Australian Dollar continued its decline today as speculation mounted that China might allow Yuan to weaken in 2025 to counteract the economic impact of increased US trade tariffs under the incoming Trump administration. While no official announcement has been made, Beijing appears to ready to signal greater reliance on market-driven currency valuation. Also, according to a Reuters report, Chinese officials might tolerate depreciation of Yuan from its current level of 7.3 against Dollar to 7.5 if trade tensions intensify.

Technically, USD/CNH also bounces on the news but stays below 7.3145 short term top. Nevertheless, further rally is expected as long as 7.2279 support holds. Rise from 6.9709 is expected to continue. Break of 7.3145 will pave the way to 7.3745 key resistance (2022 high). The next rally is USD/CNH could give extra drag on AUD/USD.

Overall for the week so far, however, Yen is currently the worst performer, followed by Kiwi, and then Euro. Sterling is the best, followed by Dollar, and then Canadian. Swiss Franc and Aussie are mixed in the middle. The markets are now looking into today’s US CPI and BoC rate decision for the next big moves.

BoC to flash rates by 50bps again in quick path to neutral

BoC is widely anticipated to lower its overnight rate by another 50bps at today’s meeting, reducing the policy rate to 3.25%. This follows a similar move in October, aimed at addressing a cooling economy where inflation has been at or below 2% for three months already, and core measures remain slightly above target. Last week’s data showing unemployment rate jumping to 6.8% from 6.5% solidified expectations of a significant rate reduction.

A recent Reuters poll highlighted this expectation, with 21 of 27 respondents predicting a 50bps cut and the remainder forecasting a more modest 25bps reduction. The primary argument for aggressive easing centers on the need to return interest rates to a neutral range, estimated between 2.25% and 3.25%. Following today’s expected cut, rates would align with the upper bound of neutral, still potentially exerting a mildly restrictive effect on the economy.

However, there is an opposing view that recent resilience in consumer spending, inflation, and labor market data could justify a slower pace of easing. This argument suggests that BoC could take a more measured approach, affording time to assess the economy’s response to October’s 50bps cut before making further moves.

Regardless, the debate now shifts to determining the eventual terminal rate, with clarity likely, hopefully, to emerge only in January’s Monetary Policy Report.

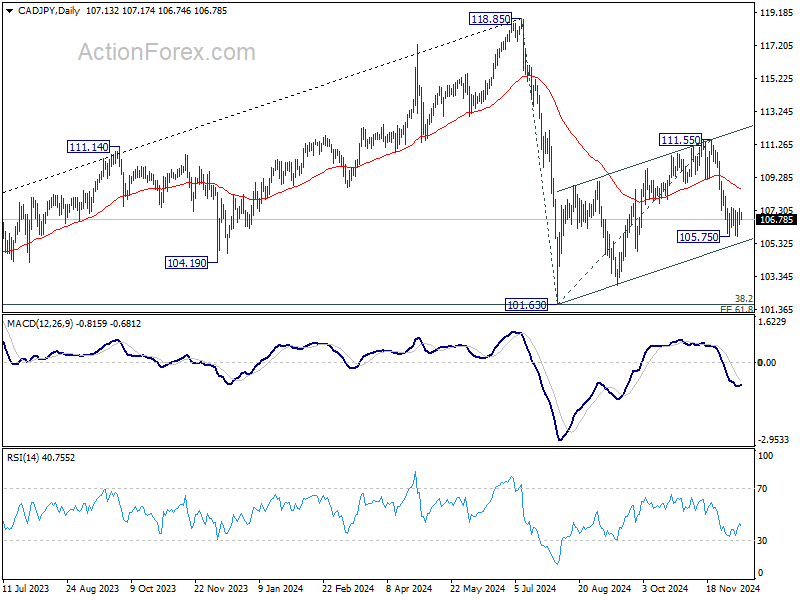

Technically, similar to other Yen crosses, CAD/JPY’s corrective rebound from 101.63 should have completed with three waves up to 111.55. Further decline is expected as long as 55 D EMA (now at 108.65) holds. Break of last week’s low at 105.75 will resume the fall from 111.55 towards 101.63 low, and possibly through it to resume the larger decline from 118.85. However, the speed of the decline could more hinge on the development in Yen than Loonie.

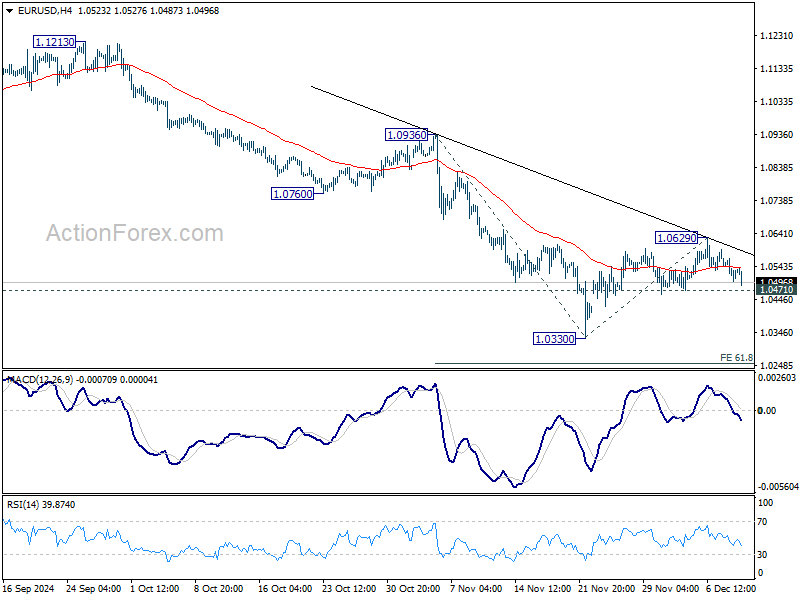

US CPI sets to drive EUR/USD for downside breakout

The spotlight today is firmly on the release of US CPI data for November. Expectations are for headline inflation to tick up from 2.6% to 2.7%, continuing its rebound from the September low of 2.4%. Meanwhile, core CPI is forecast to hold steady at 3.3%, staying in the 3.2%-3.2% range it has maintained since June.

Unless today’s data deviates significantly from expectations, it is unlikely to deter Fed from delivering a widely anticipated 25bps rate cut next week, bringing the federal funds rate to 4.25-4.50%. Fed fund futures currently reflect an 86% probability of this move.

But more critically, today’s readings could solidify the case for a pause in January, supported by futures pricing nearly 80% probability of such an outcome.

A pause would allow policymakers to digest the inflationary implications of upcoming fiscal and trade policies under President-elect Donald Trump. Current Treasury Secretary Janet Yellen cautioned that Trump’s tariffs pose a dual risk of “derail the progress” on inflation and have “adverse consequences on growth”, creating a potential headache for Fed as it balances these challenges.

Technically, EUR/USD would be a key to watch in reaction to US CPI. Recovery from 1.0330 short term bottom is seen as a corrective move, might could have completed at 1.0629 already. Break of 1.0471 support will suggest that fall from 1.1213 is ready to resume through 1.0330. Next target will be 61.8% projection of 1.0936 to 1.0330 from 1.0629 at 1.0254.

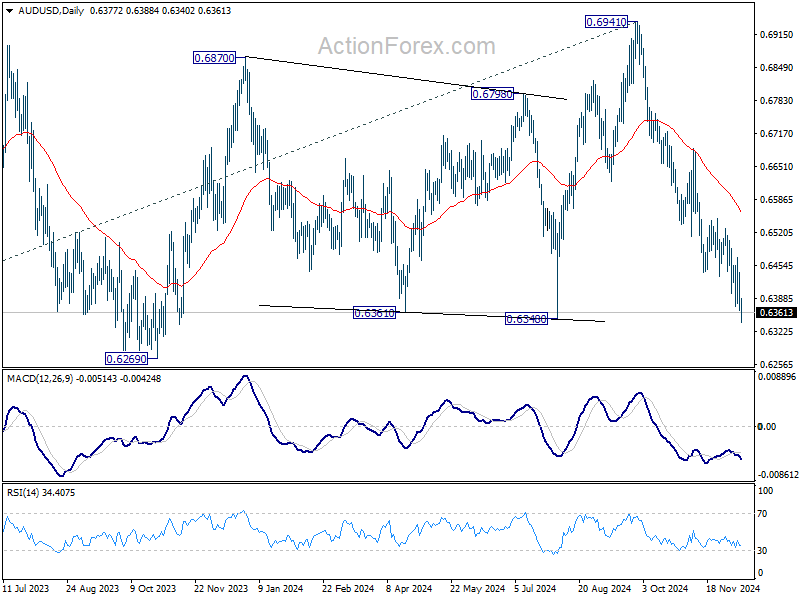

AUD/USD Daily Report

Daily Pivots: (S1) 0.6347; (P) 0.6395; (R1) 0.6426; More...

AUD/USD’s break of 0.6371 temporary low indicates resumption of whole fall from 0.6941. Intraday bias is back on the downside for 0.6348 support, and then 0.6269. On the upside, above 0.6470 resistance will turn intraday bias neutral first. But outlook will stay bearish as long as 55 D EMA (now at 0.6559) holds, in case of recovery.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006. More sideway trading could be seen above 0.6169, but overall outlook will stay bearish as long as 0.6941 resistance holds. Firm break of 0.6169 will resume the down trend to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next.