Sterling surged notably today and reached its highest level against Dollar since March 2022. The move followed BoE’s decision to hold interest rates steady as expected. The surprise came from Deputy Governor Dave Ramsden, who chose not to vote for a rate cut. The overall tone from BoE suggests that while further rate cuts are still on the horizon, they will likely proceed with caution. Concerns over persistently high inflation, especially in the services sector, remain a key issue for policymakers. For now, November is still seen as the most likely time for the next rate cut, but the path forward is far from set in stone.

Meanwhile, US markets seem to have come to terms with yesterday’s 50 bps rate cut by Fed. Stock futures point to a sharp rally, with both DOW and S&P 500 poised to hit new all-time highs. At the same time, 10-year Treasury yields surged past 3.75%. Fed fund futures now price in a 67% chance of a smaller 25bps cut in November. The mix of rising stock prices, higher yields, and fed pricing reflects the market’s confidence in Fed’s strategy, with Jerome Powell having successfully conveyed that the aggressive rate cut was a preemptive measure rather than a panic reaction to economic weakness. Investors remain optimistic even with a gradual pace of easing moving forward.

Overall, Aussie and Kiwi have outpaced Sterling as the day’s strongest performers so far, buoyed by risk-on sentiment. Aussie received additional support from strong employment data released earlier in the Asian session. Meanwhile, Yen and Swiss Franc are the weakest performers, reacting to the positive market sentiment and rising US and European yields. Dollar is also softening but cushioned by rising yields, while Euro and Canadian Dollar are in the middle of the pack.

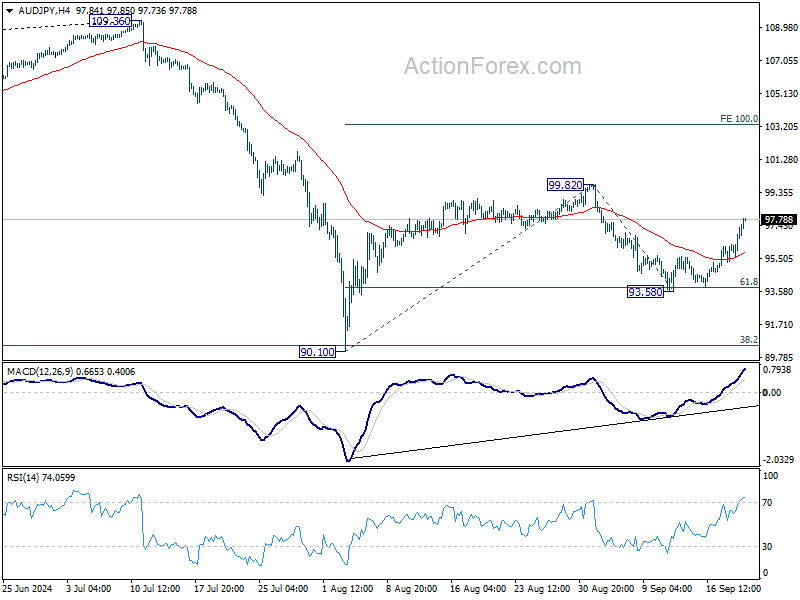

Technically, AUD/JPY is currently the top mover of the day, and the strong rally suggests that pull back from 99.82 has completed at 93.58 already, after drawing support from 61.8% retracement of 90.10 to 99.82. Further rise is now expected as long as 55 4H EMA holds (now at 95.88). Firm break of 99.82 will resume the whole rebound from 90.10. and target 100% projection of 90.10 to 99.82 from 93.58 at 103.30. Japan’s CPI release and BoJ rate decision could both be the trigger of the next move.

In Europe at the time of writing, FTSE is up 0.98%. DAX is up 1.57%. CAC is up 1.95%. UK 10-year yield is up 0.050 at 3.896. Germany 10-year yield is up 0.005 at 2.202. Nikkei rose 2.13%. Hong Kong HSI rose 2.00%. China Shanghai SSE rose 0.69%. Singapore Strait Times rose 1.13%. Japan 10-year JGB yield rose 0.0268 to 0.854.

US jobless claims falls to 219k, vs exp 232k

US initial jobless claims fell -12k to 219k in the week ending September 14, below expectation of 232k. Four-week moving average of initial claims fell -3.5k to 227.5k.

Continuing claims fell -14k to 1829k in the week ending September 7. Four-week moving average of continuing claims fell -6.5k to 1844k.

BoE holds rates steady at 5% by hawkish 8-1 vote

BoE opted to keep the Bank Rate unchanged at 5.00%, as expected, with an 8-1 vote. Swati Dhingra, a known dove, was the only member voting for a 25bps rate cut. Deputy Governor Dave Ramsden, who has consistently supported cuts since May, chose not to vote for a reduction this time.

In its statement, BoE noted that UK economic indicators have shown “limited news” relative to expectations outlined in the August MPR. Inflation stood at 2.2% in August and is anticipated to rise to around 2.5% by year-end as the effects of last year’s energy price declines drop out of the annual comparison. Services inflation remains notably elevated at 5.6%, while private sector wage growth slowed to 4.9% in the three months to July.

BoE emphasized that “absence of material developments”, it will continue to follow a “gradual approach” to unwinding policy restrictions. Monetary policy is expected to stay restrictive for a sufficiently long period until inflation risks subside, ensuring it returns to the 2% target. The central bank reaffirmed its commitment to closely monitor inflation persistence and determine the necessary level of restrictiveness “at each meeting.”

ECB’s Schnabel: Sticky services inflation persists, wage growth expected to ease

In a speech today, ECB Executive Board member Isabel Schnabel noted the ongoing challenge of “sticky” services inflation, which continues to keep headline inflation elevated. She highlighted that price pressures within the services sector are “broad-based and global,” and that the momentum remains high, well above levels that would be consistent with price stability. This persistent inflation in services is a key concern for the ECB’s outlook.

However, there is some optimism regarding easing wage pressures. Schnabel pointed to expectations that wage growth will slow as the effects of past price shocks begin to fade. Additionally, firms are projecting moderation in selling price increases, as “profit margins buffer higher wages”. She also noted that while demand for services has remained resilient, there are signs it is beginning to soften.

Schnabel also addressed the risks posed by geopolitical uncertainty, stating that it continues to be a significant factor influencing inflationary pressures. She cautioned that inflation perceptions remain high, which makes inflation expectations more “fragile to new shocks.”

SECO: Swiss economic growth sluggish in 2024, moderate recovery expected in 2025

Switzerland’s State Secretariat for Economic Affairs forecasts the economy to perform “considerably below average” in 2024, with modest growth expected to pick up in 2025. Adjusted for major sporting events, GDP growth is projected to be at 1.2% for 2024, unchanged from June’s estimates. However, the outlook for 2025 has been slightly downgraded to 1.6%, compared to June forecast of 1.7%.

Inflation is now expected to decline faster than previously thought, with projections for 2024 revised down to 1.2% (from 1.4% in June) and 0.7% for 2025 (down from 1.1%). This easing of inflationary pressures reflects lower price growth, especially in sectors impacted by the strong appreciation of the Swiss Franc.

SECO acknowledged the challenges posed by sluggish economic activity in Europe, which, alongside the real appreciation of the Swiss Franc, is straining export-sensitive sectors in Switzerland this year. Looking ahead, gradual recovery in Europe is expected to support Swiss exports and boost investments in 2025, helping to stabilize growth across key sectors.

New Zealand GDP contracts – 0.2% qoq in Q2, manufacturing offers some resilience

New Zealand’s GDP contracted by -0.2% qoq in Q2, slightly better than the expected -0.4% qoq decline. Despite the overall negative figure, 7 out of 16 industries posted increases, with manufacturing leading the growth.

GDP per capita also saw a decline, falling by -0.5%, marking the fourth consecutive quarter of contraction in this metric. The last time GDP per capita increased was back in Q3 2022.

On the expenditure side, GDP was flat for the quarter, showing no growth or contraction at 0.0%. Household spending, however, provided a small positive with a 0.4% increase. Real gross national disposable income was also flat at 0.0%, reflecting limited income growth in the face of economic headwinds.

Australia’s employment grows 47.5k in Aug, labor market remains tight

Australia’s employment grew by a robust 47.5k in August, significantly exceeding expectations of 25.3k. While full-time employment declined slightly by -3.1k, part-time jobs saw a sharp increase of 50.6k, boosting the overall figure. The employment-to-population ratio edged up by 0.1% to 64.3%, just shy of the record high of 64.4% set in November 2023.

Unemployment rate held steady at 4.2%, as anticipated, with the number of unemployed individuals falling by -10.5k, a -1.6% mom decline. Participation in the labor force remained strong, with the participation rate unchanged at 67.1%. Additionally, monthly hours worked rose by 0.4% mom, reflecting continued labor demand.

Kate Lamb, head of labor statistics at ABS, commented: “The employment and participation measures remain historically high, while unemployment and underemployment measures are still low, especially compared with what we saw before the pandemic. This suggests the labor market remains relatively tight.”

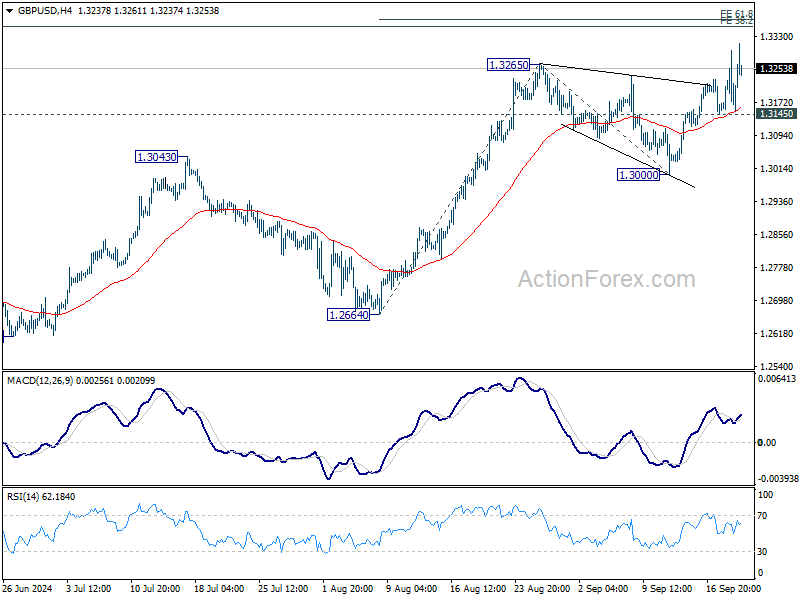

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3145; (P) 1.3221; (R1) 1.3290; More…

Intraday bias in GBP/USD remains on the upside at this point. Current rally should target 61.8% projection of 1.2664 to 1.3265 from 1.3000 at 1.3371 in the near term. Firm break there will pave the way to 100% projection at 1.3601 next. On the downside, however, break of 1.3145 support will turn bias to the downside for deeper pullback to 1.3000 support next.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. Sustained break there will target 61.8% projection at 1.4022. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.

Economic Indicators Update

| GMT | CCY | EVENTS | ACT | F/C | PP | REV |

|---|---|---|---|---|---|---|

| 22:45 | NZD | GDP Q/Q Q2 | -0.20% | -0.40% | 0.20% | 0.10% |

| 01:30 | AUD | Employment Change Aug | 47.5K | 25.3K | 58.2K | 48.9K |

| 01:30 | AUD | Unemployment Rate Aug | 4.20% | 4.20% | 4.20% | |

| 06:00 | CHF | Trade Balance (CHF) Aug | 4.58B | 5.05B | 4.89B | 4.88B |

| 07:00 | CHF | SECO Economic Forecasts | ||||

| 08:00 | EUR | Eurozone Current Account (EUR) Jul | 39.6B | 40.3B | 50.5B | |

| 11:00 | GBP | BoE Interest Rate Decision | 5.00% | 5.00% | 5.00% | |

| 11:00 | GBP | MPC Official Bank Rate Votes | 0–1–8 | 0–2–7 | 0–5–4 | |

| 12:30 | USD | Initial Jobless Claims (Sep 13) | 219K | 232K | 230K | 231K |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Sep | 1.7 | 2.4 | -7 | |

| 12:30 | USD | Current Account (USD) Q2 | -266.8B | -260B | -238B | -241B |

| 14:00 | USD | Existing Home Sales Aug | 3.85M | 3.95M | ||

| 14:30 | USD | Natural Gas Storage | 53B | 40B |