Dollar regained some traction overnight, supported by strong services sector data that bolstered expectations for Fed to hold interest rates steady this month. Fed fund futures now imply a 95% probability of no rate cut in January, up from 90% last week. The upbeat economic performance placed moderate downward pressure on both equities and bonds, as markets reassess the Fed’s path. Attention now turns to Friday’s non-farm payroll report, which could finalize the case for the Fed’s January decision and shift market focus toward policy moves for the remainder of the year.

The upcoming release of FOMC December meeting minutes today is another critical event for traders. At the meeting, policymakers projected a median year-end federal funds rate target of 3.75%–4.00%, reflecting a 50bps reduction from current levels. The minutes are expected to provide valuable insight into Fed’s internal deliberations, shedding light on whether risks favor a steeper or shallower easing path in 2025. This will be key in shaping market expectations for monetary policy throughout the year.

Elsewhere, Australian Dollar is under pressure today following release of November monthly CPI data. While headline inflation ticked higher due to the fading impact of energy rebates, the slowdown in trimmed mean CPI—a key measure of core inflation—provided welcome evidence of disinflation. Australian Treasurer Jim Chalmers highlighted the notable improvement in services inflation, which fell from 4.8% to 4.2%. Market expectations for an RBA rate cut in February have now increased to 60%-75%, with traders leaning toward an earlier start to the central bank’s easing cycle, rather than the May timeline initially anticipated.

For the week so far, most major currency pairs remain confined within last week’s ranges. Yen, Swiss Franc, and Dollar are the weakest performers, while Canadian Dollar, British Pound, and New Zealand Dollar are showing relative strength. Euro and Australian Dollar are trading in the middle of the pack.

Technically, overall risk sentiment is a major focus for the rest of the week, for their reactions to FOMC minutes and NFP. NASDAQ is currently extending the consolidation pattern from 20204.58. Deeper retreat cannot be ruled out, but outlook will stay bullish as long as 18671.06 resistance turned support holds. The record-run up trend is expected to resume at a later stage.

Australian monthly CPI rises to 2.3%, but easing core pressures offer RBA relief

Australia’s monthly CPI rose from 2.1% yoy to 2.3% yoy in November, slightly above market expectations of 2.2%. Inflation excluding volatile items and holiday travel jumped from 2.4% yoy to 2.8% yoy. However, trimmed mean CPI, a measure closely watched by RBA, declined from 3.5% to 3.2%, signaling some relief in underlying inflationary pressures.

The rise in CPI was influenced by the reduced impact of government electricity rebates compared to previous months. According to Michelle Marquardt, head of prices statistics at ABS, Electricity prices were -21.5% lower in November, compared to a -35.6% annual fall in October.” Excluding government rebates, electricity prices would have declined by only -1.7% over the same period.

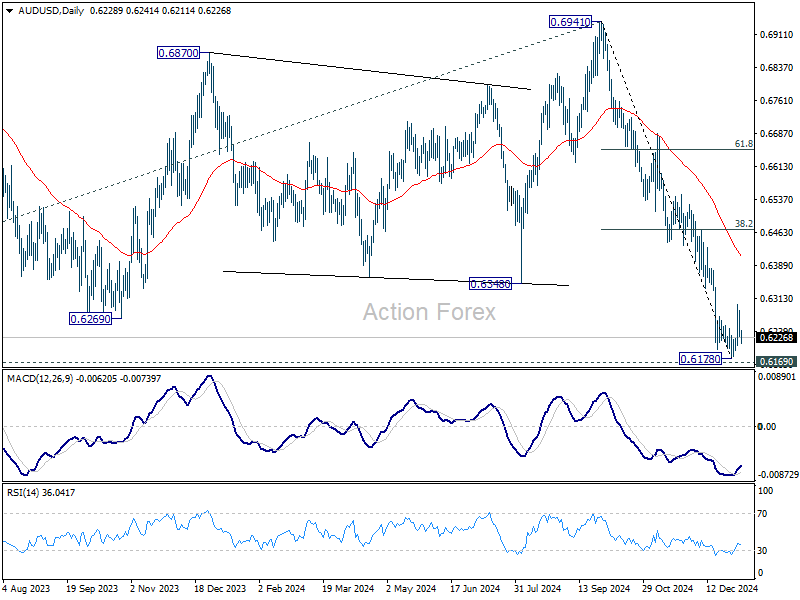

AUD/USD Daily Report

Daily Pivots: (S1) 0.6210; (P) 0.6249; (R1) 0.6270; More...

Intraday bias in AUD/USD is turned neutral with current retreat. Consolidation from 0.6178 could still extend with another rise to 55 D EMA (now at 0.6416). But near term outlook will stay bearish as long as 38.2% retracement of 0.6941 to 0.6178 at 0.6469. Nevertheless, firm break of 0.6169 key support will confirm larger down trend resumption.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006, and could have completed at 0.6941 already. Firm break of 0.6169 support will confirm down trend resumption for 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6587) holds.