Australian Dollar dropped sharply in Asian session following a significant dovish turn in RBA’s communication. After holding rates steady at 4.35%, the central bank signaled growing confidence that inflationary pressures are easing, marking a departure from its previously vigilant tone. While May remains the most likely timing for a rate cut according to many economists, traders are increasingly pricing in a February reduction, now seen as a real possibility.

Meanwhile, optimism around China’s economic stimulus faded as markets shrugged off state media reports of President Xi Jinping’s “full confidence” in achieving economic growth targets. Hong Kong stocks remained subdued, reflecting the market’s demand for more concrete and actionable measures from policymakers. The upcoming Central Economic Work Conference is now in focus, with investors seeking clarity on 2025 economic priorities and strategies. Without substantive developments, sentiment around China’s recovery efforts may remain tepid.

Overall in the currency markets, Aussie is the day’s weakest currency so far, closely followed by Kiwi and then Dollar. On the other hand, Swiss Franc is the strongest performer, with Euro and Sterling also gaining ground. Canadian Dollar and Yen showed mixed performances.

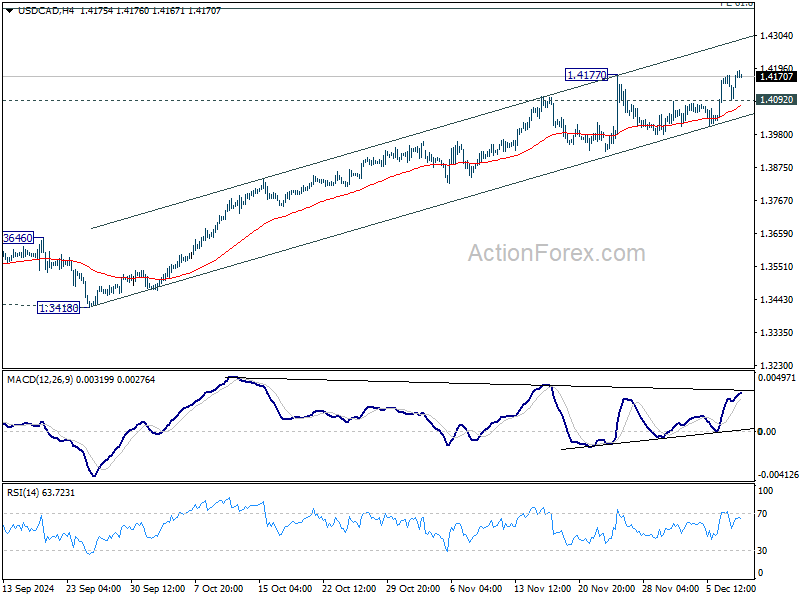

Technically, USD/CAD’s breach of 1.4177 resistance suggests that larger up trend is resuming. Further rise is now in favor as long as 1.4092 support holds. Next target is medium term projection level at 1.4391.

In Asia, Nikkei rose 0.43%. Hong Kong HSI is up 0.17%. China’s Shanghai SSE is up 0.74%. Singapore Strait Times is up 0.56%. Japan 10-year JGB yield is up 0.0223 at 1.064. Overnight, DOW fell -0.54%. S&P 500 fell -0.61%. NASDAQ fell -0.62%. 10-year yield rose 0.048 to 4.199.

RBA holds rates steady, dovish shift raises odds of Feb cut

RBA held its cash rate steady at 4.35% as widely expected, but the accompanying statement marked a clear pivot towards a more dovish stance. While May remains the more likely timing for the first rate cut, February is now emerging as a real possibility, depending on upcoming Q4 jobs and inflation data from Australia.

The most striking change in the RBA’s statement was its removal of the phrase “not ruling anything in or out” regarding future monetary policy decisions. This change aligns with the board’s growing “confidence that inflationary pressures are declining.” RBA acknowledged that some upside risks to inflation have eased and noted the gap between aggregate demand and supply capacity is continuing to narrow.

Recent activity data, according to the RBA, has been “on balance softer than expected,” with the central bank pointing out risks of a slower-than-anticipated recovery in consumer spending. These factors collectively suggest a step away from inflation vigilance and a move closer to easing policy.

Governor Michele Bullock later emphasized that the wording adjustments in the statement were deliberate. While she clarified that a rate cut was not discussed during today’s meeting, she acknowledged uncertainty over whether one could occur as early as February.

Markets responded swiftly, with swaps traders raising the probability of a February rate cut to over 60%, up from 50% the previous day. Market expectations now fully price in two rate reductions by May.

Australia’s NAB confidence turns negative to -3 as business conditions deteriorate

Australia’s NAB Business Confidence index slid sharply to -3 in November, down from 5 in October, returning to below average levels. Business conditions also weakened notably, dropping from 7 to 2, marking declines across trading, profitability, and employment metrics. Trading conditions fell to 5 from 13, profitability shifted into negative territory at -1 from 5, and employment conditions edged down to 2 from 3.

Cost pressures showed little relief, with input costs largely unchanged. Labor cost growth held steady at 1.4% in quarterly terms, while purchase cost growth edged slightly higher by 0.2 percentage points to 1.1%. On the pricing side, output price growth remained unchanged at 0.6% in quarterly terms, with retail price growth retreating to 0.6% and recreation and personal services easing slightly to 0.7%.

China’s trade data highlights persistent import weakness amid export slowdown

China’s trade data for November showed weak signals as exports grew 6.7% yoy to USD 312.3B, down sharply from October’s 12.7% yoy expansion and missing expectations of 8.5% growth.

Export performance varied across key regions, with shipments to the US rising 8% yoy, to the EU up 7.2% yoy, and to ASEAN growing by 14.9% yoy. However, exports to Russia declined by -2.5% yoy.

On the import side, the picture was decidedly more negative. Imports fell by -3.9% yoy, marking the steepest decline since September 2023, and missing expectations of a slight 0.3% yoy increase.

Weakness was broad-based, with imports from ASEAN dropping -3% yoy, the US contracting by -11% yoy, and the EU and Russia both registering declines of -6.5% yoy. These numbers underscore persistent weak domestic demand, consistent with recent data showing subdued consumer inflation.

Trade balance widened from USD 95.7B to 97.4B, above expectation of USD 92.0B.

Looking ahead

Germany CPI final will be released in European session. Later in the day, US will release NFIB business optimism and non-farm productivity Q3.

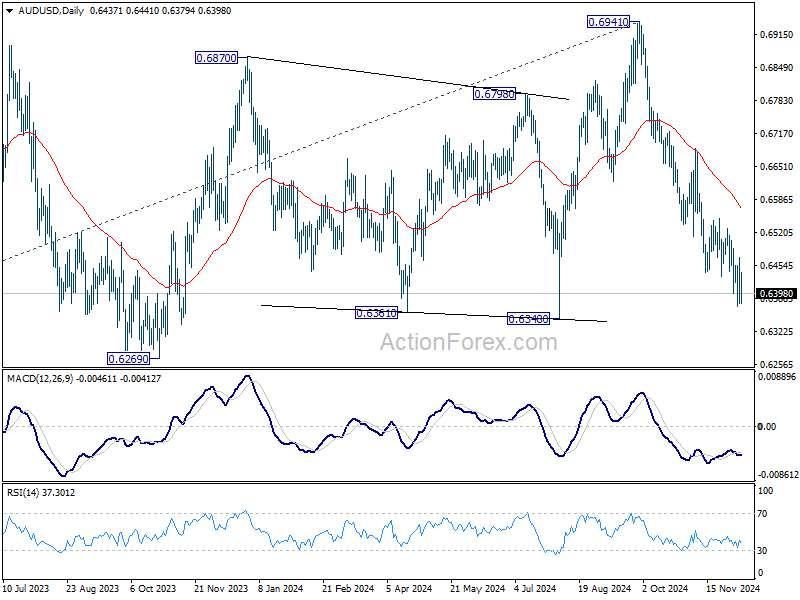

AUD/USD Daily Report

Daily Pivots: (S1) 0.6390; (P) 0.6430; (R1) 0.6481; More...

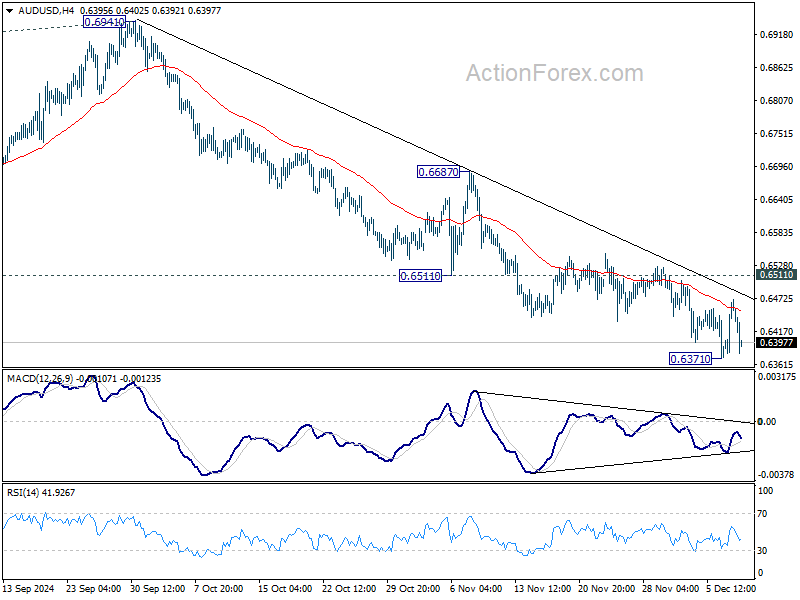

Volatility continues in AUD/USD but it’s still staying in range above 0.6371 temporary low. Intraday bias remains neutral and further decline is expected with 0.6511 resistance intact. On the downside, below 0.6371 will resume the fall from 0.6941 to 0.6348 support, and then 0.6269. Nevertheless, considering bullish convergence condition in 4H MACD, firm break of 0.6511 will confirm short term bottoming, and turn bias back to the upside for 55 D EMA (now at 0.6568) next.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006. More sideway trading could be seen above 0.6169, but overall outlook will stay bearish as long as 0.6941 resistance holds. Firm break of 0.6169 will resume the down trend to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next.