australia’s monthly CPI rose from 2.1% yoy to 2.3% yoy in November, slightly above market expectations of 2.2%. Inflation excluding volatile items and holiday travel jumped from 2.4% yoy to 2.8% yoy. However, trimmed mean CPI, a measure closely watched by RBA, declined from 3.5% to 3.2%, signaling some relief in underlying inflationary pressures.

The rise in CPI was influenced by the reduced impact of government electricity rebates compared to previous months. According to Michelle Marquardt, head of prices statistics at ABS, Electricity prices were -21.5% lower in November, compared to a -35.6% annual fall in October.” Excluding government rebates, electricity prices would have declined by only -1.7% over the same period.

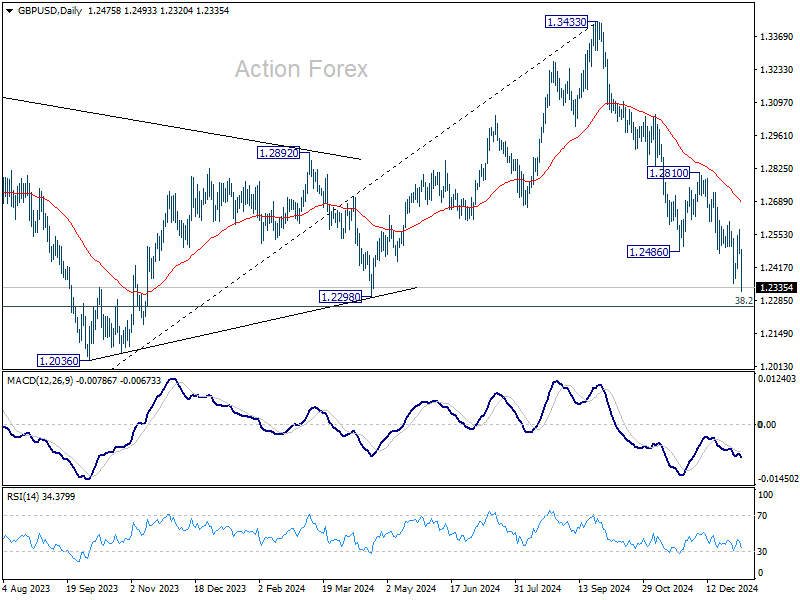

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2445; (P) 1.2510; (R1) 1.2544; More…

GBP/USD’s fall from 1.3433 resumed by breaking through 1.2352 today and intraday bias is back on the downside. Deeper decline would be seen to 1.2256/98 cluster support zone. Strong support could be seen there to bring sustainable rebound. But break of 1.2575 resistance is needed to signal short term bottoming. Otherwise, risk will stay on the downside. Decisive break of 1.2256/98 will carry larger bearish implications.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern. However, firm break of 1.2256 will argue that the trend has reversed and target 61.8% retracement at 1.1528.