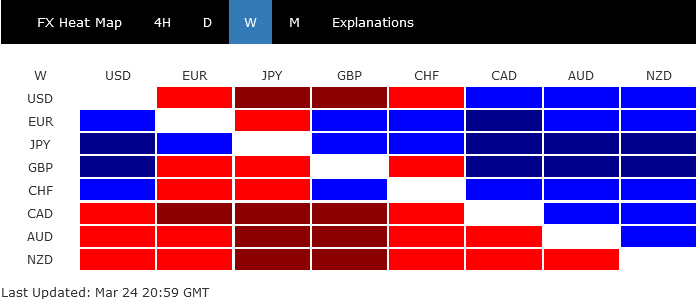

Last week’s financial landscape was far from clear-cut. While it wasn’t a definitive risk-on market, investors seemed reluctant to abandon US shares completely. The markets found themselves mired in confusion, struggling to make sense of the relentless barrage of headlines detailing bank crises that began with Silicon Valley Bank, then spread to First Republic, Credit Suisse, and eventually Deutsche Bank. Amid the banking turmoil, rate hikes by Fed, BoE, and SNB added another layer of complexity, prompting reinterpretations of rate outlooks and their influence on financial markets.

Despite the chaos, Yen emerged as the strongest performer for yet another week. Euro and Swiss Franc trailed behind, both making a notable recovery from the previous week’s losses. Were it not for Deutsche Bank’s woes, Euro might have claimed the top spot. Commodity currencies bore the brunt of the market turbulence, while Dollar and Sterling delivered mixed results.

As uncertainties continue to mount, including potentially more bank troubles, rate outlooks, and recession risks, the fluctuations between Dollar and European majors may persist until clarity is restored. For the time being, however, Yen appears to be in prime position to extend its gains against commodity currencies.

{kind=link}

Fed rate at 4.75%-5.00% already the peak?

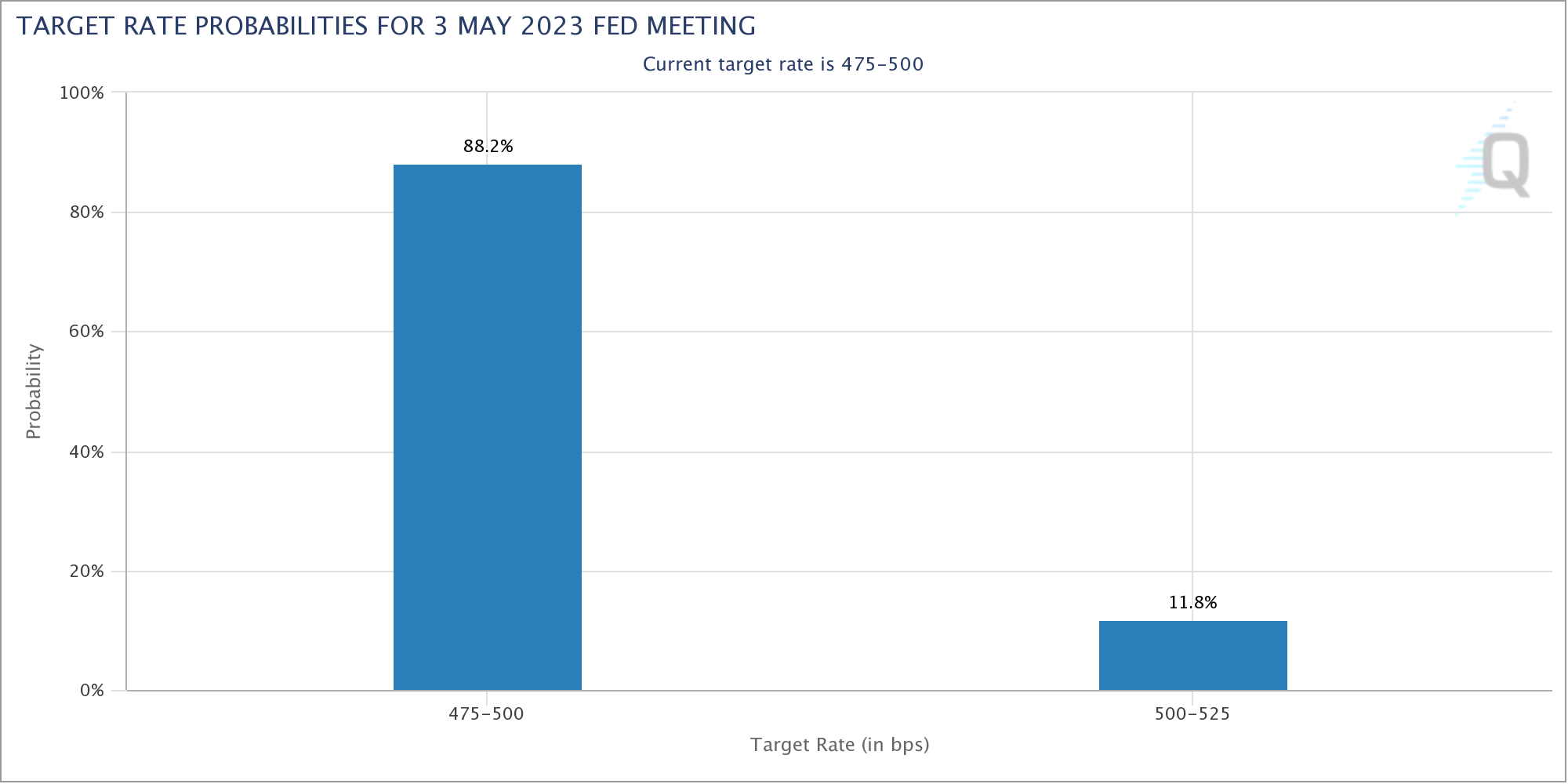

Last week, Fed raised interest rates by 25bp to 4.75-5.00% amidst flip-flopping speculations. Despite the less hawkish tone, the meeting wasn’t entirely dovish. Median projections still indicate an interest rate peak at 5.1% this year, with another 25bps hike possible. The median projection for 2024 interest rate increased from 4.1% to 4.3%, signaling a slower path of rate cuts. Chair Jerome Powell also indicated in the post-meeting press conference that a rate cut this year was “not our baseline expectation.”

However, as the banking crisis appeared to be dragging on, investors are clearly having different views to FOMC members. As of end of Friday, fed fund futures are pricing in 88.2% chance of Fed being on hold in May, with just 11.8% chance of a 25bps hike.

{kind=link}

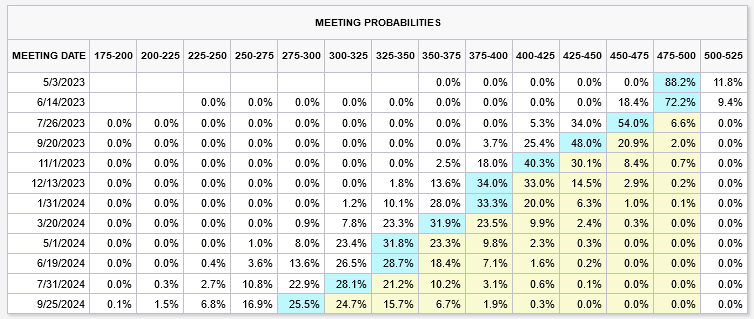

Indeed, the current 4.75-5.00% is seen as the peak already with over 90% chance of it staying there after June meeting. There’s now over 90% chance of starting a rate cut cycle in July, with near 50% chance of having interest rate back to 3.75-4.00%, a 100bps below the current level, by the end of the year.

{kind=link}

Happened last week too, BoE delivered a 25bps to 4.25% as widely expected, and then signalled that “if there were to be evidence of more persistent (inflation) pressures, then further tightening in monetary policy would be required.” Or in other words, if inflation pressure doesn’t persist, it’s also open to a pause. The outlook, however, was complicated by February CPI, which reaccelerated to 10.4% yoy. Baseline expectations are now for BoE to hike another 25bps in May then pause.

SNB hiked by 50bps to 1.50% as widely expected and said “”it cannot be ruled out that additional rises in the SNB policy rate will be necessary”. With assumption of 1.5% interest rate over the forecast horizon, inflation projections for both 2023 and 2024 were raised. Markets are expecting another 25bps hike in June to bring the tightening cycle to conclusion.

Minutes of RBA’s meeting this month indicated that members agreed to “reconsider the case for a pause at the following meeting, recognizing that pausing would allow additional time to reassess the outlook for the economy.” There case is there now for RBA to pause in April, before determining whether to hike again in May based on the new economic projections then.

US stocks resilient with NASDAQ leading

In the US stock markets, much resilience was shown despite all the headlines about banking turmoils. Sentiment seemed to be firmly supported by expectations of a lower terminal rate of Fed and an early start of rate cut cycle.

NASDAQ flared pretty well with break of 11827.91 resistance, even though it couldn’t close the week above there. The development is inline with the view that corrective pullback from 12269.55 has completed at 10987.80 already. Further rally is in favor as long as 55 day EMA (now at 11474.49) holds, for 12269.55 and above in the near term.

{kind=link}

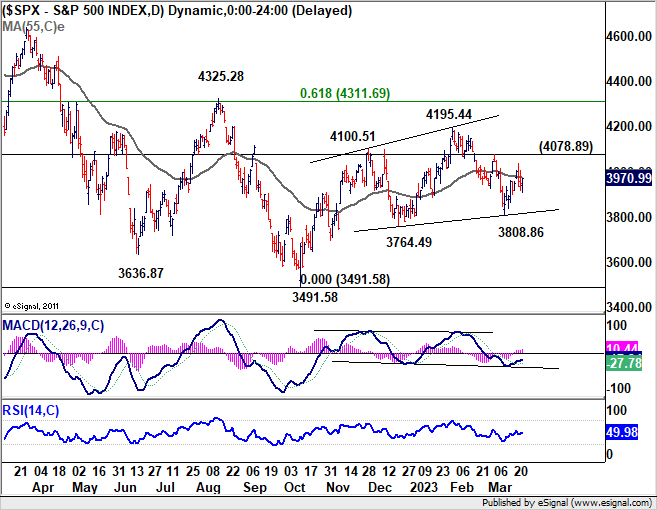

Underlying bullish momentum in US stocks would be further confirmed if S&P 500 could take out corresponding resistance level at 4078.89. That would indicate completion of the corrective pull back form 4195.44 at 3808.86. Rise from 3491.58 should then be ready to resume through 4195.44.

{kind=link}

10-year yield trying to draw support from 3.21/22

US 10-year yield dived to as low as 3.295 on Friday on developments around Deutsche Bank. But it recovered notably to close at 3.380, showing that sentiments were still relatively calm. Technically, TNX is extending the corrective pattern from 4.333, with 4.091 as the third leg.

While another fall cannot be ruled out, we’d still expect strong support from 61.8% retracement level of 2.525 to 4.333 at 3.215, which is in close proximity to 55 week EMA (now at 3.220). This zone should provide enough support to complete the corrective pattern to bring rebound. However, sustained break of 3.2 handle would signal even larger troubles on the horizon.

{kind=link}

{kind=link}

Dollar index recovered ahead of 101.91 low, but stays bearish

Dollar index’s decline from 105.88 extended further to low as 101.91 but recovered to close at 103.11. Medium term outlook remains bearish with 38.2% retracement of 114.77 to 100.82 at 106.14 intact. That is, eventual break of 100.82 support is expected.

However, the question is whether price actions from 100.82 would develop into a three wave corrective pattern. Break of 103.44 support turned resistance would suggest that it is. Stronger rise would then be seen back to 105.88 or further to 106.14 in the near term, before breaking through 100.82 in the medium term.

{kind=link}

{kind=link}

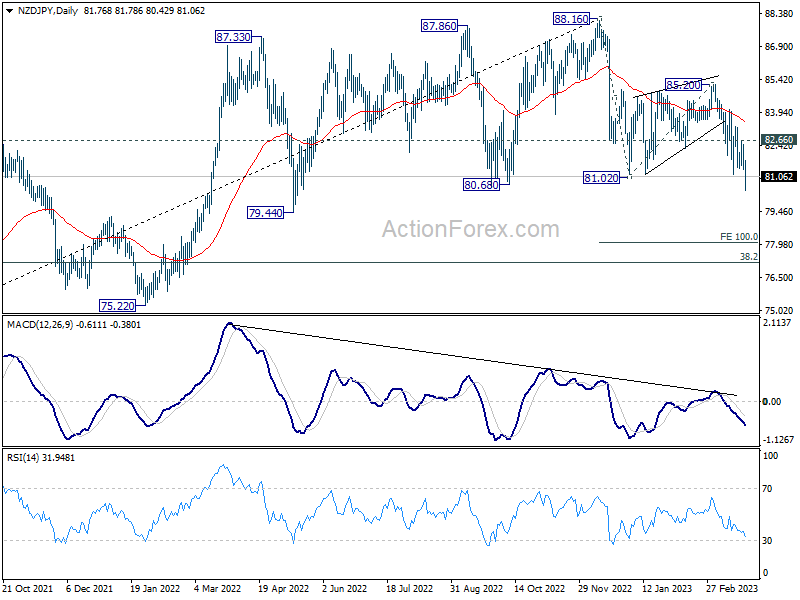

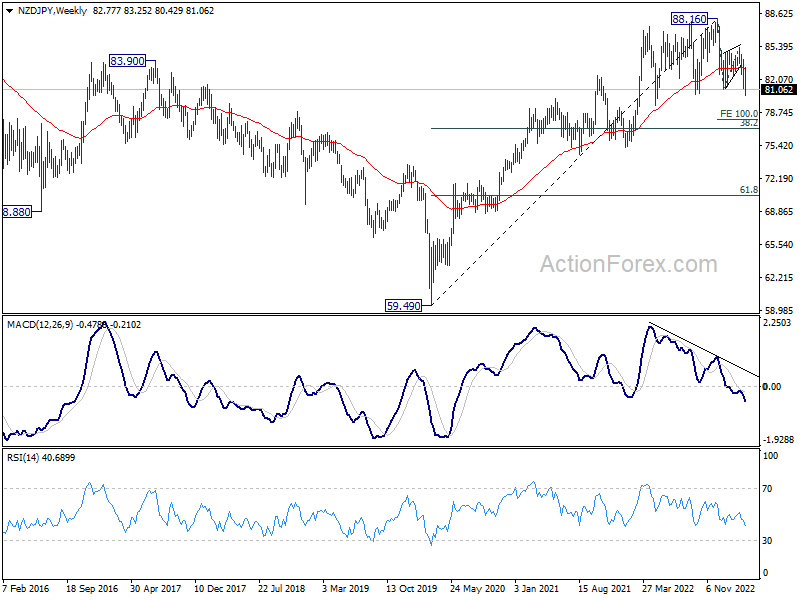

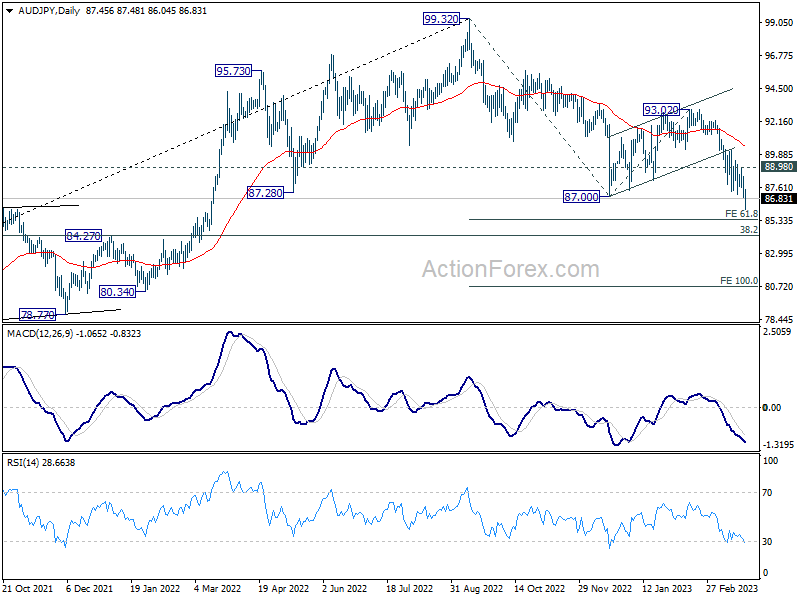

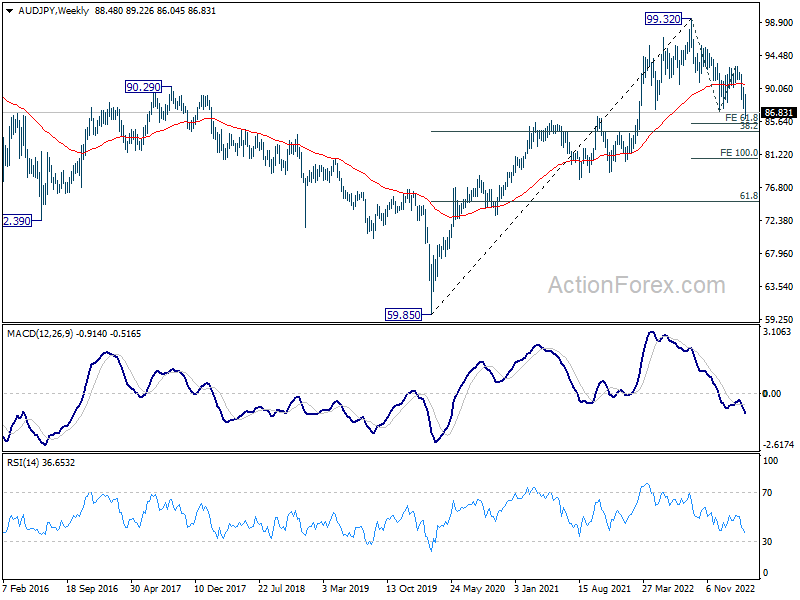

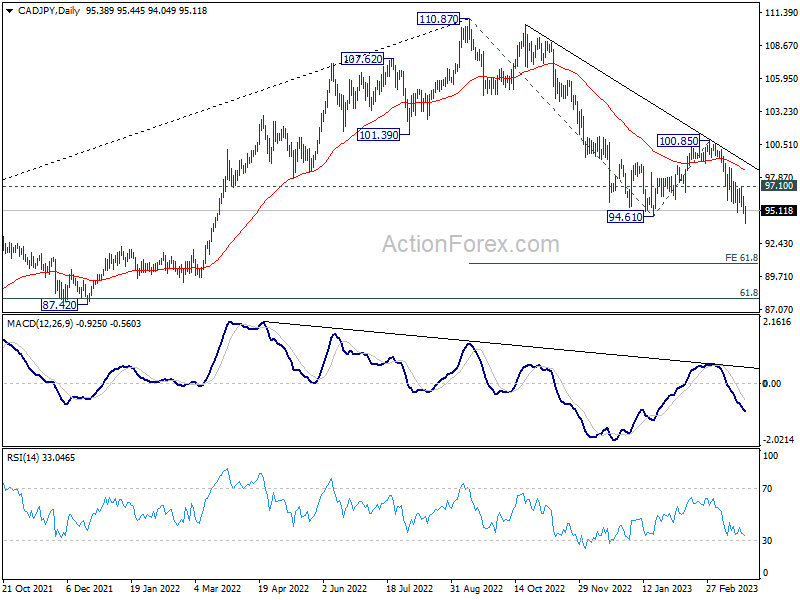

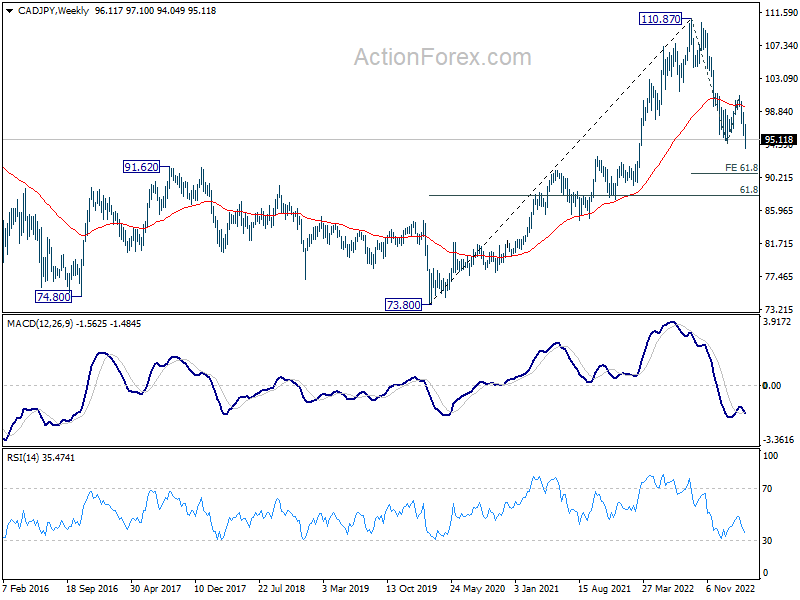

NZD/JPY, AUD/JPY an CAD/JPY downside breakout as medium term decline resumed

Yen broke out to the upside against all three commodity currencies last week. NZD/JPY was among the better performer recently. But even so, it should now be in a medium term decline, as a correction to the up trend from 59.49 (2020 low). Near term outlook will stay bearish as long as 82.66 resistance holds. Fall from 88.16 medium term top should target 100% projection of 88.16 to 81.02 from 85.20 at 78.06. Strong support could be seen around 38.2% retracement of 59.49 to 88.16 at 77.20 to conclude the correction to bring reversal.

{kind=link}

{kind=link}

AUD/JPY is also in correction to the up trend from 59.85 (2020 low). Near term outlook will stay bearish as long as 88.98 resistance holds. Next target is 61.8% projection of 99.32 to 87.00 from 93.02 at 85.40. There might be some support from 38.2% retracement of 59.85 to 99.32 at 84.24 to complete the correction. If not, AUD/JPY’s decline from 99.32 would extend further to 100% projection at 80.70 before conclusion.

{kind=link}

{kind=link}

Similarly, CAD/JPY is also now in correction to the up trend from 73.80 (2020 low), steeper than NZD/JPY and AUD/JPY. Near term outlook will stay bearish as long as 97.10 resistance holds. Next target is 61.8% projection of 110.87 to 94.61 from 100.85 at 90.80. While CAD/JPY might fall through this projection level, strong support should be seen from 61.8% retracement of 73.80 to 110.87 at 87.96 to complete the correction.

{kind=link}

{kind=link}

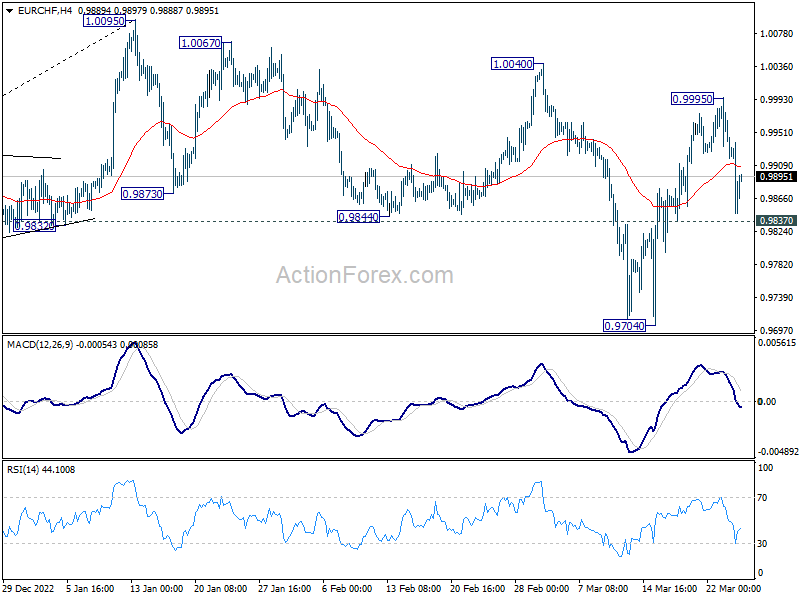

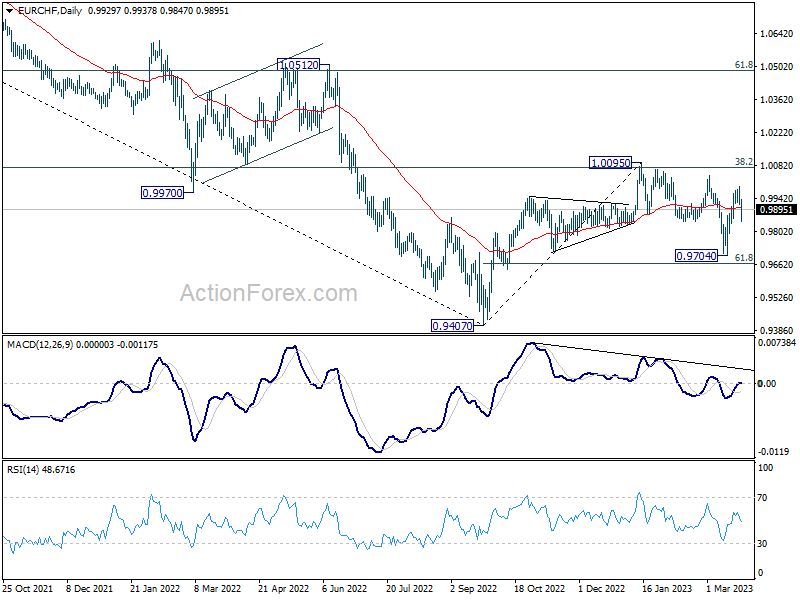

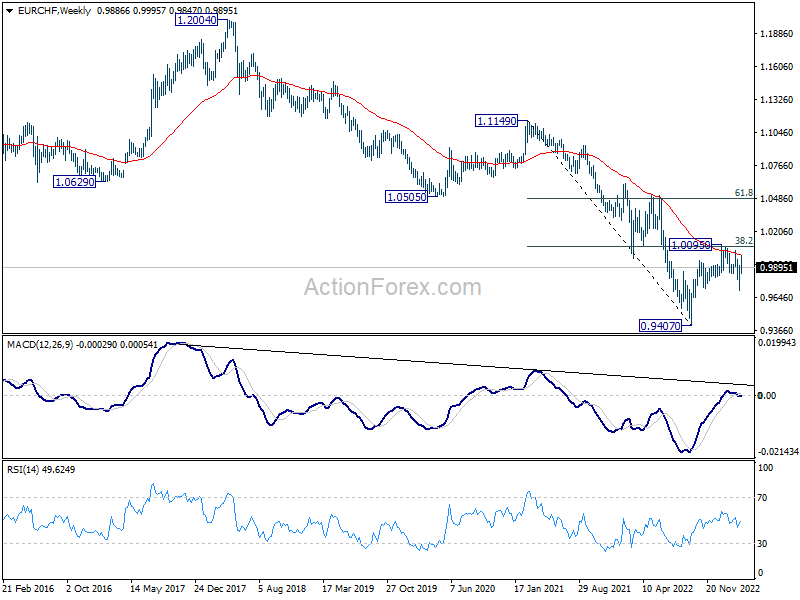

EUR/CHF Weekly Outlook

EUR/CHF’s rise from 0.9704 extended higher to 0.9995 last week but retreated sharply since then. Initial bias remains neutral this week first. Another rise will remain mildly in favor as long as 0.9837 minor support holds. Break of 0.9995 will affirm the case that correction from 1.0095 has completed at 0.9704. Further rally should be seen through 1.0040 to retest 1.0095 high. However, firm break of 0.9837 will dampen this bullish view and turn bias back to the downside for 0.9704 support instead.

{kind=link}

In the bigger picture, prior rejection by 55 week EMA (now at 1.1002) and 38.2% retracement of 1.1149 to 0.9407 at 1.0072 suggests that medium term outlook is staying bearish. That is, down trend from 1.2004 is not completed yet and is in favor to resume through 0.9407 at a later stage. However, decisive break of 1.0095 resistance will raise the chance of bullish trend reversal. Rise from 0.9407 should then target 1.0505 cluster resistance (2020 low at 1.0505, 61.8% retracement of 1.1149 to 0.9407 at 1.1484).

{kind=link}

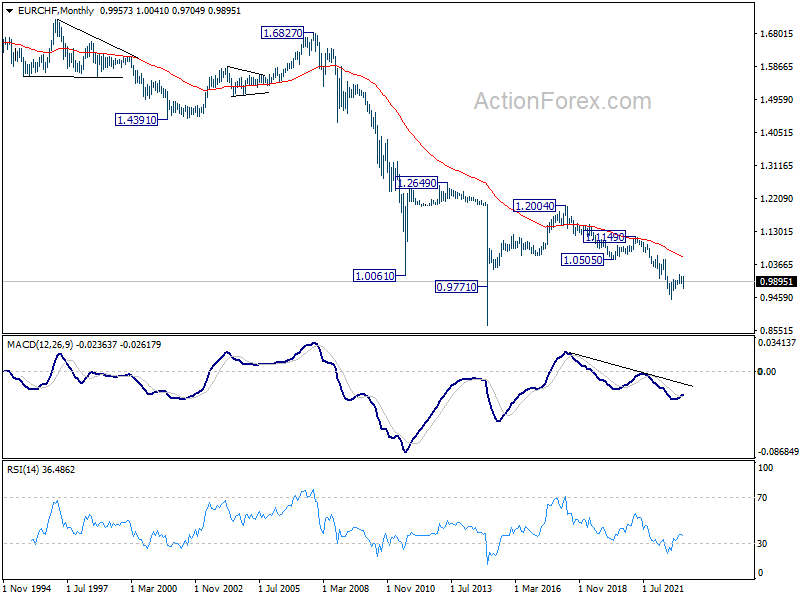

In the long term picture, it’s still way too early too call for bullish trend reversal with upside capped well below 55 month EMA and 1.0505 support turned resistance (2020 low). The multi-decade down trend could still continue.

{kind=link}

{kind=link}