Dollar has maintained its position as the strongest performer for the week, despite the noticeable waning of its upside momentum over the past two days. Today, markets anticipates the release of several US economic indicators, including PCE inflation and durable goods orders. However, the primary driver is likely to be any updates on the debt ceiling negotiations.

Reports suggest that a deal is in the works that would increase the debt limit to USD 31.4T for a two-year period. However, both the deal itself and the market’s response to it are fraught with considerable uncertainty.

In other currency market developments, Sterling is attempting a bounce after encouraging retail sales data, but thus far, buyers seem to be demonstrating a lack of conviction. Meanwhile, the sell-off in Australian and New Zealand Dollars appears to be slowing down.

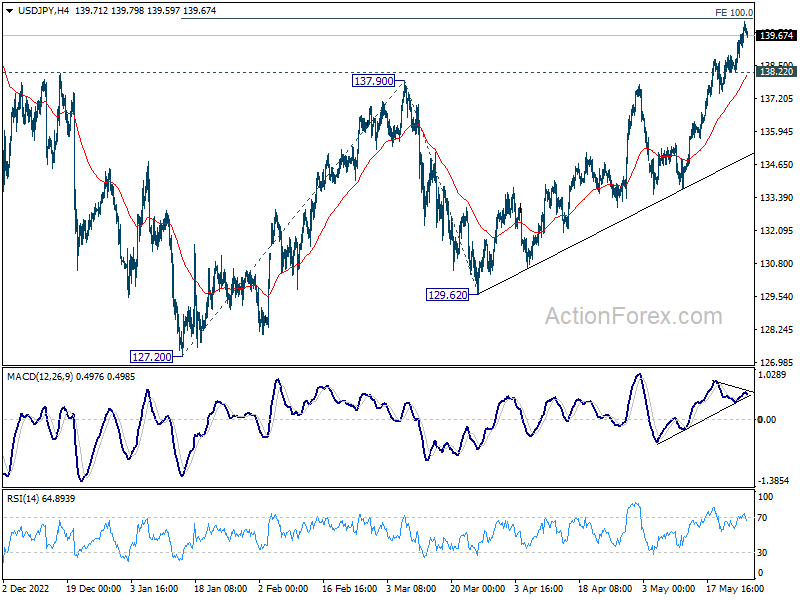

Technically, USD/JPY is worth a watch for the rest of the week and the early part of next. It’s been losing some upside momentum as seen in 4H MACD. Also, it has almost met the target of 100% projection of 127.20 to 137.90 from 129.62 at 140.32. Rejection by 140.32, followed by break of 138.22 support could mark the completion of the three-wave corrective rise from 127.20. If realized, the could set a bearish tone for other Yen crosses for the near term.

{kind=link}

UK retail sales volume up 0.5% mom in Apr, value up 1.1% mom

UK retail sales volumes rose 0.5% mom in April, well above expectation of 0.0% mom. Excluding automotive fuel, sales volume rose 0.8% mom. Sales value rose 1.1% mom in the month, with ex-automotive fuel sales value up 1.7% mom.

In the three months to April, sales volumes rose 0.8% 3mo3m, the highest rates since August 2021, which was at 1.3% 3mo3m.

RBNZ Silk warns against premature rate cut expectations

RBNZ Assistant Governor Karen Silk advised caution against pricing in rate cuts too prematurely. In her comments, Silk stressed that RBNZ has reached a juncture where it can “take a pause and watch how this evolves,” ensuring that “you don’t overdo things.”

However, Silk emphasized that it’s core inflation that the central bank is focused on bringing down, and this will require maintaining the current rate levels for an extended period. “We’ve said we need to hold for an extended period of time to ensure core inflation comes down; it’s core inflation that we need to get down,” she stated.

She explained the bank’s holistic approach to assessing economic conditions, saying, “We look at economic data, but we also look at transmission,” Silk explained. “If at a wholesale level and most importantly at a retail level we start to see those things come off faster, then that’s one of the things we take into account when we think about where we set the OCR.”

In terms of the inflationary impact of Cyclone Gabrielle, Silk indicated that its effect has been less severe than initially anticipated. RBNZ had initially projected the storm would add 0.3% to inflation in both the first and second quarters. Still, it has since revised this down to just 0.1%, citing that while the storm led to increased food costs, it didn’t inflate the prices of other goods such as used cars.

Australia retail sales flat in Apr, cost-of-living pressures and rising interest rates

Australia retail sales turnover was flat at 0% mom in April, and up 4.2% yoy.

“Retail turnover has plateaued over the last six months as consumers spent less on discretionary goods in response to cost-of-living pressures and rising interest rates. Spending was again soft in April but was boosted by increased spending on winter clothing in response to cooler and wetter than average weather across the country,” Ben Dorber, ABS head of retail statistics said.

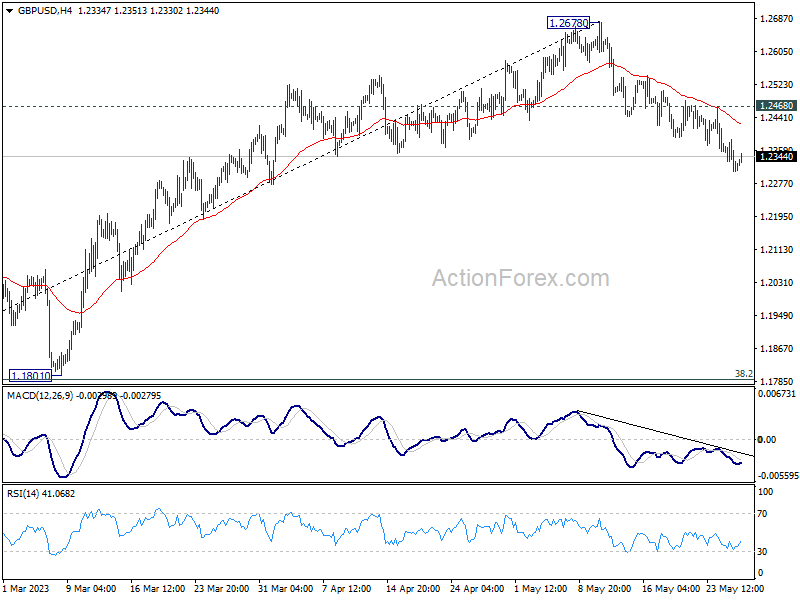

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2291; (P) 1.2339; (R1) 1.2370; More…

GBP/USD recovers mildly today but there is no clear sign of bottoming yet. Intraday bias stays on the downside for the moment. Current decline is seen as correcting whole up trend from 1.0351. Deeper fall should be seen to 1.1801 cluster support (38.2% retracement of 1.0351 to 1.2678 at 1.1789). On the upside, above 1.2468 minor resistance will turn intraday bias neutral first.

{kind=link}

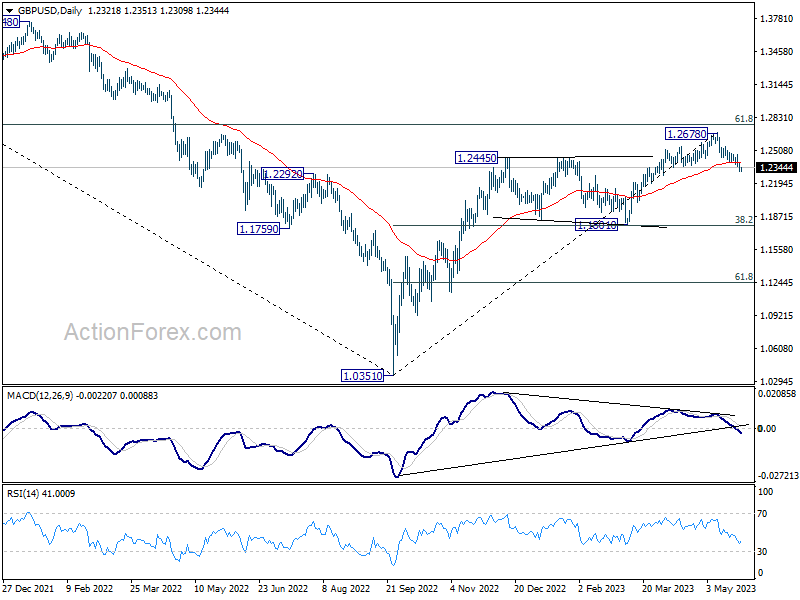

In the bigger picture, as long as 1.1801 support holds, rise from 1.0351 medium term bottom (2022 low) is expected to extend further. Sustained break of 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759 will add to the case of long term bullish trend reversal. However, firm break of 1.1801 will indicate rejection by 1.2759, and bring deeper decline, even as a correction.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y May | 3.20% | 3.40% | 3.50% | |

| 23:50 | JPY | Corporate Service Price Index Y/Y Apr | 1.60% | 1.40% | 1.60% | 1.70% |

| 01:30 | AUD | Retail Sales M/M Apr | 0.00% | 0.30% | 0.40% | |

| 06:00 | GBP | Retail Sales M/M Apr | 0.50% | 0.00% | -0.90% | |

| 12:30 | USD | Durable Goods Orders Apr | -0.90% | 3.20% | ||

| 12:30 | USD | Durable Goods Orders ex Transportation Apr | 0.00% | 0.20% | ||

| 12:30 | USD | Personal Income M/M Apr | 0.40% | 0.30% | ||

| 12:30 | USD | Personal Spending M/M Apr | 0.40% | 0.00% | ||

| 12:30 | USD | PCE Price Index M/M Apr | 0.40% | 0.10% | ||

| 12:30 | USD | PCE Price Index Y/Y Apr | 3.90% | 4.20% | ||

| 12:30 | USD | Core PCE Price Index M/M Apr | 0.40% | 0.30% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Apr | 5.00% | 4.60% | ||

| 12:30 | USD | Goods Trade Balance (USD) Apr P | -85.6B | -84.6B | ||

| 12:30 | USD | Wholesale Inventories Apr P | 0.10% | 0.00% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index May F | 58.2 | 57.7 |