Dollar took a significant hit in early US session, following the release of weaker-than-expected consumer inflation data. A particularly notable point is that headline CPI remained flat for the month, a scenario not seen since November last year. Annual core CPI also continued its steady disinflationary trend. In response to this data, US stock futures jumped, while the yield on the 10-year Treasury note dropped sharply.

This shift in inflation data has set the stage for heightened anticipation around the looming FOMC announcement. While it’s widely expected that Fed will hold interest rates steady, the real focus will be on the new economic projections and the updated dot plot. These will provide insights into Fed’s outlook on future rate moves. If the projections show that most policymakers anticipate two rate cuts this year, and fewer see the need for another rate hike, Dollar’s downward momentum could continue.

Overall in the currency markets, Dollar has become the weakest performer of the week, even more so than the politically troubled Euro. Yen is trailing closely behind Euro as the third weakest currency. On the other hand, New Zealand Dollar and Australian Dollar are showing the most strength, followed by British Pound. Canadian Dollar and Swiss Franc are holding middle positions in terms of performance.

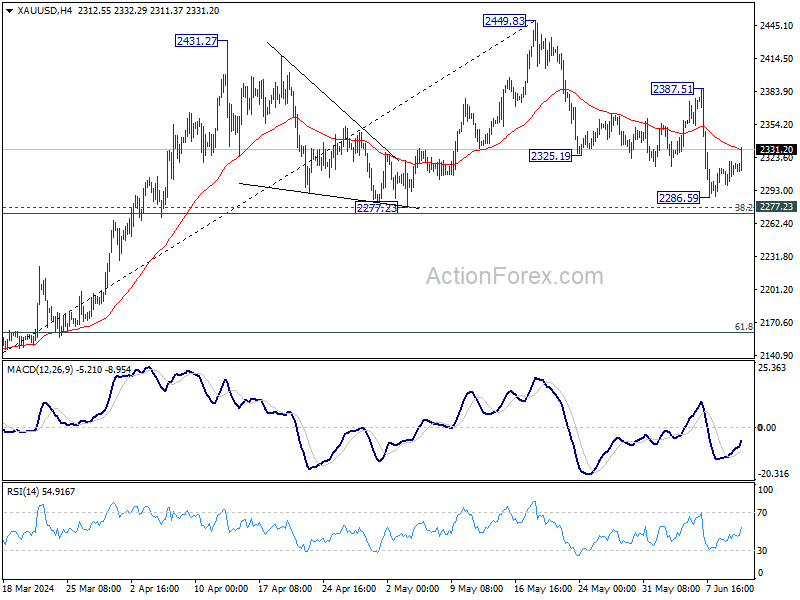

Technically, Gold also jumped on Dollar’s sell-off. Sustained trading above 55 4H EMA (now at 2331.01) will argue that correction from 2449.83 has completed with three waves down to 2286.59, after defending 2277.23 cluster support. Further rise should then be seen towards 2387.51. Firm break there will strengthen this bullish case and target 2449.83 high.

In Europe, at the time of writing, FTSE is up 1.06%. DAX is up 1.18%. CAC is up 1.03%. UK 10-year yield is down -0.100 at 4.177. Germany 10-year yield is down -0.069 at 2.565. Earlier in Asia, Nikkei fell -0.66%. Hong Kong HSI fell -1.31%. China Shanghai SSE rose 0.31%. Singapore Strait Times fell -0.05%. Japan 10-year JGB yield fell -0.0273 to 0.989.

US CPI at 0.0% mom, 3.3% yoy in May, below expectations

US CPI was flat at 0.0% mom in May below expectation of 0.2% mom. CPI core (all items less food and energy)rose 0.2% mom, below expectation of 0.3% mom. Food prices rose 0.1% mom, while energy prices fell -2.0% mom.

For the 12-month period, CPI slowed from 3.4% yoy to 3.3% yoy, below expectation of 3.4% yoy. CPI core decelerated from 3.6% yoy to 3.4% yoy, below expectation of 3.5% yoy. Food prices was up 2.1% yoy while energy prices rose 3.7% yoy.

UK GDP holds steady in April as services offset declines in production and construction

UK GDP showed no growth in April, aligning with market expectations. The data reveals a mixed picture, with certain sectors compensating for declines in others.

Services output grew by 0.2% mom, marking its fourth consecutive month of growth, underscoring the resilience of the services sector. Conversely, production output fell by -0.9% mom, reflecting ongoing challenges in the industrial sector. Construction output declined by -1.4% mom, continuing its downward trend for the third straight month.

Looking at the three-month period from February to April compared to the preceding three months from November to January, GDP grew by 0.7%. Within this period, services expanded by 0.9%, driven by consistent monthly gains. Production also showed a positive trend with a 0.7% increase, despite the monthly volatility. However, construction suffered a -2.2% decline, indicating sustained weakness in this sector.

Japan’s CGPI rises to 2.4% yoy, highest in nine months

Japan’s corporate goods price index accelerated from 1.1% yoy to 2.4% yoy in May, surpassing expectations of 2.0% yoy increase. This marks the fastest annual rise in nine months. The Yen-based import goods price index also rose 6.9% yoy , up from a 6.6% yoy gain in April, indicating that the Yen’s depreciation is driving up the cost of raw material imports.

In a related development, a draft government policy blueprint released today emphasizes Japan’s commitment to using “all policy tools” to sustain wage hikes. These wage increases are deemed crucial for ending deflation and achieving consistent economic growth above 1%, despite the country’s rapidly shrinking population.

China’s CPI stagnates in May, PPI remains in negative territory

China’s CPI rose 0.3% yoy in May, unchanged from the previous month’s reading and falling short of the expected 0.4% yoy increase. Food prices declined by -2.0% yoy, while non-food prices saw a modest increase of 0.8% yoy. Prices of consumer goods remained flat, and service prices rose by 0.8% yoy .

On a monthly basis, CPI edged down by -0.1% mom, missing the expectation of no change. Food prices were stable, but non-food prices fell by -0.2% mom, consumer goods prices decreased by -0.1% mom, and service prices also fell by 0.1% mom.

PPI dropped by -1.4% yoy, an improvement from the previous month’s -2.5% yoy decline and better than the expected -1.8% yoy fall. Despite this improvement, PPI has been negative for the 20th consecutive month, indicating ongoing deflationary pressures in the industrial sector.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2713; (P) 1.2732; (R1) 1.2759; More…

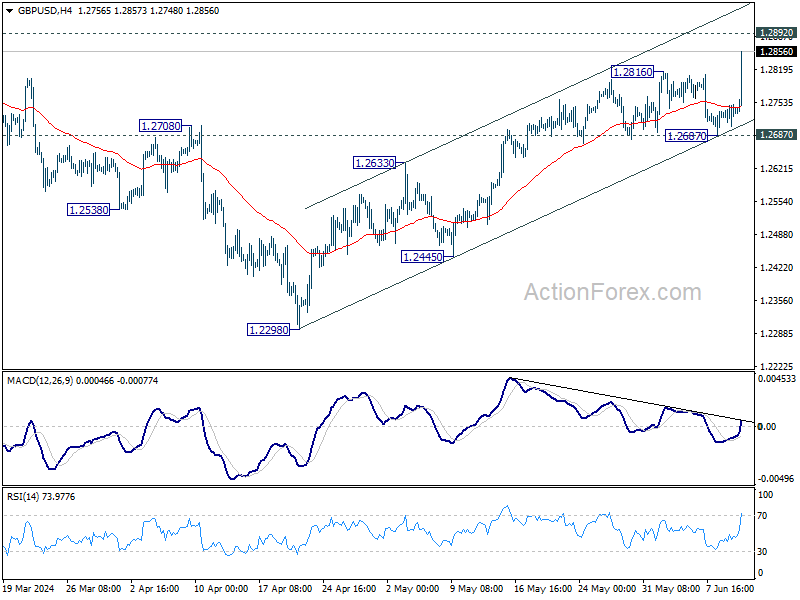

GBP/USD’s strong rally and firm break of 1.2816 support confirms resumption of rise from 1.2298. Intraday bias is back on the upside for 1.2892 resistance. Decisive break there will strengthen the case that correction from 1.3141 has completed, and bring further rally to retest this high. On the downside, break of 1.2687 support is needed to indicate short term topping. Otherwise, outlook will stay bullish in case of retreat.

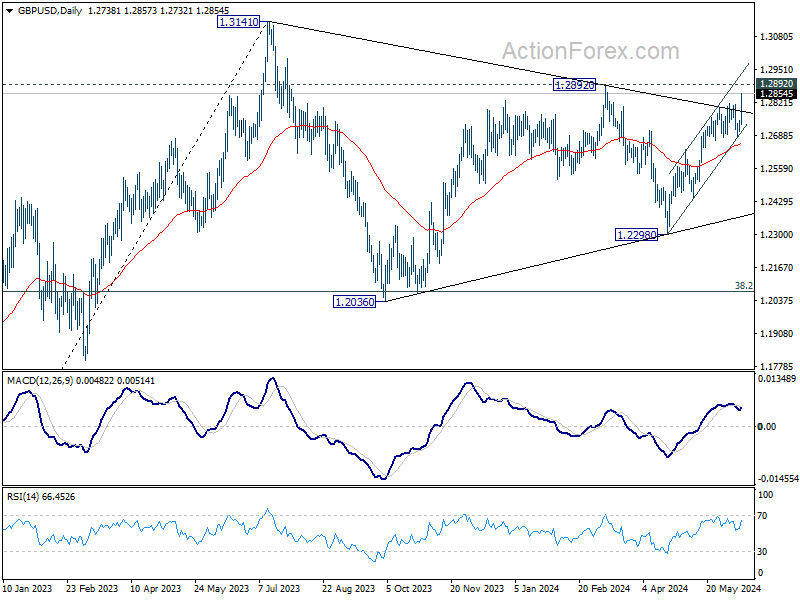

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2445 support will extend the corrective pattern with another decline instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y May | 2.40% | 2.00% | 0.90% | 1.10% |

| 01:30 | CNY | CPI Y/Y May | 0.30% | 0.40% | 0.30% | |

| 01:30 | CNY | PPI Y/Y May | -1.40% | -1.80% | -2.50% | |

| 06:00 | GBP | GDP M/M Apr | 0.00% | 0.00% | 0.40% | |

| 06:00 | GBP | Industrial Production M/M Apr | -0.90% | -0.10% | 0.20% | |

| 06:00 | GBP | Industrial Production Y/Y Apr | -0.40% | 0.30% | 0.50% | |

| 06:00 | GBP | Manufacturing Production M/M Apr | -1.40% | -0.20% | 0.30% | |

| 06:00 | GBP | Manufacturing Production Y/Y Apr | 0.40% | 1.60% | 2.30% | |

| 06:00 | GBP | Goods Trade Balance (GBP) Apr | -19.6B | -14.2B | -14.0B | |

| 06:00 | EUR | Germany CPI M/M May F | 0.10% | 0.10% | 0.10% | |

| 06:00 | EUR | Germany CPI Y/Y May F | 2.40% | 2.40% | 2.40% | |

| 12:30 | USD | CPI M/M May | 0.00% | 0.20% | 0.30% | |

| 12:30 | USD | CPI Y/Y May | 3.30% | 3.40% | 3.40% | |

| 12:30 | USD | CPI Core M/M May | 0.20% | 0.30% | 0.30% | |

| 12:30 | USD | CPI Core Y/Y May | 3.40% | 3.50% | 3.60% | |

| 14:30 | USD | Crude Oil Inventories | -1.2M | 1.2M | ||

| 18:00 | USD | Fed Interest Rate Decision | 5.50% | 5.50% | ||

| 18:30 | USD | FOMC Press Conference |