Swiss Franc weakened across the board today after inflation data revealed a reversal in annual CPI back 0.6% in December. This marks the fourth consecutive month of deflationary pressure, as monthly CPI continues to slide. With inflation well below 1% for the past four months, concerns over a return to deflation have grown, intensifying expectations for further monetary easing by SNB in 2025.

Following the release, the probability of a 25-basis-point cut by SNB in March rose to 98.4% from 91% previously. Speculation is also building around the possibility of a 50-basis-point cut, similar to December’s move, which would bring the policy rate to 0.00%. Even more notably, discussions are emerging about the return of negative interest rates this year, as a tool for managing deflationary pressures.

Euro, on the other hand, is supported by another month of acceleration in headline CPI, while consumer inflation expectations also jumped. Its still early to argue that inflation expectations have deviated too much from ECB’s 2% target, and thus, policy easing should still carry on. Yet, the pace would remain measured and gradual, as many policymakers have expressed their preference for.

On the broader currency market, Swiss Franc emerged as the weakest performer, followed by the Yen and Dollar. The greenback struggled amid persistent ambiguity surrounding the incoming Trump administration’s tariff policy, with speculation oscillating between blanket tariffs and sector-specific measures. Meanwhile, commodity-linked currencies showed strength, led by New Zealand Dollar and Australian Dollar, as risk sentiment improved. British Pound also posted gains, while Canadian Dollar and Euro held steady in mid-range performance.

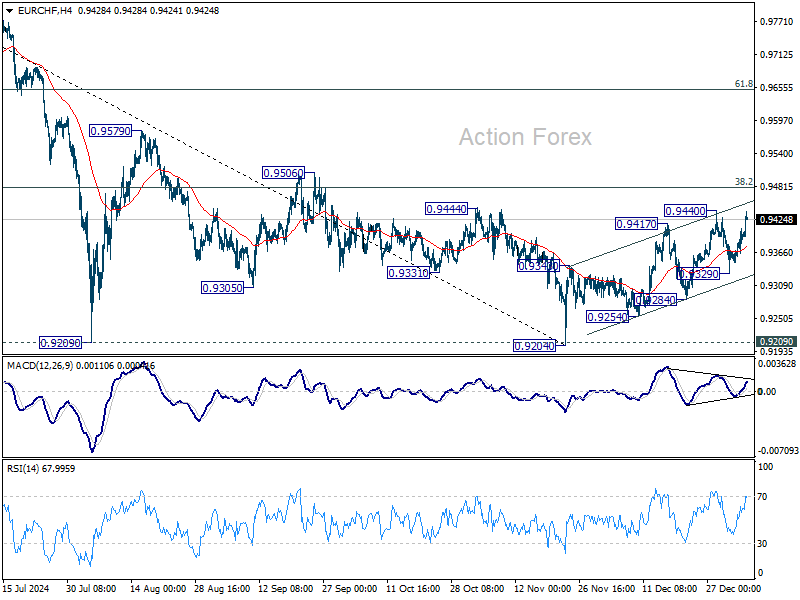

Technically, EUR/CHF’s corrective rally from 0.9204 looks ready to resume through 0.9440. Yet, strong resistance is expected from 38.2% retracement of 0.9928 to 0.9204 at 0.9481 to limit upside.

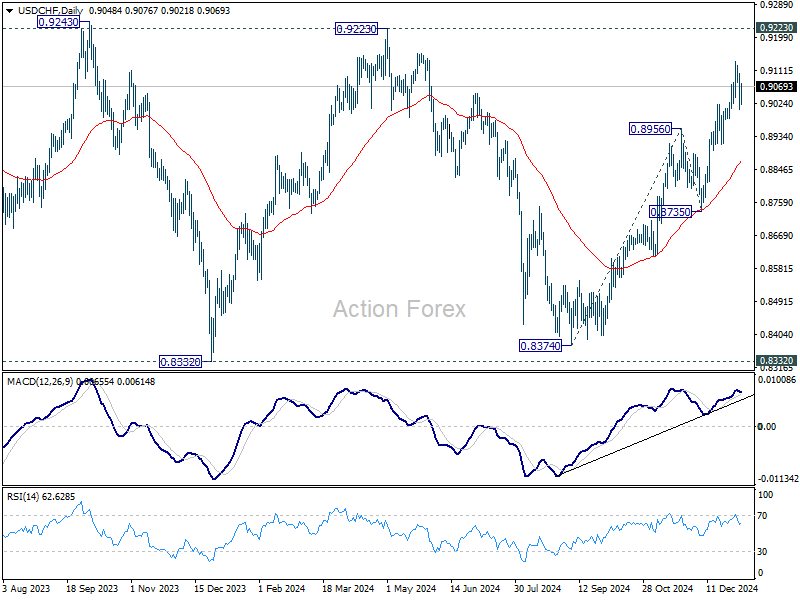

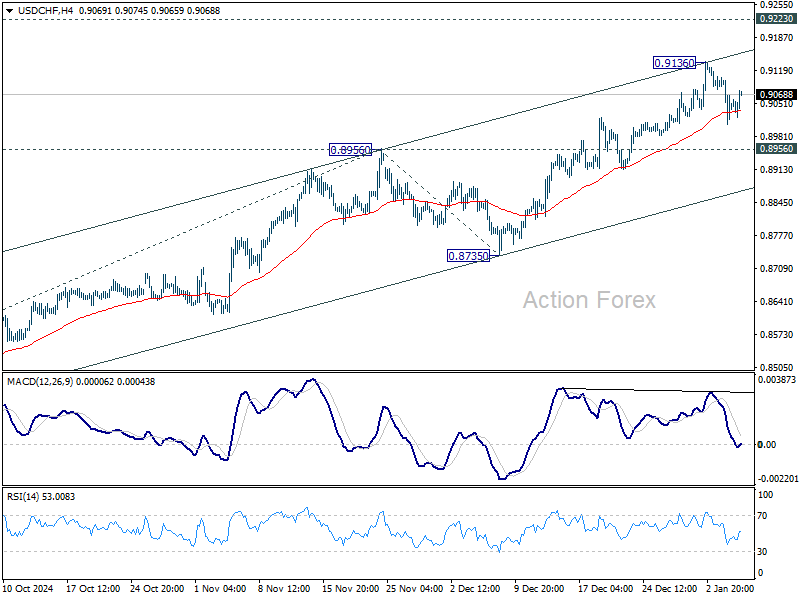

However, if USD/CHF could break through 0.9223 resistance with conviction, that would be a sign of bullish reversal in the pair, and a signal of more pronounced selloff in Swiss Franc.

Accelerated rally in USD/CHF could be accompanied by similar move in EUR/CHF through mentioned 0.9481 fibonacci level.

In Europe, at the time of writing, FTSE is down -0.23%. DAX is up 0.61%. CAC is up 0.74%. UK 10-year yield is up 0.0313 at 4.640. Germany 10-year yield is up 0.004 at 2.452. Earlier in Asia, Nikkei rose 1.97%. Hong Kong HSI fell -1.22%. China Shanghai SSE rose 0.71%. Singapore Strait Times rose 0.17%. Japan 10-year JGB yield fell -0.0004 to 1.129.

Canada’s merchandise trade deficit narrows to CAD -544m in Nov

Canada’s merchandise trade deficit narrowed in November, shrinking to CAD -323 million from October’s revised CAD -544 million, outperforming market expectations of a CAD -800 million shortfall. This improvement was driven by a 2.2% mom rise in exports, complemented by a 1.8% mom increase in imports.

Exports saw gains across nine of the 11 product categories, with higher prices partially contributing to the increase. Adjusted for inflation, real export volumes still advanced by 0.5% mom.

Canadian Dollar’s depreciation against the US Dollar over October and November played a notable role in boosting the relative value of cross-border trade.

Over the two months, Canadian exports grew 3.9%, while imports increased 2.2%. In US Dollar terms, however, exports rose by just 0.8%, and imports declined by 1.0%.

Eurozone CPI rises to 2.4% yoy, core unchanged at 2.7% yoy again

Eurozone inflation accelerated again in December, with headline CPI rising to 2.4% yoy, up from November’s 2.2% yoy, as per the flash estimate. That’s also the third month rise in inflation since hitting 1.8% yoy back in September.

Meanwhile, core CPI, which excludes volatile components such as energy, food, alcohol, and tobacco, remained steady at 2.7% yoy for the fourth straight months. Both readings , aligned with forecasts.

Breaking down the components of inflation, services led the way with an annual rate of 4.0%, up slightly from November’s 3.9%. This was followed by food, alcohol, and tobacco, which held steady at 2.7%. Non-energy industrial goods inflation softened marginally to 0.5% from 0.6%, while energy prices rebounded modestly to 0.1% from a sharp -2.0% contraction in the prior month.

ECB survey shows inflation expectations rise, growth outlook deteriorates

ECB’s Consumer Expectations Survey for November 2024 revealed that inflation expectations continued their upward drift, with the median forecast for inflation over the next 12 months ticking up to 2.6%, from 2.5% in October. This marks the second consecutive monthly increase. Longer-term inflation expectations for three years ahead also rose to 2.4%, up from October’s 2.1%, reaching a level last seen in July 2024.

Despite the uptick in inflation forecasts, uncertainty around short-term inflation expectations held steady at its lowest point since February 2022. This suggests consumers are becoming more confident in their projections, albeit with inflation still running above ECB’s 2% target over the medium term.

On the downside, economic growth expectations took a sharper negative turn, with households predicting a contraction of -1.3% over the next 12 months, compared to the -1.1% forecast in October. This worsening outlook reflects persistent concerns about the Eurozone’s economic health amid weak demand and geopolitical risks.

Labor market sentiment also deteriorated, as expectations for unemployment rate 12 months ahead climbed to 10.6%, reversing October’s slight improvement to 10.4%.

Swiss CPI falls back to 0.6% yoy in Dec

Swiss CPI fell -0.1% mom in December, matched expectations. Core CPI (excluding fresh and seasonal products, energy and fuel) was unchanged for the month. Domestic products prices rose 0.1% mom while imported products prices fell -0.5% mom.

Comparing with the same month a year ago, headline CPI slowed from 0.7% yoy to 0.6% yoy, matched expectations. Core CPI slowed from 0.9% yoy to 0.7% yoy. Domestic products prices slowed from 1.7% yoy to 1.5% yoy. Imported products prices ticked up from -2.3% yoy to -2.2% yoy.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9001; (P) 0.9053; (R1) 0.9097; More…

USD/CHF bounces slightly after drawing support from 55 4H EMA, but stays below 0.9136 resistance. Intraday bias remains neutral for more consolidations. But further rally is expected as long as 0.8956 resistance turned support holds. Above 0.9136 will resume the rally from 0.8374 to 0.9223 key resistance next. However, firm break of 0.8956 will turn bias back to the downside for 55 D EMA (now at 0.8869).

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes. However, decisive break of 0.9223 will be an important sign of bullish trend reversal.