Dollar strengthened broadly in Asian session, especially against commodity currencies, following a bold announcement from President-elect Donald Trump. Trump pledged to impose steep tariffs on Canada, Mexico, and China to pressure them into halting fentanyl trafficking to the US.

The announcement came as markets were digesting the positive sentiment surrounding Trump’s Treasury Secretary pick, hedge fund magnate Scott Bessent, whose appointment had propelled DOW to record highs overnight. Analysts viewed Bessent as a stabilizing presence, with some seeing him as someone who could keep Trump “on a tight leash.” However, Trump’s remarks reinforced his intent to lead decisively on trade policies.

In the currency markets, Japanese Yen emerged is currently the strongest performer for the day so far, bolstered by the sharp decline in US Treasury yields. Additionally, October’s corporate services inflation in Japan rose to 2.9%, which keeps a December BoJ rate hike alive. Dollar followed as the second strongest currency, with New Zealand Dollar ranking third.

Conversely, Canadian Dollar plummeted on Trump’s tariff threats, making it the session’s weakest currency, followed by Australian Dollar and Euro. British Pound and Swiss Franc held steady in middle positions.

Technically, US 10-year yield is now pressing 4.264 support after yesterday’s gap down and extended decline. Firm break there will confirm short term topping at 4.505, after rejection by both medium term falling trend line and 61.8% retracement of 4.997 to 3.603 at 4.464. Deeper fall should then be seen through 55 D EMA (now at 4.185) and drag USD/JPY back towards 150 mark.

In Asia, at the time of writing, Nikkei is down -1.42%. Hong Kong HSI is up 0.19%. China Shanghai SSE is up 0.07%. Singapore Strait Times is down -0.17%. Japan 10-year JGB yield is down -0.0096 at 1.065. Overnight, DOW rose 0.99%. S&P 500 rose 0.30%. NASDAQ rose 0.27%. 10-year yield fell -0.145 to 4.265.

CAD falls sharply as Trump pledges 25% tariffs to combat fentanyl trafficking

Canadian Dollar and Mexican Peso faced sharp declines after US President-elect Donald Trump announced plans for aggressive trade measures targeting Canada, Mexico, and China.

Trump stated that on January 20, as one of his first Executive Orders, he will authorize a 25% tariff on “all products” imported from Canada and Mexico. The tariffs will remain in place “until such time as drugs, in particular Fentanyl, and all illegal aliens stop this invasion of our country” through what he termed “ridiculous open borders.”

China is also in Trump’s crosshairs, with plans for an additional 10% tariff on top of existing levies, aimed at combating the “massive amounts of drugs” flowing into the US from the region.

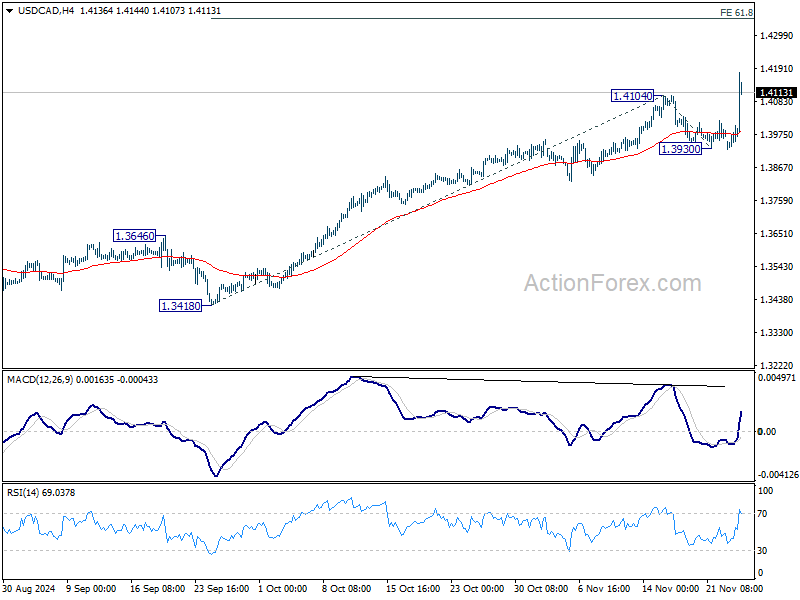

Technically, USD/CAD’s up trend resumed by breaking through 1.4104 resistance. Further rise is now expected as long as 1.3930 support holds even in case of retreat. Next target is 61.8% projection of 1.3418 to 1.4104 from 1.3930 at 1.4354.

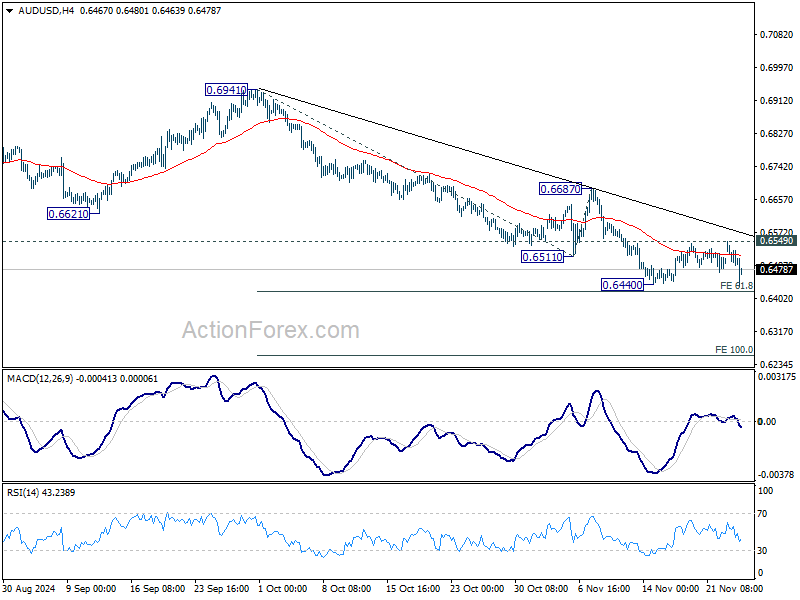

AUD/USD also dipped notably but stays above 0.6440 support so far. Further decline is expected as long as 0.6549 resistance holds. Decisive break of 61.8% projection of 0.6941 to 0.6511 from 0.6687 at 0.6421 will resume the fall from 0.6941 to 100% projection at 0.6257 next.

Fed’s Goolsbee sees clear path towards neutral rates

Chicago Fed President Austan Goolsbee has reiterated his support for gradual reduction in the fed funds rate, provided there is no “convincing evidence of overheating” in the economy. He noted that the pace of rate adjustments would depend on evolving economic conditions and the broader outlook.

“The through line to me is pretty clear that we’re on a path, and that path is going to lead to lower rates, closer to what you might call neutral,” Goolsbee emphasized overnight.

Policymakers will assess several key data points ahead of the December meeting. Goolsbee cautioned against drawing firm conclusions from one month’s data. He remarked that inflation is now “not that far above the 2% target”.

Fed’s Kashkari: December rate cut still a reasonable debate

Minneapolis Fed President Neel Kashkari signaled that a rate cut at the December meeting remains a “reasonable consideration,” reflecting ongoing debates within the central bank. Speaking to Bloomberg TV, Kashkari stated, “Right now, knowing what I know today, still considering a 25-basis-point cut in December—it’s a reasonable debate for us to have.”

Kashkari highlighted that the economy’s resilience in the face of higher interest rates suggests the neutral rate may be higher than previously estimated. This observation raises questions about the effectiveness of current monetary policy in cooling economic demand. He noted that if this resilience persists, it might indicate a structural shift rather than a temporary one.

“This is what I’m trying to understand right now,” Kashkari said, emphasizing the need to assess “how much downward pressure we are putting on the economy, and what is the path for inflation.”

Looking ahead

US house price index, new home sales, and consumer confidence will be released today. But more focus will be on FOMC minutes, which is released a day earlier than usual due to thanksgiving shortened week in the US.

USD/JPY Daily Outlook

Daily Pivots: (S1) 153.58; (P) 154.15; (R1) 154.75; More…

Intraday bias in USD/JPY remains neutral as consolidation from 156.74 is still extending. On the downside, break of 153.27 will bring deeper correction to 38.2% retracement of 139.57 to 156.74 at 150.18. Meanwhile, on the upside, firm break of 156.74 will resume the rally from 139.57 towards 161.95 high.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.