While Dollar engaged in retreat for most of the day, some buying appears to emerge again in early US session. A surprising rise in both headline and core PCE inflation is considered to be a key factor driving this resurgence. While it’s unsure whether that could result in sustainable rally, the sentiment should stabilize the greenback at least.

Meanwhile, selloff in Yen is taking off again, following rally in US and European benchmark yields, with US 10-year yield breaking 3.8% level in pre-market. The current tone in the markets will likely keep the greenback as the best performer for the week. New Zealand and Australian Dollars will end as the worst, with Yen a distant third. Euro, Sterling, and Swiss Franc are basically still bounded in range against each other.

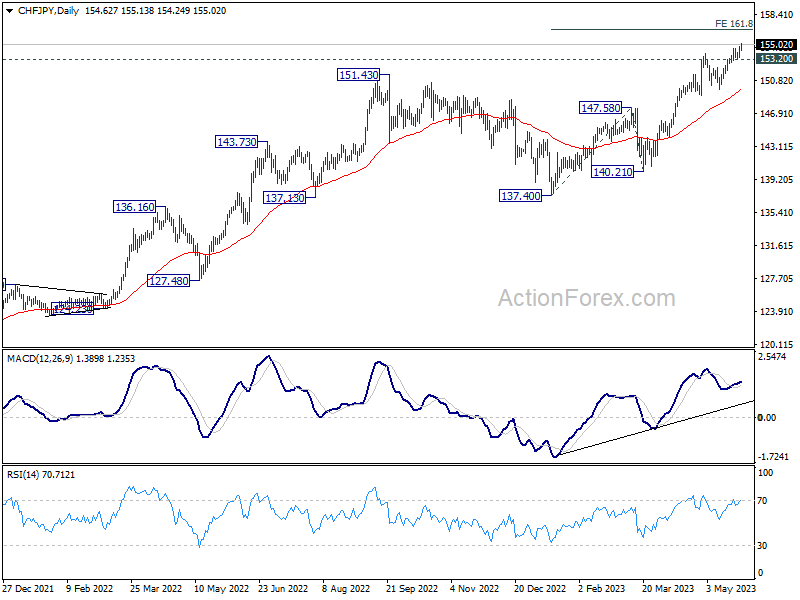

Technically, CHF/JPY’s rally resumes today and hits as high as 155.13 so far. Near term outlook will stay bullish as long as 153.20 support holds. Next target is 100% projection of 137.40 to 147.58 from 140.21 at 156.68. GBP/JPY is also extending recent up trend and breaks above 173 handle. It’s a question now whether the development is enough to take EUR/JPY through 151.60 resistance.

{kind=link}

In Europe, at the time of writing, FTSE is up 0.24%. DAX is up 0.33%. CAC is up 0.44%. Germany 10-year yield is up 0.005 at 2.529. Earlier in Asia, Nikkei rose 0.37%. Hong Kong HSI dropped -1.93%. China Shanghai SSE rose 0.35%. Singapore Strait Times dropped -0.01%. Japan 10-year JGB yield dropped -0.0078 to 0.422.

US PCE rose to 4.4% yoy, core PCE up to 4.7% yoy

US personal income rose 0.4% mom or USD 80.1B in April, matched expectations. Personal spending rose 0.8% mom or USD 151.7B, above expectation of 0.4% mom.

For the month, PCE price index rose 0.4% mom. Core PCE price index (excluding food and energy) rose 0.4% mom. Goods prices increased 0.3% mom while services prices increased 0.4% mom. Food prices decreased less than -0.1% mom. Energy prices rose 0.7% mom.

From the same month one year ago, headline PCE price index rose from 4.2% yoy to 4.4% yoy, above expectation of 3.9% yoy. Core PCE price index also ticked up from 4.6% yoy to 4.7% yoy, above expectation of 4.6% yoy. Prices for goods were up 2.1% yoy and prices for services were up 5.5% yoy. Foods prices increased 6.9% yoy. Energy prices decreased -6.3% yoy.

Also released, durable goods orders rose 1.1% mom in April versus expectation of -0.9% mom. Ex-transport orders dropped -0.2% mom versus expectation of 0.0%. Goods trade deficit widened to USD -96.8B, versus expectation of USD -85.6B.

ECB Lane: Reversal of energy prices will feed into lower core

ECB Chief Economist Philip Lane has asserted that falling energy prices could lead to lower core inflation due to reduced living costs and, consequently, restrained wage increases. However, he stressed the timeline and extent of this effect remain uncertain.

Speaking at a conference in Dubrovnik, Lane said, “I don’t think it’s symmetric… but when energy prices fall, core inflation does follow, because there is less pressure from an energy cost, there’s less pressure on the cost of living, therefore on nominal wage increases

“So, we do think this spectacular reversal of energy prices will feed into lower core, but the timeline for that and the scale of it is uncertain,” he added.

Lane further observed that wage growth is generally progressing at a moderate pace, with many people still bound to older contracts. “The latest deals are coming in at above 5%, but (this is in the) ballpark of what we expect,” he noted.

Despite this, he expects nominal wage growth to peak this year and suggested it would take real wages until 2025 to recover back to their 2019 level.

UK retail sales volume up 0.5% mom in Apr, value up 1.1% mom

UK retail sales volumes rose 0.5% mom in April, well above expectation of 0.0% mom. Excluding automotive fuel, sales volume rose 0.8% mom. Sales value rose 1.1% mom in the month, with ex-automotive fuel sales value up 1.7% mom.

In the three months to April, sales volumes rose 0.8% 3mo3m, the highest rates since August 2021, which was at 1.3% 3mo3m.

RBNZ Silk warns against premature rate cut expectations

RBNZ Assistant Governor Karen Silk advised caution against pricing in rate cuts too prematurely. In her comments, Silk stressed that RBNZ has reached a juncture where it can “take a pause and watch how this evolves,” ensuring that “you don’t overdo things.”

However, Silk emphasized that it’s core inflation that the central bank is focused on bringing down, and this will require maintaining the current rate levels for an extended period. “We’ve said we need to hold for an extended period of time to ensure core inflation comes down; it’s core inflation that we need to get down,” she stated.

She explained the bank’s holistic approach to assessing economic conditions, saying, “We look at economic data, but we also look at transmission,” Silk explained. “If at a wholesale level and most importantly at a retail level we start to see those things come off faster, then that’s one of the things we take into account when we think about where we set the OCR.”

In terms of the inflationary impact of Cyclone Gabrielle, Silk indicated that its effect has been less severe than initially anticipated. RBNZ had initially projected the storm would add 0.3% to inflation in both the first and second quarters. Still, it has since revised this down to just 0.1%, citing that while the storm led to increased food costs, it didn’t inflate the prices of other goods such as used cars.

Australia retail sales flat in Apr, cost-of-living pressures and rising interest rates

Australia retail sales turnover was flat at 0% mom in April, and up 4.2% yoy.

“Retail turnover has plateaued over the last six months as consumers spent less on discretionary goods in response to cost-of-living pressures and rising interest rates. Spending was again soft in April but was boosted by increased spending on winter clothing in response to cooler and wetter than average weather across the country,” Ben Dorber, ABS head of retail statistics said.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0703; (P) 1.0730; (R1) 1.0752; More…

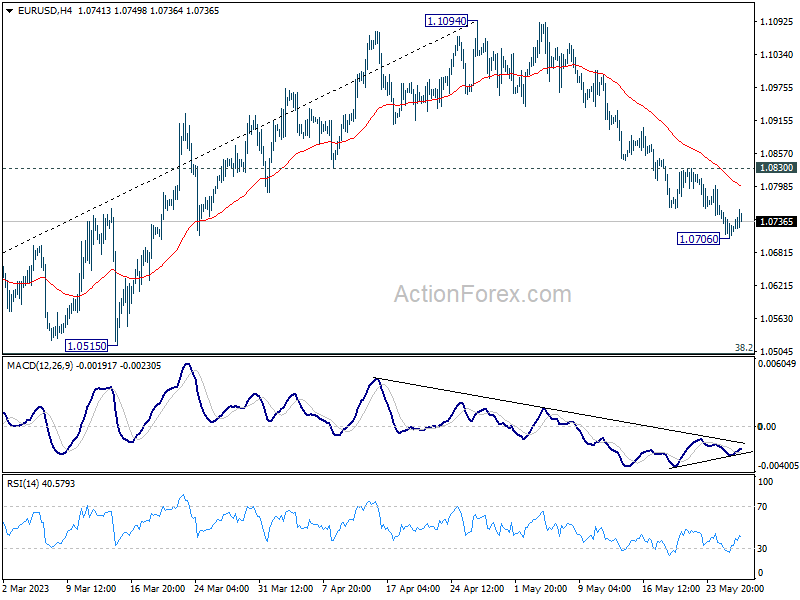

Intraday bias in EUR/USD is turned neutral first with current recovery, and some consolidations could be seen. But further decline is expected as long as 1.0830 resistance holds. Current fall from 1.1094 is seen as correcting whole up trend from 0.9534. Below 1.0706 will target 1.0515 cluster support, 38.2% retracement of 0.9534 to 1.1094 at 1.0498. On the upside, however, above 1.0830 minor resistance will turn bias to the upside for stronger rebound.

{kind=link}

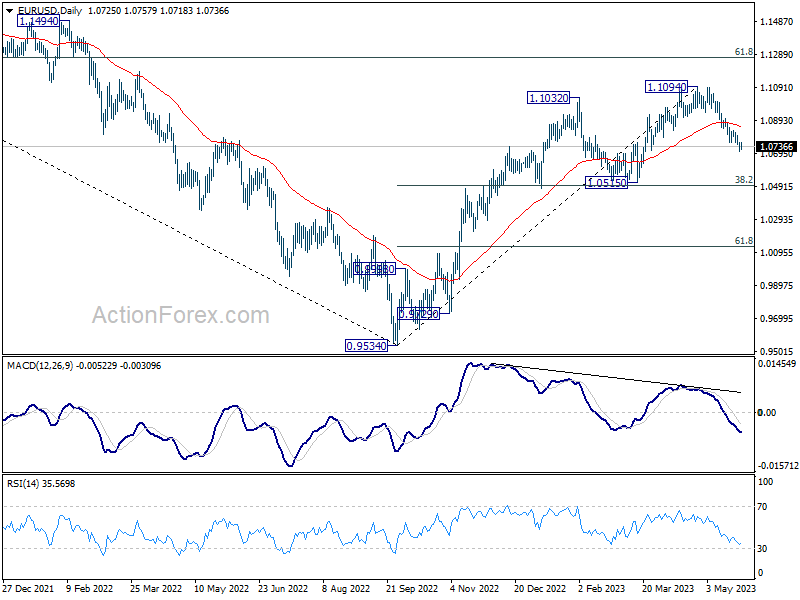

In the bigger picture, as long as 1.0515 support holds, rise from 0.9534 (2022 low) would still extend higher. Sustained break of 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y May | 3.20% | 3.40% | 3.50% | |

| 23:50 | JPY | Corporate Service Price Index Y/Y Apr | 1.60% | 1.40% | 1.60% | 1.70% |

| 01:30 | AUD | Retail Sales M/M Apr | 0.00% | 0.30% | 0.40% | |

| 06:00 | GBP | Retail Sales M/M Apr | 0.50% | 0.00% | -0.90% | |

| 12:30 | USD | Durable Goods Orders Apr | 1.10% | -0.90% | 3.20% | 3.30% |

| 12:30 | USD | Durable Goods Orders ex Transportation Apr | -0.20% | 0.00% | 0.20% | |

| 12:30 | USD | Personal Income M/M Apr | 0.40% | 0.40% | 0.30% | |

| 12:30 | USD | Personal Spending M/M Apr | 0.80% | 0.40% | 0.00% | 0.10% |

| 12:30 | USD | PCE Price Index M/M Apr | 0.40% | 0.40% | 0.10% | |

| 12:30 | USD | PCE Price Index Y/Y Apr | 4.40% | 3.90% | 4.20% | |

| 12:30 | USD | Core PCE Price Index M/M Apr | 0.40% | 0.40% | 0.30% | |

| 12:30 | USD | Core PCE Price Index Y/Y Apr | 4.70% | 4.60% | 4.60% | |

| 12:30 | USD | Goods Trade Balance (USD) Apr P | -96.8B | -85.6B | -84.6B | -82.7B |

| 12:30 | USD | Wholesale Inventories Apr P | -0.20% | 0.10% | 0.00% | |

| 14:00 | USD | Michigan Consumer Sentiment Index May F | 58.2 | 57.7 |