Yen is drawing some attention in today’s Asian trading session, supported by declining benchmark US and European treasury yields and robust core-core inflation in Japan. Risk-sensitive currencies, such as Sterling and commodity currencies, are under pressure as major Asian indexes trade lower. Dollar is recovering against the Euro but still lags far behind for the week. Market focus will shift to Eurozone and UK PMI data, Canadian retail sales, and US durable goods orders later today.

For the week, Euro is the standout performer thus far, as ECB’s tightening could extend longer, while Fed and BoE appear closer to pausing based on this week’s meetings. Yen, currently in second place, could potentially overtake Euro if bond rallies continue. Swiss Franc is the third strongest currency, while Australian and New Zealand dollars are the weakest performers this week, trailed by Dollar and Canadian.

Technically, Gold is back pressing 2000 handle after defending 1936.15 support earlier in the week. The real test lies in 61.8% projection of 1614.60 to 1959.47 from 1804.48 at 2017.60. Sustained break there could solidify upside momentum to push Gold through historical high at 2074.84. If realizes, the development could signal more downside in Dollar, in particular against Yen.

{kind=link}

In Japan, Nikkei closed down -0.20%. Hong Kong HSI is down -0.77%. China Shanghai SSE is down -0.73%. Singapore Strait Times is down -0.13%. Japan 10-year JGB yield is down -0.016 at 0.290. Overnight, DOW rose 0.23%. S&P 500 rose 0.30%. NASDAQ rose 1.01%. 10-year yield dropped -0.094 to 3.406.

Japan CPI core down sharply to 3.1%, but core-core rose to 40-yr high

Japan’s headline CPI in February experienced a sharp slowdown from 4.3% yoy to 3.3% yoy, falling below the expected 4.1% yoy. CPI core (all items excluding food) dropped from 4.2% yoy to 3.1% yoy, meeting expectations. Meanwhile, CPI core-core (all items excluding food and energy) rose from 3.2% yoy to 3.5% yoy, surpassing the anticipated 3.4% yoy.

Despite the steep decline in CPI core from a 41-year high of 4.2% to 3.1%, the figure remains well above the Bank of Japan’s (BoJ) 2% target. The core-core reading, closely monitored by the BoJ as an indicator of domestic demand, reached its highest rate since January 1982.

The data suggests that incoming BoJ Governor Kazuo Ueda may need to address a shift from cost-push inflation to demand-driven inflation, which could prove more sustainable.

Japan PMIs: Growth continues with strong services but struggling manufacturing

Japan PMI Manufacturing rose from 47.7 to 48.6 in March, slightly above expectation of 48.2. PMI Manufacturing Output rose from 45.3 to 47.4. PMI Services ticked up from 54.0 to 54.2, the best reading since October 2013. MI Composite improved from 51.1 to 51.9.

Japanese private sector firms experienced growth for the third consecutive month, with the services sector witnessing a notable improvement. Demand conditions strengthened, as government support and the lifting of COVID-19 restrictions in mainland China led to increased activity and new orders.

However, the manufacturing sector continued to face challenges, with output and new orders still contracting, albeit at a slower rate than February. Manufacturers reported ongoing supply chain normalization, as supplier delivery times lengthened at the slowest pace since October 2020.

Australia PMI composite dropped to 48.1, renewed contraction

Australia PMI Manufacturing dropped from 50.5 to 48.7 in March, a 34-month low. PMI Services dropped from 50.7 to 48.2, a 3-month low. PMI Composite dropped from 50.6 to 48.1, a 3-month low. All readings indicated renewed contraction in the private sector following improvements in February.

Looking at some details, the results indicate a continued economic slowdown, with composite output and new orders indexes at their lowest since the 2021 Delta lockdowns. Despite easing labor demand, employment indexes suggest businesses are still looking to expand their workforce in 2023. Price indicators have eased but remain elevated, with Australian inflation peaking in late 2022. Service industry input prices are still high, suggesting potential inflationary pressures in 2023 due to labor costs and energy prices.

As RBA prepares for its April meeting, it faces a tough decision on whether to pause its tightening cycle amid global financial uncertainty, strong employment numbers, and concerns about inflation levels. Some argue that the RBA should raise the cash rate closer to 4% before pausing to observe the economy’s performance over the next few months.

Warren Hogan, Chief Economic Advisor at Judo Bank noted: “There is no point pausing for a month before hiking again. The RBA Board need to get the cash rate to a level that they think will buy them the time to observe how the economy unfolds for at least three months, if not longer.”

Looking ahead

UK retail sales, PMIs and Eurozone PMIs are the main focus in European session. Later in the day, Canada will release retail sales. US will publish durable goods orders and PMIs.

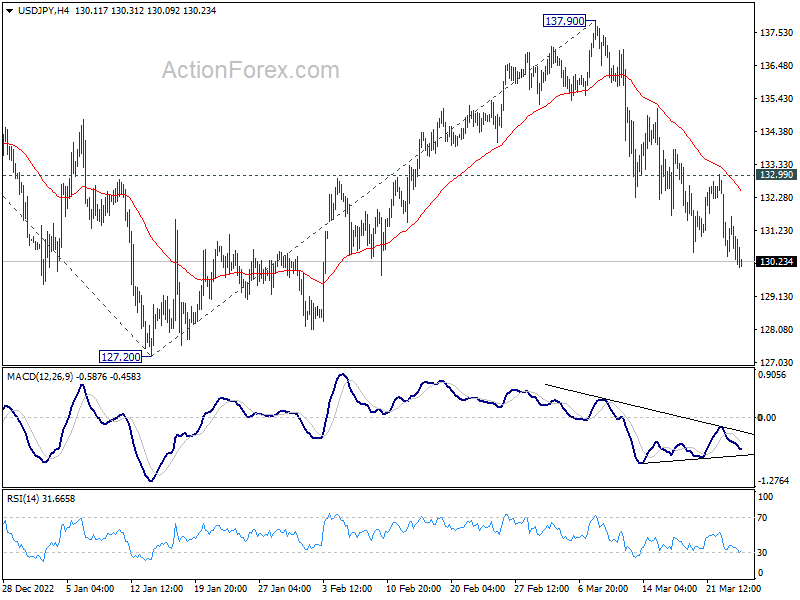

USD/JPY Daily Outlook

Daily Pivots: (S1) 130.23; (P) 130.94; (R1) 131.57; More…

USD/JPY’s fall from 137.90 continues today and edged lower to 130.04. Intraday bias remains on the downside for retesting 127.20 low. Decisive break there will resume larger down trend from 151.93 to 122.61 fibonacci projection level. On the upside, break of 132.99 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

{kind=link}

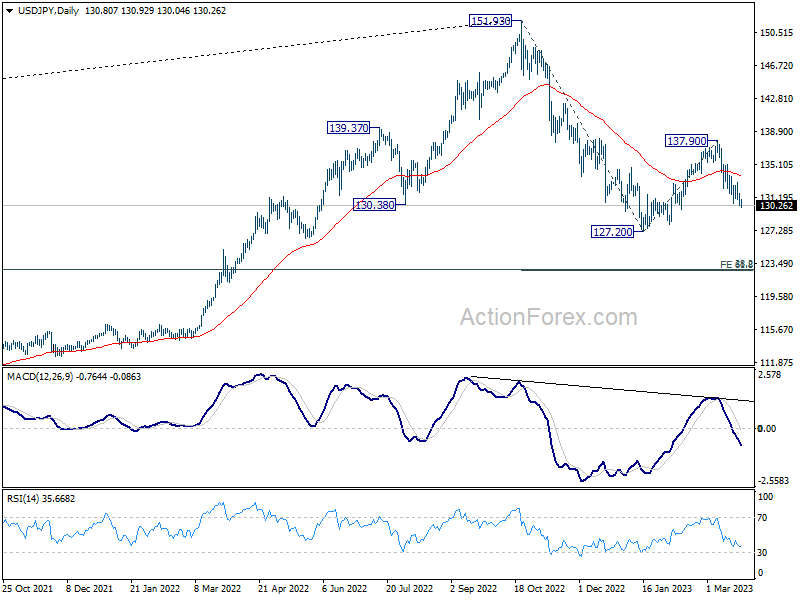

In the bigger picture, rebound from 127.20 should have completed at 137.90 as a corrective move. The down trend from 151.93 (2022 high) is still in progress. Break of 127.20 will resume this down trend and target 61.8% projection of 151.93 to 127.20 from 137.90 at 122.61. This will now be the favored case as long as 137.90 resistance holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:00 | AUD | Manufacturing PMI Mar P | 48.7 | 50.5 | ||

| 22:00 | AUD | Services PMI Mar P | 48.2 | 50.7 | ||

| 23:30 | JPY | CPI Y/Y Feb | 3.30% | 4.10% | 4.30% | |

| 23:30 | JPY | CPI ex-Fresh Food Y/Y Feb | 3.10% | 3.10% | 4.20% | |

| 23:30 | JPY | CPI ex Food & Energy Y/Y Feb | 3.50% | 3.40% | 3.20% | |

| 00:01 | GBP | GfK Consumer Confidence Mar | -36 | -35 | -38 | |

| 00:30 | JPY | Manufacturing PMI Mar P | 48.6 | 48.2 | 47.7 | |

| 00:30 | JPY | Services PMI Mar P | 53.8 | 54 | ||

| 07:00 | GBP | Retail Sales M/M Feb | 0.20% | 0.50% | ||

| 07:00 | GBP | Retail Sales Y/Y Feb | -4.70% | -5.10% | ||

| 07:00 | GBP | Retail Sales ex-Fuel M/M Feb | 0.10% | 0.40% | ||

| 07:00 | GBP | Retail Sales ex-Fuel Y/Y Feb | -4.70% | -5.30% | ||

| 08:15 | EUR | France Manufacturing PMI Mar P | 48.2 | 47.4 | ||

| 08:15 | EUR | France Services PMI Mar P | 53 | 53.1 | ||

| 08:30 | EUR | Germany Manufacturing PMI Mar P | 47.1 | 46.3 | ||

| 08:30 | EUR | Germany Services PMI Mar P | 51.1 | 50.9 | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Mar P | 48.9 | 48.5 | ||

| 09:00 | EUR | Eurozone Services PMI Mar P | 52.9 | 52.7 | ||

| 09:30 | GBP | Manufacturing PMI Mar P | 50 | 49.3 | ||

| 09:30 | GBP | Services PMI Mar P | 53.1 | 53.5 | ||

| 12:30 | CAD | Retail Sales M/M Jan | 0.70% | 0.50% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Jan | 0.60% | -0.60% | ||

| 12:30 | USD | Durable Goods Orders Feb | 0.40% | -4.50% | ||

| 12:30 | USD | Durable Goods Orders ex Transportation Feb | 0.20% | 0.70% | ||

| 13:45 | USD | Manufacturing PMI Mar P | 47.3 | |||

| 13:45 | USD | Services PMI Mar P | 50.6 |