In today’s Asian trading session, forex markets are experiencing a lull, with most of the major currency pairs and crosses moving within the boundaries set by yesterday’s trading ranges. The anticipated volatility sparked by the robust remarks from the heads of the ECB, Fed, BoE, and BoJ during the ECB forum overnight failed to materialize. Their unified message underscored the ongoing fight against inflation amidst a landscape of uncertainties, yet the markets remain unresponsive. While major US indexes closed with mixed results, Asian markets seem to lack a clear common trajectory.

Taking stock of the week’s movements thus far, Dollar leads as the strongest currency, displaying promising gains against commodity currencies. However, it would need to make further rally against Euro and Swiss Franc to substantiate its underlying strength. Euro trails as the second-strongest currency, followed the Swiss Franc, boosted partially by buying against the weakening Sterling. Australian and New Zealand Dollars sit at the bottom of the pack as the week’s worst performers, while Japanese Yen remains mixed, digesting its recent losses.

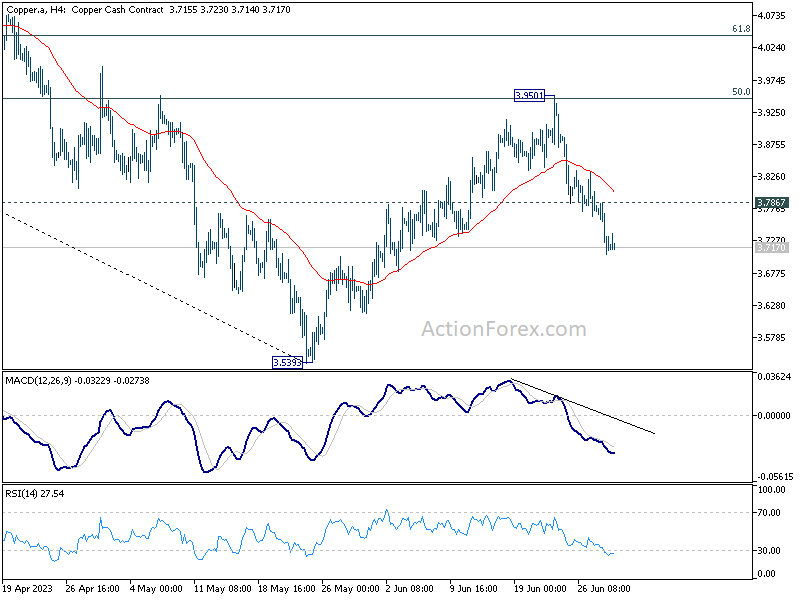

Technically, Copper’s fall from 3.9051 is extending and the development reinforces the case that corrective rebound from 3.5393 has completed already. Further decline is now in favor as long as 3.7867 minor resistance holds, back to retest 3.5393 low. Any downside acceleration could drag AUD/USD further towards 0.6457 support.

{kind=link}

In Asia, at the time of writing, Nikkei is up 0.37%. Hong Kong HSI is down -1.35%. China Shanghai SSE is down -0.18%. Singapore Strait Times is up 0.06%. Japan 10-year JGB yield is down -0.002 at 0.385. Overnight, DOW dropped -0.22%. S&P 500 dropped -0.04%. NASDAQ rose 0.27%. 10-year yield fell -0.058 to 3.710.

Japan retail sales rose 1.3% mom, 5.7% yoy, beat expectations

In the latest release from Japan, retail sales rose 1.3% mom, surpassing the anticipated increase of 0.8% mom. This growth also reflects a robust 5.7% yoy rise, again beating expectations of 5.2% year-on-year.

While inflation remaining above 3% mark could have been a contributing factor in boosting retail sales, there is evidence to suggest that return of overseas tourists is also playing a substantial role in stimulating economic activity.

Earlier reports from Japan National Tourism Organization highlighted that number of overseas visitors is nearing 70% of pre-pandemic levels as of May, indicating a resilient recovery of the tourism sector, and with it, potential for further economic growth.

In separate release, Consumer Confidence index nudged up from 36.0 to 36.2. This is the highest reading observed since January 2022, suggesting that households are more optimistic about the economy’s trajectory. This could potentially translate into a higher propensity to spend, further bolstering retail sales and overall economic performance in the coming months.

NZ ANZ business confidence rose to -18, subtle signs of easing inflation pressures

New Zealand ANZ Business Confidence Index improved notably from -31.1 to -18.0 in June, marking the highest level since November 2021. Furthermore, the outlook for their own activity rose from -4.5 to 2.7, turning positive for the first time in 14 months.

Digging into the details reveals a more nuanced picture. Despite the improved overall business sentiment, export intentions dipped from 2.0 to -1.8. However, there were more encouraging signs in other areas: investment intentions rose from -6.8 to -2.7, and employment intentions followed suit, moving from -5.7 to -3.5. Meanwhile, pricing intentions have shown a modest decline from 52.4 to 49.3.

On the inflation front, there are tentative signs that pressures might be easing slightly. Cost expectations dropped from 84.1 to 76.0, and inflation expectations decreased from 5.47% to 5.29%. There was also a slight improvement in profit expectations, which rose from -27.4 to -24.1.

Commenting on the results, ANZ noted, “for now, cautious optimism appears to be emerging that the worst could be past – but it’s conditional on those inflation indicators continuing to fall.”

Australia retail sales rose 0.7% mom, boosted by sales events

Australia retail sales turnover rose 0.7% mom to AUD 35.52B in May, well above expectation of 0.1% mom. Through the year, sales turnover was up 4.2% yoy.

Ben Dorber, ABS head of retail statistics, said: “Retail turnover was supported by a rise in spending on food and eating out, combined with a boost in spending on discretionary goods.

“This latest rise reflected some resilience in spending with consumers taking advantage of larger than usual promotional activity and sales events for May.”

Looking ahead

Eurozone economic sentiment, Germany CPI flash, UK M4 money supply and mortgage approvals will be released in European session. ECB will also publish monthly economic bulletin. Later in the day, US will release jobless claims, pending home sales and Q1 GDP final.

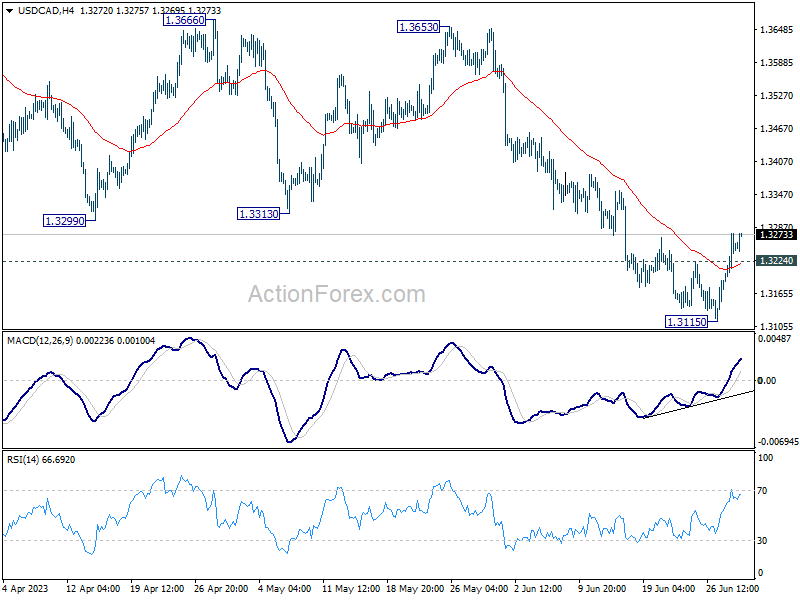

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3207; (P) 1.3242; (R1) 1.3294; More….

USD/CAD’s break of 1.3224 minor resistance should confirm short term bottoming at 1.3115, on bullish convergence condition in 4H MACD. Intraday bias is back on the upside for 1.3229 support turned resistance. Firm break there will extend the rebound to 55 D EMA (now at 1.3389). On the downside, break of 1.3115 is needed to confirm resumption of recent decline. Otherwise, more consolidative trading should be seen first, in case of retreat.

{kind=link}

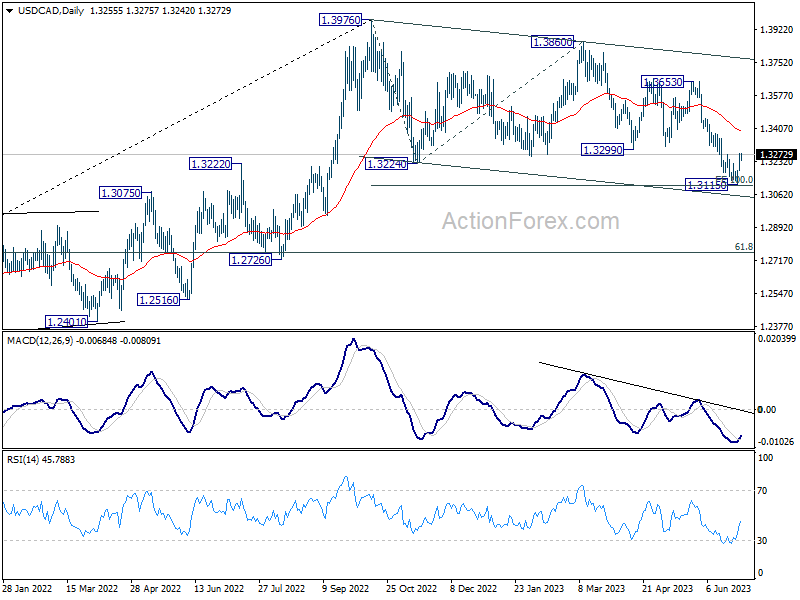

In the bigger picture, price actions from 1.3976 are still viewed as a correction to up trend from 1.2005 (2021 low), but chance of trend reversal is increasing with current decline. In either case, risk will stay on the downside as long as 1.3299 support turned resistance holds, even in case of strong rebound. Next target is 61.8% retracement of 1.2005 to 1.3976 at 1.2758. Sustained trading above 1.3229 will raise the chance that the correction has completed and turn focus back to 1.3653 resistance.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Retail Trade Y/Y May | 5.70% | 5.20% | 5.00% | 5.10% |

| 01:00 | NZD | ANZ Business Confidence Jun | -18 | -31.1 | ||

| 01:30 | AUD | Retail Sales M/M May | 0.70% | 0.10% | 0.00% | |

| 05:00 | JPY | Consumer Confidence Jun | 36.2 | 36.2 | 36 | |

| 08:00 | EUR | ECB Economic Bulletin | ||||

| 08:30 | GBP | Mortgage Approvals May | 50K | 49K | ||

| 08:30 | GBP | M4 Money Supply M/M May | -0.10% | 0.00% | ||

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Jun | 96 | 96.5 | ||

| 09:00 | EUR | Eurozone Industrial Confidence Jun | -5.5 | -5.2 | ||

| 09:00 | EUR | Eurozone Services Sentiment Jun | 5.5 | 7 | ||

| 09:00 | EUR | Eurozone Consumer Confidence Jun F | -16.1 | -16.1 | ||

| 12:00 | EUR | Germany CPI M/M Jun P | 0.20% | -0.10% | ||

| 12:00 | EUR | Germany CPI Y/Y Jun P | 6.30% | 6.10% | ||

| 12:30 | USD | Initial Jobless Claims (Jun 23) | 265K | 264K | ||

| 12:30 | USD | GDP Annualized Q1 F | 1.30% | 1.30% | ||

| 12:30 | USD | GDP Price Index Q1 F | 4.20% | 4.20% | ||

| 14:00 | USD | Pending Home Sales M/M May | -0.30% | 0.00% | ||

| 14:30 | USD | Natural Gas Storage | 83B | 95B |