Bank of England (BoE) Governor Andrew Bailey explains the decision to lower the policy rate by 25 basis points to 5% in August and responds to questions from the press.

BoE press conference key quotes

“Services price inflation may rise slightly in August before easing in the rest of the year.”

“Services inflation excluding volatile components, such as airfares and hotels, may be a better guide.”

“We need to watch services prices very carefully.”

“We should not adjust our course with every data surprise that comes in.”

“We still face a question on whether persistent component of inflation is on course to decline to level consistent with 2% inflation.”

“Unclear if decline in persistence is baked in, needs period of slack, or needs period of tighter for longer policy.”

“We are making good progress returning inflation to 2% target sustainably.”

“Possible UK’s natural rate of unemployment may have risen in recent years.”

“We give some weight to alternative less benign inflation persistence scenario.”

“MPC continues to remain highly alert to risks of inflation persistence.”

“BoE goes meeting to meeting, making judgement based on evidence.”

“BoE takes the lead from measures of private sector pay.”

“Public sector pay does have an impact on demand.”

“We do not have the full story, do not know how public sector pay rise will be funded.”

“Will give no view on path of rates.”

This section below was published at 11:00 GMT to cover the Bank of England’s policy decisions and the initial market reaction.

The Bank of England (BoE) announced on Thursday that it cut the policy rate by 25 basis points to 5% from 5.25%. Policymakers voted 5-4 in favor of the decision, with BoE Monetary Policy Committee (MPC) members Pill, Greene, Mann and Haskel voting to keep rates on hold.

Follow our live coverage of the Bank of England’s policy announcements and the market reaction.

BoE policy statement key takeaways

“Decision was finely balanced for some MPC members who voted to cut rates.”

“CPI expected to rise to around 2.75% in H2 2024 as energy base effects fade.”

“Expect slack to emerge as GDP slows and unemployment rises.”

“Risk that inflation pressures from 2nd-round effects endure into medium term.”

“BoE forecast shows CPI in two years’ time at 1.7% (May forecast: 1.9%), based on market interest rates.”

“BoE forecast shows CPI in one year’s time at 2.4% (May forecast: 2.6%), based on market interest rates and modal forecast.”

“BoE estimates GDP +0.7% QQ in Q2 2024 (June forecast: +0.5%), sees Q3 +0.4% QQ and Q4 +0.2%.”

“BoE forecasts GDP growth in 2024 +1.25% (May forecast: 0.5%), 2025 1% (May: 1%), 2026 1.25% (May: 1.25%), based on market rates.”

“BoE forecast shows CPI in three years’ time at 1.5% (May forecast: 1.6%), based on market interest rates.”

“BoE forecasts unemployment rate 4.4% in Q4 2024% (May forecast: 4.4%); Q4 2025 4.7% (May: 4.7%); Q4 2026 4.7% (May: 4.8%).”

“Market rates show slightly more BoE loosening than in May, show bank rate at 4.9% in Q4 2024, 4.1% in Q4 2025, 3.7% in Q4 2026 (May: 4.8% in Q4 2024, 4.3% in Q4 2025, 3.8% in Q4 2026).”

“BoE estimates private sector regular wage growth 5.0% YY in Q4 2024 (May forecast: 5.0%), Q4 2025 3.0% (May: 3.0%); Q4 2026 2.75% (May: 2.75%).”

“The MPC will ensure bank rate is restrictive for sufficiently long until the risks to inflation returning to the 2% target had dissipated further.”

“MPC will decide degree of monetary policy restrictiveness at each meeting.”

“There is uncertainty about interaction between cutting bank rate and quantitative tightening.”

“If QT impact is larger than expected, level of bank rate provides scope for looser policy if needed.”

Market reaction to BoE policy announcements

GBP/USD stays under bearish pressure following the BoE policy decisions and was last seen losing 0.75% on the day at 1.2760.

British Pound PRICE Today

The table below shows the percentage change of British Pound (GBP) against listed major currencies today. British Pound was the weakest against the Swiss Franc.

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | 0.32% | 0.74% | 0.12% | 0.11% | 0.18% | 0.12% | -0.14% | |

| EUR | -0.32% | 0.42% | -0.23% | -0.22% | -0.13% | -0.19% | -0.46% | |

| GBP | -0.74% | -0.42% | -0.65% | -0.63% | -0.55% | -0.61% | -0.87% | |

| JPY | -0.12% | 0.23% | 0.65% | -0.01% | 0.07% | -0.04% | -0.28% | |

| CAD | -0.11% | 0.22% | 0.63% | 0.00% | 0.08% | 0.02% | -0.24% | |

| AUD | -0.18% | 0.13% | 0.55% | -0.07% | -0.08% | -0.06% | -0.32% | |

| NZD | -0.12% | 0.19% | 0.61% | 0.04% | -0.02% | 0.06% | -0.26% | |

| CHF | 0.14% | 0.46% | 0.87% | 0.28% | 0.24% | 0.32% | 0.26% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the British Pound from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent GBP (base)/USD (quote).

This section below was published at 06:00 GMT as a preview of the Bank of England’s policy decisions.

- Odds for a rate cut by the Bank of England remain divided.

- UK disinflationary pressure stalled in June.

- GBP/USD appears to be supported so far by 1.2800 region.

Consensus among market participants appears pretty divided around the imminent interest rate decision by the Bank of England (BoE) arriving on Thursday. It is worth recalling that the central bank maintained its policy rate unchanged at 5.25% in the last seven meetings, although renewed repricing by investors seems to favour a potential 25 bps rate cut this week.

The BoE’s MPC vote is expected to be a close call

The Bank of England’s policy decision is expected to be a close call, while market pricing is now signalling a 63% probability for a quarter-point cut, and the Monetary Policy Committee (MPC) vote could come as close as 5-4 in favouring a reduction of the central bank’s rate.

Let’s remember that at the June gathering, the MPC decided to keep rates unchanged with a 7-2 vote. However, those who voted to hold rates indicated that their decision was “finely balanced,” hinting at the idea that a rate cut could be in the offing.

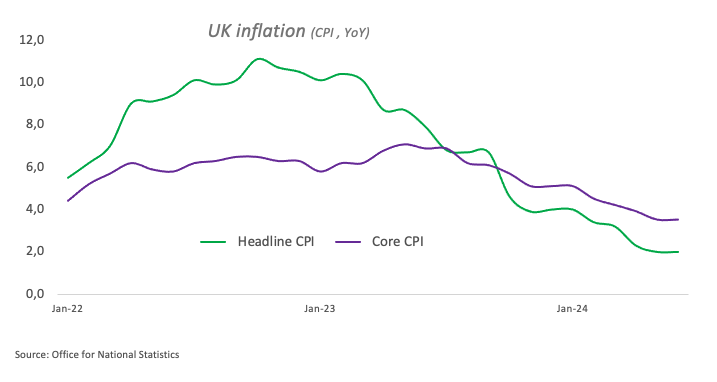

Disinflationary pressure seems to have hit a wall in June after the headline Consumer Price Index (CPI) rose by 2.0% over the previous 12 months, matching May’s reading. The core CPI, which excludes food and energy costs, also matched the previous month’s prints, advancing by 3.5%.

In the same line, service inflation rose by 5.7% YoY from a year earlier and remains quite above the central bank’s 5.1% projection.

Still around inflation, the BoE’s Chief Economist, Huw Pill, argued that the bank was nearing a decision to cut interest rates, though service price inflation and wage growth remained troublingly high. It is worth noting that Pill joined the majority of his colleagues in June in voting to keep interest rates at 5.25%.

Her colleague Catherine Mann emphasized the strong price pressure in the UK economy, signalling that she is unlikely to support an interest rate cut in August. Mann added that the recent drop in domestic inflation was merely “touch and go” and predicted that inflation would likely exceed that rate for the remainder of the year.

Favouring a rate cut this week, Rabobank’s Senior Macro Strategist Stefan Koopman said, “We anticipate a 25bp cut to the Bank rate, bringing it to 5.00%, marking the start of a gradual easing cycle with 25bp cuts each quarter. However, there is a risk that officials may want to see another month of data first.”

Additionally, analysts at TD Securities argued, “We expect a 25bps cut at the August MPC meeting, with a narrow 5-4 vote. That said, uncertainty is high, not only due to sticky service inflation prints but also due to compositional changes on the committee. The message will likely be a cautious one, as the MPC should not want to signal consecutive cuts at this stage.”

How will the BoE interest rate decision impact GBP/USD?

Despite disinflationary pressures losing momentum in June, market participants seem to lean toward a rate cut at the BoE’s monetary policy meeting on August 1 at 11 GMT.

FXStreet Senior Analyst Pablo Piovano sees the British Pound coming under renewed downside pressure in the event of a rate cut, as such a scenario is only partially supported by market forecasts.

Pablo adds that the GBP/USD rally experienced in the first half of July that lifted Cable to fresh 2024 peaks near 1.3050 was almost exclusively on the back of accelerated weakness in the US Dollar (USD) following investors’ repricing of a rate cut by the Federal Reserve (Fed) in September.

Against that backdrop, extra losses could motivate GBP/USD to break below the weekly low of 1.2806 (July 29) and challenge the provisional support at the 55-day and 100-day SMAs at 1.2776 and 1.2682, respectively. The breach of that region exposes a probable slide to the July low of 1.2615 (July 2), which appears reinforced by the proximity of the key 200-day SMA (1.2836).

On the upside, Pablo sees the initial stop for bulls at the 2024 peak of 1.3044 (July 17).