Yen fell broadly during Asian session today, reversing all of this week’s earlier gains. Market sentiment has calmed somewhat despite the escalation in Russia’s war in Ukraine, as there is no clear intensification toward a nuclear conflict. US Treasury yields have stabilized after yesterday’s decline, and Gold’s rebound has also stalled. Attention now turns to the upcoming UK CPI data.

UK inflation is expected to rebound from 1.7% to 2.2% in October, while core CPI is projected to slow slightly but remain elevated at 3.1%. The British Retail Consortium, along with over 80 retail companies, has requested a meeting with Finance Minister Rachel Reeves, warning that last month’s budget would result in higher prices, job losses, and reduced investment.

BoE Governor Andrew Bailey has indicated that, given the uncertainty surrounding the impact of the Autumn budget, a gradual approach to monetary easing is needed. Persistent inflation is likely to keep BoE cautious about an inflation resurgence, leaning toward another pause at the December meeting.

Overall in the currency markets for the week so far, Aussie is the strongest one followed by Loonie and then Kiwi. Yen is the worst now, followed by Dollar and then Euro. Sterling and Swiss Franc are positioning in the middle. But almost all major pairs and crosses are still stuck inside last week’s range, indicating that consolidations remain in progress.

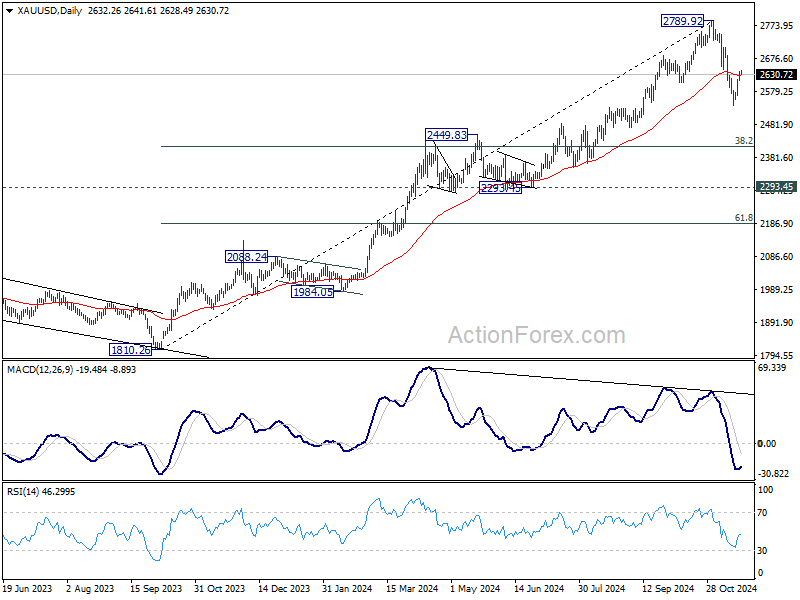

Technically, while Gold rebounded strongly this week, it’s still struggling to break through 55 D EMA (now at 2627.547). Price actions from 2789.92 are seen as a correction to whole five-wave rally from 18102.6. Rejection by the 55 D EMA will extend the decline to 38.2% retracement of 1810.26 to 2789.92 at 2415.68. Nevertheless, sustained trading above 55 D EMA will bring retest of 2789.92 high first, before starting the third leg to finish the corrective pattern.

In Asia, at the time of writing, Nikkei is down -0.36%. Hong Kong HSI is down -0.17%. China Shanghai SSE is up 0.20%. Singapore Strait Times is down -0.14%. Japan 10-year JGB yield is up 0.0073 at 1.072. Overnight, DOW fell -0.28%. S&P 500 rose 0.40%. NASDAQ rose 1.04%. 10-year yield fell -0.035 to 4.379.

Fed’s Schmid: Path and destination of rate cut yet to be determined

Kansas City Fed President Jeffrey Schmid highlighted in a speech overnight the decision to lower rates this year as a reflection of the “growing confidence” in inflation’s moderation.

This optimism, he explained, stems from signs that “both labor and product markets have come into better balance in recent months.”

While acknowledging this progress, Schmid cautioned, “It still remains to be seen how much further interest rates will decline or where they might eventually settle.”

Schmid also addressed concerns about the implications of large fiscal deficits on monetary policy. He emphasized that such deficits are not inherently inflationary, as long as Fed maintains its commitment to the 2% inflation target.

However, he warned that this approach could necessitate “persistently higher interest rates,” creating tensions with political authorities. He noted, “History has shown that efforts to avoid higher interest rates by accommodating deficits often result in higher inflation.”

Japan’s exports rebound by 3.1% yoy in Oct, but trade deficit persists

Japan’s exports rose 3.1% yoy in October, reaching JPY 9,427B, a strong recovery from the -1.7% yoy decline in September, which marked a 43-month low.

This rebound was primarily driven by a 1.5% yoy increase in shipments to China, buoyed by strong demand for chipmaking equipment. However, exports to the US, Japan’s largest trading partner, fell -6.2% yoy, reflecting weakness in auto shipments.

On the import side, growth remained modest at 0.4% yoy, totaling JPY 9,888B. This resulted in a trade deficit of JPY -461B for the month, the fourth straight month of shortfall.

Seasonally adjusted data showed exports declining -0.7% mom to JPY 8,882B, while imports ticked up 0.2% mom to JPY 9,239B, leading to a seasonally adjusted trade deficit of JPY -358B.

Australia Westpac leading index hits 0.26%, decisive breakaway from year-long sluggishness

Australia’s Westpac Leading Index moved decisively into positive territory in October, rising from -0.20% in September to +0.26%.

This marks a significant shift, as the index had been hovering in slight negative territory, between -0.3% and flat, for most of the past year. The October reading is not only the first clear above-trend result since November 2023 (+0.16%) but also the strongest since July 2022 (+0.63%).

The improvement in the index provides a “constructive signal” for the economy’s future momentum. Westpac’s outlook aligns with this shift, forecasting an acceleration in economic growth from a nadir of 1.0% in mid-2024 to 1.5% by year-end and 2.4% by the end of 2025.

Looking ahead

UK CPI is the main focus in European session while PPI will also be featured. Germany will release PPI.

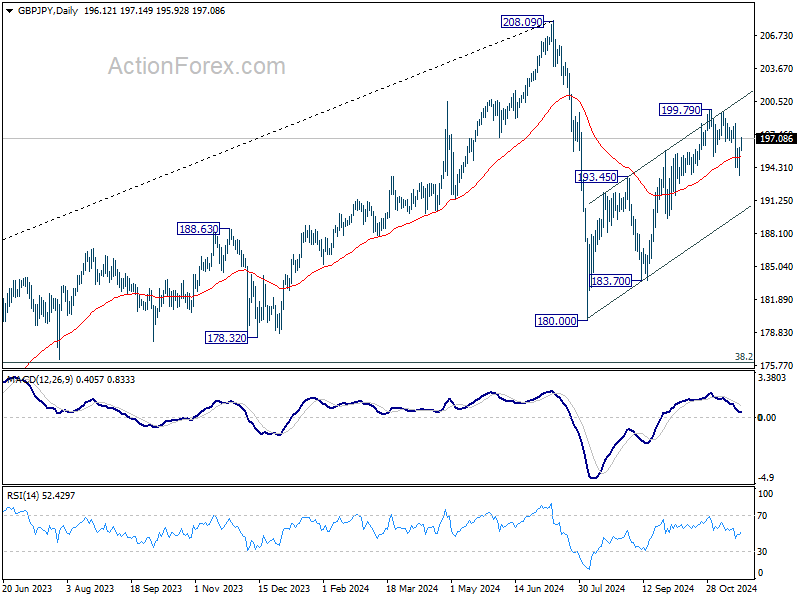

GBP/JPY Daily Outlook

Daily Pivots: (S1) 194.35; (P) 195.37; (R1) 197.16; More…

GBP/JPY’s strong rebound an break of 196.13 minor resistance suggests that pull back from 199.79 has already completed. The development also revive near term bullishness. Intraday bias is back on the upside for retesting 199.79 resistance first. Firm break there will rebound whole rebound from 180.00.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.