As markets wind down for the year-end holiday period, forex trading activity turns subdued, with limited momentum across major pairs. Dollar, while maintaining its position as the strongest currency of the month, is facing challenges in decisively breaking last month’s highs against European majors. However, the greenback still made some headway against Yen and commodity currencies

This week’s economic calendar is notably lighter, with the focus shifting to central bank minutes from BoJ, BoC, and RBA, alongside a handful of key data releases from the US, Canada, and Japan.

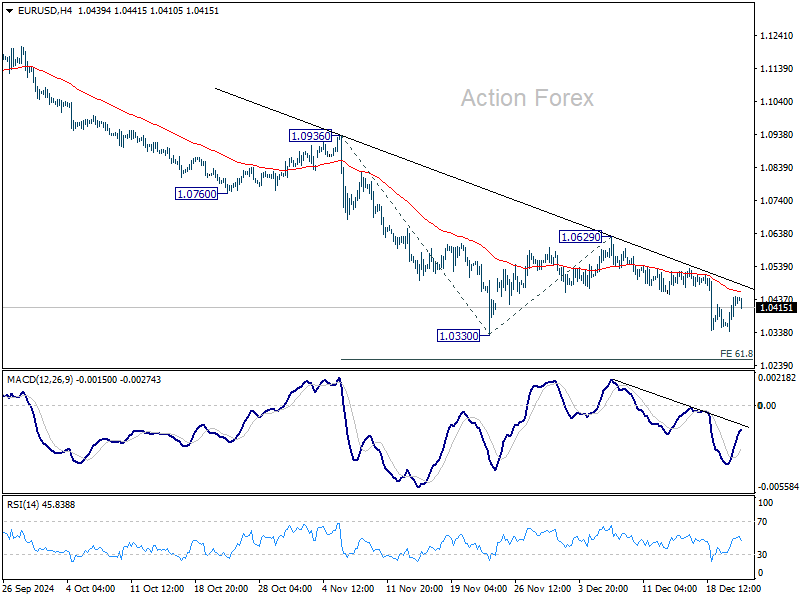

Technically, while EUR/USD failed to break through 1.0330 support on first attempt last week, it seems not giving up yet, with the recovery capped below falling 55 4H EMA. Another fall remains in favor through 1.0330 to 61.8% projection of 1.0936 to 10330 from 1.0629 at 1.0254. However, a significant breakout below this projection is likely to occur only after the New Year.

In Asia, Nikkei closed up 1.19%. Hong Kong HSI is up 0.70%. China Shanghai SSE is down -0.50%. Singapore Strait Times is up 0.88%. Japan 10-year JGB yield rose 0.011 to 1.067.

ECB’s Lagarde: Inflation target within reach, services inflation still stubborn

In an interview with the Financial Times, ECB President Christine Lagarde expressed optimism about nearing the inflation target.

She remarked that ECB is “very close” to declaring that inflation has been “sustainably” brought back to its 2% medium-term target.

The latest inflation reading of 2.2% reflects the success of ECB’s restrictive monetary policy. However, she highlighted persistent concerns in the services sector, where inflation remains high at 3.9%, describing it as “not budging much” despite showing slight signs of decline.

On the topic of US tariff threats, Lagarde emphasized the economic risks of retaliatory trade measures, stating, “Retaliation was a bad approach.” She warned that tit-for-tat trade conflicts could harm the global economy.

Natural gas prices surge on winter demand and long-term power trends

Natural gas prices climbed to a nearly two-year high, driven by immediate weather-related demand and a bullish long-term outlook for global energy consumption.

In the short term, forecasts for below-average temperatures across the northern hemisphere—including North America, Europe, China, and Japan—are expected to significantly increase daily heating demand as these regions, which account for more than two-thirds of global gas consumption, enter their peak heating season. This has bolstered sentiment, with limited downside for prices likely until well into 2025.

Beyond the seasonal factors, the long-term outlook for natural gas remains robust. Rising electricity demand as the race for artificial intelligence accelerates, is projected to grow power consumption for such facilities by 10–15% annually through 2030, potentially accounting for up to 5% of global power demand by that time.

Natural gas is expected to play a pivotal role as a baseload energy source in this transition, given its current dominance in power generation. In the US, natural gas powers approximately 40–45% of electricity production, while globally, that share is closer to 25%. However, as more countries transition from coal to gas, the share of gas in electricity generation is anticipated to increase.

Technically, the break of 3.446 resistance last week was an important sign of underlying medium term momentum. Rise from 1.570 (Feb low) is now expected to continue to 161.8% projection of 1.570 to 3.024 from 1.852 at 4.204.

Nevertheless, momentum should target to wane above 4.204, and, in particular, as it approaches 38.2% retracement of 10.03 to 1.570 at 4.80.

Minutes and deliberations from BoC, BoJ and RBA highlight a holiday week

With the global markets winding down for the holiday season, the week ahead features a much lighter economic calendar. The spotlight will fall on central bank deliberations and meeting minutes from BoJ, BoC and RBA. A handful of key economic data releases from the US, Canada, and Japan will also attract attention as the year concludes.

For BoJ, Summary of Opinions for December, due on Friday, holds more weight than Tuesday’s October minutes, as markets seek clarity on the board’s discussions regarding a potential rate hike in January. The report will also provide insights into BoJ’s perspective on two critical issues: the uncertainty surrounding wage growth in 2025 and the risks posed by US trade policies. These considerations are likely to influence the pace and direction of Japan’s policy normalization, shaping expectations for the coming months.

BoC’s December meeting marked a turning point in its monetary policy stance, with a 50bps rate cut and a clear message that further easing would no longer be automatic. Policymakers indicated that decisions would now be taken on a meeting-by-meeting basis, reflecting a shift toward caution after substantial easing since June. The minutes will be analyzed for clues about how close the BoC is to a pause, the expected pace of additional cuts, and how deep further easing might go.

Meanwhile, RBA introduced a surprising dovish pivot at its December meeting. Growing confidence in the disinflationary trend led the board to omit language suggesting openness to further tightening. However, while this shift suggests the RBA is exploring a less restrictive path, it does not necessarily mean the first rate cut is imminent. Market participants will scrutinize the meeting minutes to understand the reasoning behind this “big pivot” and gauge what data RBA considers essential before moving toward easing.

On the data front, attention will turn to US consumer confidence and durable goods orders, Canada’s monthly GDP, and Tokyo CPI from Japan.

Here are some highlights for the week:

- Monday: Germany import prices; UK Q3 GDP Final; Swiss UBC economic expectations; Canada GDP, IPPI, RMPI; US consumer confidence; BoC summary of deliberations.

- Tuesday: BoJ minutes; RBA minutes; US durable goods orders, new home sales.

- Wednesday: Japan corporate services prices.

- Thursday: Japan housing starts, US jobless claims.

- Friday: Japan BoJ summary of opinions, Tokyo CPI, industrial production, retail sales, unemployment rate; US goods trade balance.

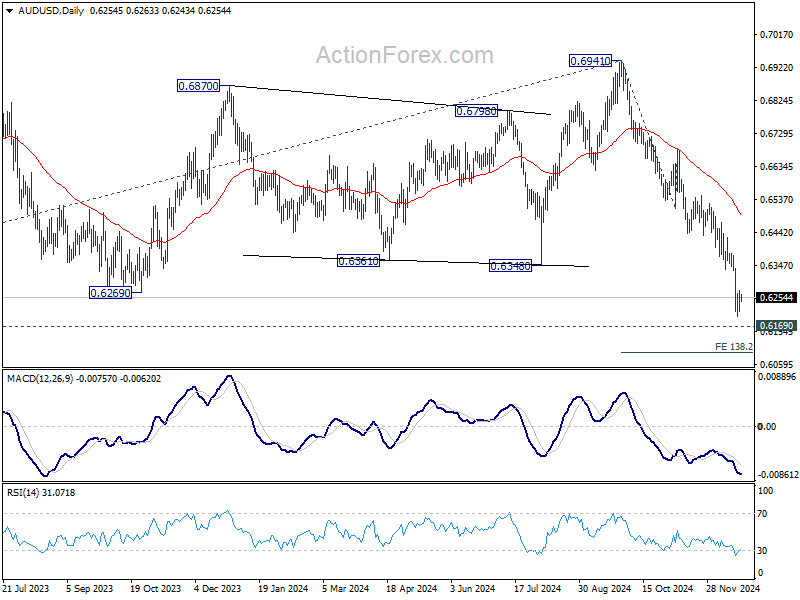

AUD/USD Daily Report

Daily Pivots: (S1) 0.6219; (P) 0.6247; (R1) 0.6278; More...

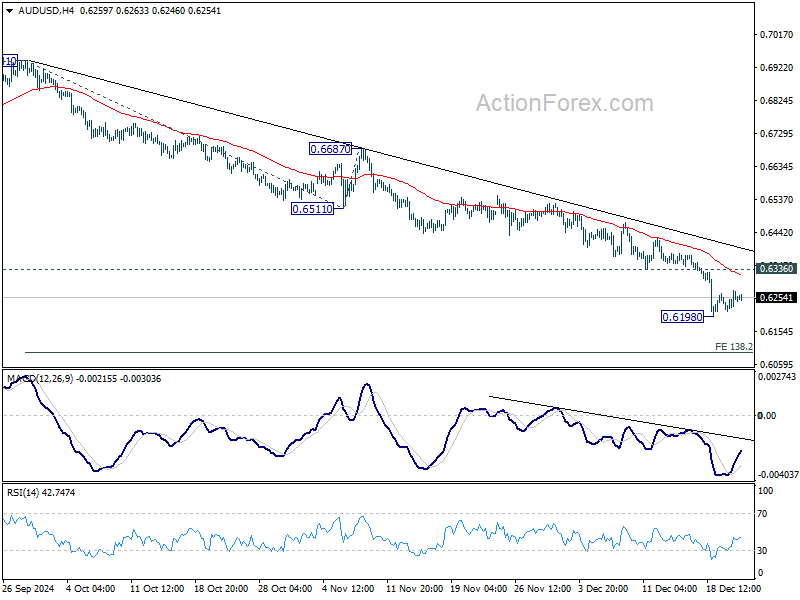

Intraday bias in AUD/USD remains neutral for sideway trading above 0.6198. Consolidations should be relatively brief as long as 0.6336 support turned resistance holds. Break of 0.6198 will resume the fall from 0.6941 to 0.6169 long term support, and then 138.2% projection of 0.6941 to 0.6511 from 0.6687 at 0.6074. Nevertheless, firm break of 0.6336 will bring stronger rebound lengthier correction before staging another decline.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006. Firm break of 0.6169 support will confirm down trend resumption for 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6588) holds.