Dollar appears to be taking a breather, experiencing a broad decline in month-end trading as it reverses some of its recent gains. The initial support from the debt ceiling deal seems to be waning, while market participants are adopting a cautious stance ahead of this week’s crucial non-farm payroll data. The figures are expected to influence bets on whether Fed will hike rates again in June.

Commodity currencies are feeling the heat, underperforming due to uninspiring risk sentiment. Meanwhile, British Pound has been rallying in the European session, helping to lift both Euro and Swiss Franc. Japanese Yen is also furthering its recovery, buoyed by pullback in benchmark yields.

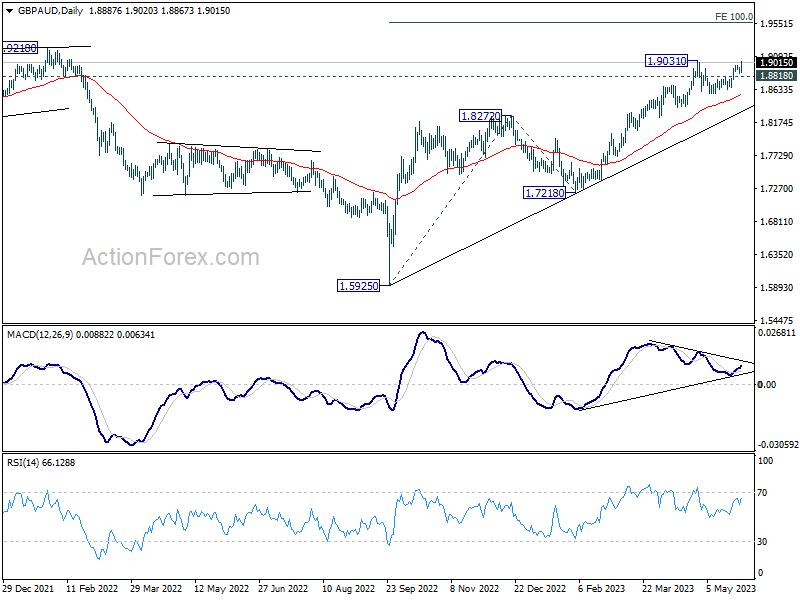

Technically, GBP/AUD is tentatively seen as ready for upside break out. Firm break of 1.9031 will resume whole up trend from 1.5925. Next target will be 100% projection of 1.5925 to 1.8272 from 1.7218 at 1.9565. However, break of 1.8818 minor support will delay the bullish case, and bring another fall to extend the consolidation pattern from 1.9031 first.

In Europe, at the time of writing, FTSE is down -0.61%. DAX is up 0.44%. CAC is down -0.53%. Germany 10-year yield is down -0.0584 at 2.385. Earlier in Asia, Nikkei rose another 0.30%. China Shanghai SSE rose 0.09%. Hong Kong HSI rose 0.24%. Singapore Strait Times dropped -0.24%. Japan 10-year JGB yield rose 0.0004 to 0.436.

{kind=link}

Eurozone economic sentiment dropped to 96.5, EU down to 95.1

Eurozone Economic Sentiment Indicator fell from 99.0 to 96.5 in May. Employment Expectation Indicator dropped from 107.5 to 104.7. Economic Uncertainty Indicator dropped from 22.2 to 21.8.

Eurozone Industry confidence dropped from -2.8 to -5.2. Services confidence dropped from 9.9 to 7.0. Consumer confidence dropped from -17.5 to -17.4. Retail trade confidence dropped from -0.9 to -5.3. Construction confidence dropped from 0.9 to 0.2.

EU ESI dropped from 97.1 to 95.1. EEI dropped from 106.2 to 104.0. EUI dropped from 21.8 to 21.3. Amongst the largest EU economies, the ESI deteriorated in Spain (-3.0), Germany (-2.9), Italy (-2.3) and the Netherlands (-1.5), whereas it improved in Poland (+1.9) and France (+1.5).

Swiss economic outlook worsens as KOF economic barometer plunges

May has brought a significant dip in Swiss KOF Economic Barometer, which fell sharply from 96.1 to 90.2, a figure notably below the anticipated 95.3. This reading, barely above the cyclic trough of 89.3 recorded last November, indicates a continued deteriorating outlook for the Swiss economy for mid-2023.

In a statement, KOF noted, “This is the second time in a row that the barometer has fallen sharply. The outlook for the Swiss economy for the middle of 2023 is thus deteriorating further and remains at a below-average level.”

The sharp decline of the barometer, an important indicator of Switzerland’s economic health, is largely attributed to the manufacturing sector and financial and insurance services. Other economic sectors and foreign demand also contributed negative signals.

In contrast, “indicators covering private consumption are slightly positive,” providing a slight glimmer of optimism amid a broadly dimming economic forecast.

BoJ Ueda: Will patiently continue monetary easing

In today’s parliamentary address, BoJ Kazuo Ueda laid out the central bank’s approach to an evolving inflation scenario in Japan. Governor Ueda announced, “We expect inflation to quite clearly slow below 2%” as we move further into the current fiscal year.

Despite this imminent deceleration, BoJ is forecasting a subsequent rebound, albeit with a degree of caution. Ueda added, “Inflation is likely to rebound thereafter … though there is high uncertainty” about the future direction of inflation rates.

In response to these trends, BoJ plans to remain patient and maintain its current approach to monetary policy. Ueda affirmed the central bank’s commitment to its strategy, stating, “(We) will patiently continue monetary easing as there’s still distance to achievement of sustainable and stable 2% price hikes together with continued rises in wages.”

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2336; (P) 1.2354; (R1) 1.2373; More…

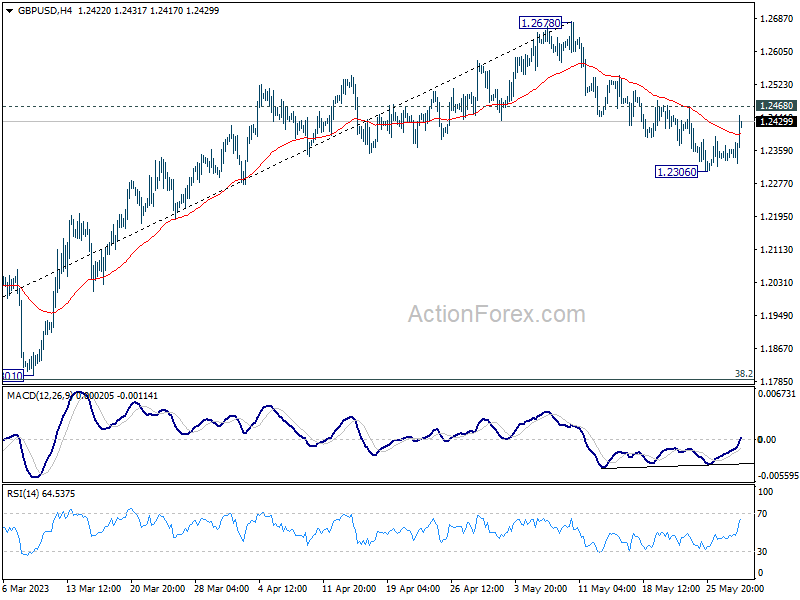

GBP/USD’s recovery from 1.2306 extends higher today but stays below 1.2468 minor resistance. Intraday bias remains neutral first and further decline is in favor. Break of 1.2306 will resume the fall from 1.2678, as correcting whole up trend from 1.0351, to 1.1801 cluster support (38.2% retracement of 1.0351 to 1.2678 at 1.1789). On the upside, however, firm break of 1.2468 will turn bias back to the upside for stronger rebound.

{kind=link}

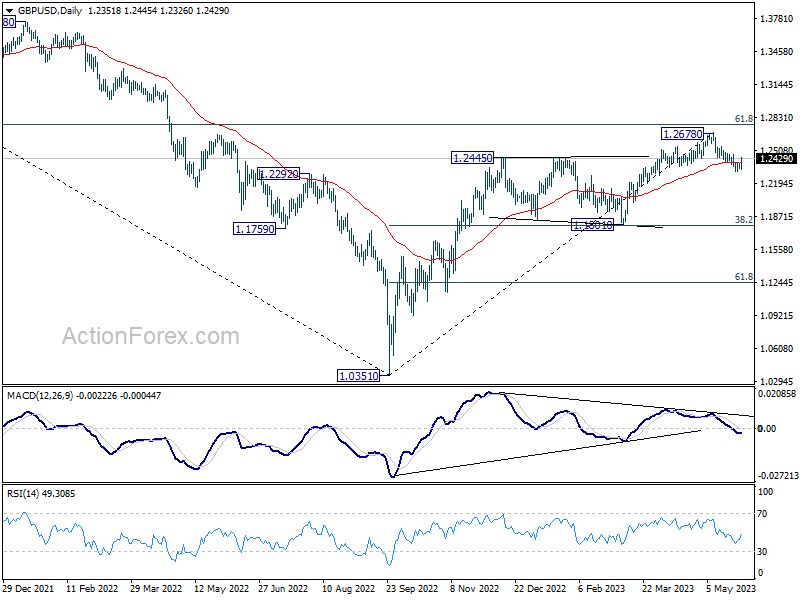

In the bigger picture, as long as 1.1801 support holds, rise from 1.0351 medium term bottom (2022 low) is expected to extend further. Sustained break of 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759 will add to the case of long term bullish trend reversal. However, firm break of 1.1801 will indicate rejection by 1.2759, and bring deeper decline, even as a correction.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Apr | -2.60% | 7.00% | 6.60% | |

| 23:30 | JPY | Unemployment Rate Apr | 2.60% | 2.70% | 2.80% | |

| 01:30 | AUD | Building Permits M/M Apr | -8.10% | 2.30% | -0.10% | -1.00% |

| 07:00 | CHF | KOF Leading Indicator May | 90.2 | 95.3 | 96.4 | 96.1 |

| 07:00 | CHF | GDP Q/Q Q1 | 0.30% | 0.10% | 0.00% | |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Apr | 1.90% | 2.10% | 2.50% | |

| 09:00 | EUR | Eurozone Economic Sentiment May | 96.5 | 99 | 99.3 | 99 |

| 09:00 | EUR | Eurozone Industrial Confidence May | -5.2 | -4 | -2.6 | -2.8 |

| 09:00 | EUR | Eurozone Services Sentiment May | 7 | 10 | 10.5 | 9.9 |

| 09:00 | EUR | Eurozone Consumer Confidence May F | -17.4 | -17.4 | -17.4 | |

| 12:30 | CAD | Current Account (CAD) Q1 | -6.2B | -9.9B | -10.6B | -8.1B |

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Mar | -1.15% | -1.70% | 0.40% | |

| 13:00 | USD | Housing Price Index M/M Mar | 0.60% | 0.30% | 0.50% | 0.70% |

| 14:00 | USD | Consumer Confidence May | 99.1 | 101.3 |