Dollar is extending the near term pull back in Asian session today, driven by a combination of factors including a risk-on market sentiment, falling Treasury yields, and growing market expectations of a Federal Reserve “skip” in June. However, the greenback, along with other currencies, will be closely watching today’s non-farm payroll data for further direction. As it stands, Swiss Franc is trailing Dollar as the week’s second worst performer, followed by Euro. On the other hand, Sterling is actually the quiet star of the week, followed by Aussie and Loonie. Yen is currently mixed as near term consolidation extends.

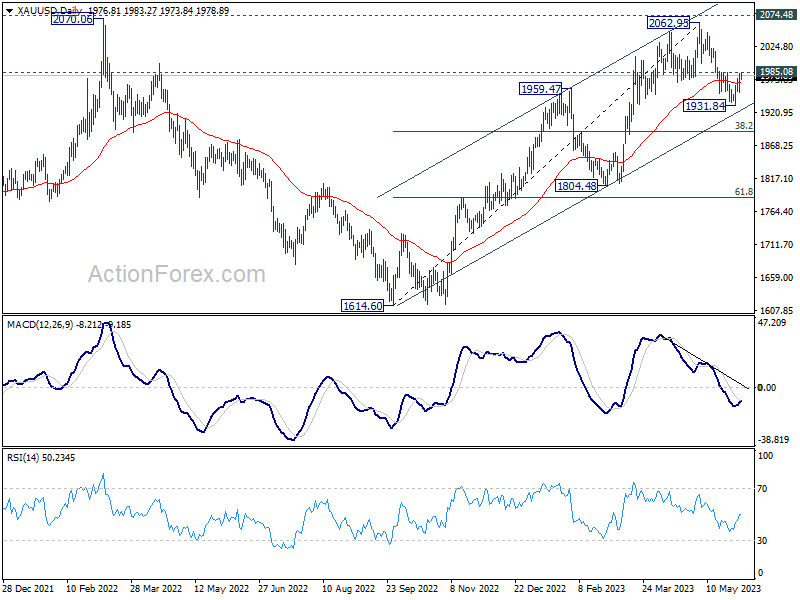

Technically, Gold is now eyeing 1985.08 minor resistance with current rebound. Break there will indicate that a short term bottoming is formed at 1931.84. More importantly, such development will keep the medium term rising channel intact. That is, rise from 1614.60 is indeed not over yet. Retest of 2062.95 or even 2074.48 record high could be seen soon, which could also correspond to near term selloff in Dollar.

{kind=link}

In Asia, at the time of writing, Nikkei is up 1.03%. Hong Kong HSI is up 3.79%. China Shanghai SSE is up 0.78%. Singapore Strait Times is up 0.24%. 10-year JGB yield is down -0.0074 at 0.413. Overnight, DOW rose 0.47%. S&P 500 rose 0.99%. NASDAQ rose 1.28%. 10-year yield dropped -0.029 to 3.608.

Fed Harker: We are clearly in restrictive, we can sit there for a while

Philadelphia Fed President Patrick Harker recommended a pause in interest rate hikes at the upcoming FOMC meeting, stating. “It’s time to at least hit the stop button for one meeting and see how it goes,” he said yesterday.

Harker also noted, “I think we are at the point, or very close to the point now, where we are clearly in restrictive territory, and we can sit there for a while,” he explained. “We don’t have to keep moving rates up, and then have to reverse course quickly.”

Looking ahead, Harker expects the US economy to grow less than 1% this year, and anticipates unemployment rate, currently at 3.4%, to increase to around 4.4%. Additionally, he forecasts a decrease in inflation to 3.5% this year and 2.5% next year, predicting it to reach Fed’s 2% target only by 2025.

BoJ Ueda: No time frame to achieve inflation target, but not so long as 10 years

In a parliamentary address today, BoJ Governor Kazuo Ueda said “The time it takes for the impact of monetary policy to appear on the economy could move around a lot depending on circumstances.”

“We therefore do not have any time frame in mind” in achieving the inflation target, he added.

“Having said that, our baseline view is that it won’t take so long as over 10 years. We’ll still seek to hit the target at the earliest date possible,” he remarked.

Ueda reiterated that the Bank of Japan’s purchases of Real Estate Investment Trusts (REITs) form part of their expansive monetary easing strategy. He noted, “We are conducting the purchases (of REITs) as part of our massive monetary easing program. Given it will take more time to achieve our price target, we will maintain the easy policy.”

US non-farm payroll in spotlight, NASDAQ presses key resistance

Today, market watchers are turning their attention to US non-farm payroll report, a key indicator of the health of the American labor market. Economists are forecasting job growth of around 180k in May, with the unemployment rate predicted to slightly increase from 3.4% to 3.5%. Meanwhile, average hourly earnings are expected to continue a trend of robust growth with another 0.3% mom rise.

Looking at some related economic data, ISM manufacturing employment index showed a modest rise from 50.2 to 51.4, while ADP private job data indicated a strong increase of 278k. The four-week moving average of initial jobless claims saw a slight dip from 239k to 230k. All these numbers suggest a job market that remains steady, showing no significant signs of weakening.

In terms of monetary policy, Fed funds futures are currently pricing in 76% probability that Fed will opt to “skip” a rate hike at the upcoming FOMC meeting on June 14. Nevertheless, there is still around a 60% chance of another 25bps increase in June to a range of 5.25-5.50%. Today’s data could significantly alter this picture if it brings any surprises.

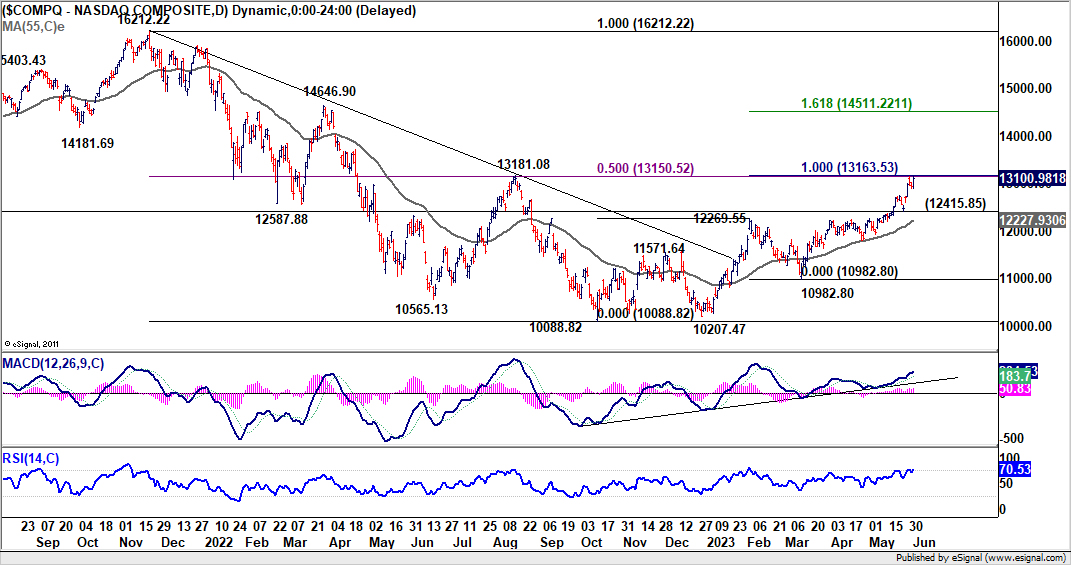

Over in the equity markets, NASDAQ is once again testing a crucial cluster resistance level at 13181.08, following a brief retreat earlier this week. The level represents 100% projection of 10088.82 to 12269.55 from 10982.80 at 13163.53, as well as 50% retracement of 16212.22 to 10088.82 at 13150.52.

Decisive breakthrough above this 13150/80 range would confirm underlying medium term bullish momentum in NASDAQ, potentially sparking upward acceleration towards 161.8% projection at 14511.22. Let’s see how NASDAQ reacts to today’s data.

{kind=link}

AUD/USD Daily Report

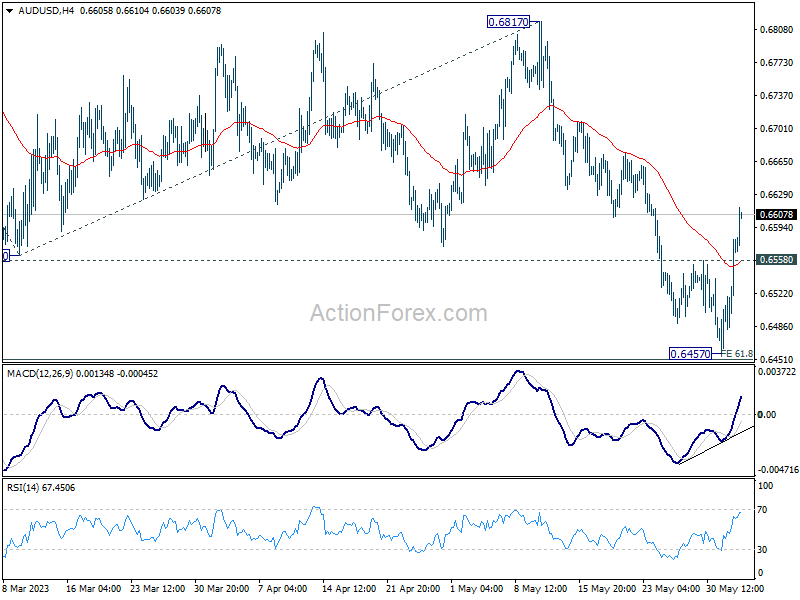

Daily Pivots: (S1) 0.6511; (P) 0.6547; (R1) 0.6608; More…

AUD/USD’s strong break of 0.6558 minor resistance confirm short term bottoming at 0.6457, just ahead of 61.8% projection of 0.7156 to 0.6563 from 0.6817 at 0.6451. Intraday bias is back on the upside for 55 D EMA (now at 0.6659). Sustained break there will target 0.6817 resistance next. Nevertheless, rejection by 55 D EMA will keep near term outlook bearish. Firm break of 0.6451 will resume the fall from 0.7156 to 100% projection at 0.6224.

{kind=link}

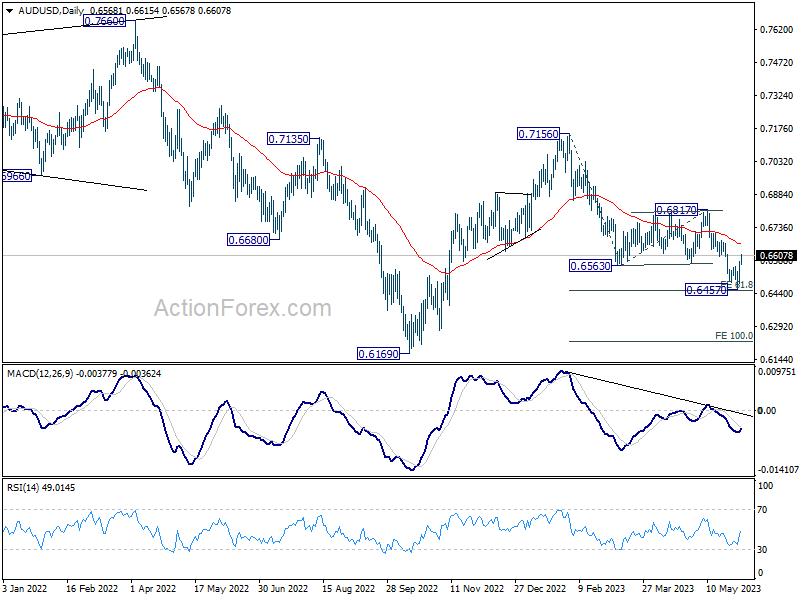

In the bigger picture, rejection by 55 W EMA (now at 0.6822) keeps medium term outlook bearish. Current development suggests that down trend from 0.8006 (2021 high) is possibly still in progress. Retest of 0.6169 (2022 low) should be seen next. Firm break there will confirm down trend resumption. For now, this will remain the favored case as long as 0.6817 resistance holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Terms of Trade Index Q1 | -1.50% | -1.10% | 1.80% | 1.50% |

| 23:50 | JPY | Monetary Base Y/Y May | -1.10% | -1.40% | -1.70% | |

| 06:45 | EUR | France Industrial Output M/M Apr | 0.30% | -1.10% | ||

| 12:30 | USD | Nonfarm Payrolls May | 180K | 253K | ||

| 12:30 | USD | Unemployment Rate May | 3.50% | 3.40% | ||

| 12:30 | USD | Average Hourly Earnings M/M May | 0.30% | 0.50% |