As the mood in the financial markets seems to be rather upbeat, Asian markets are riding the wave of positivity, tracing the upward trajectory set by their US counterparts. All eyes are on FOMC rate decision today, with most expecting a 25 basis point increase. However, uncertainty lingers as opinions within the market remain divided on what next for Fed. Market participants are eager to hear from Fed Chair Jerome Powell during today’s press conference, hoping for clarity on future policy direction, though doubts persist about how much reassurance he can provide.

The currency markets have witnessed Euro taking the lead as the week’s strongest performer, followed closely by Swiss Franc and British Pound. Sterling’s performance will hinge on the release of today’s CPI data and BoE rate decision tomorrow. Meanwhile, the Swiss Franc will turn its attention to SNB rate decision scheduled prior to the BoE’s announcement. Although commodity currencies show signs of recovery, they remain at the bottom of the performance chart. Dollar is currently exhibiting mixed results, faring slightly only better than Yen, Aussie, and Kiwi.

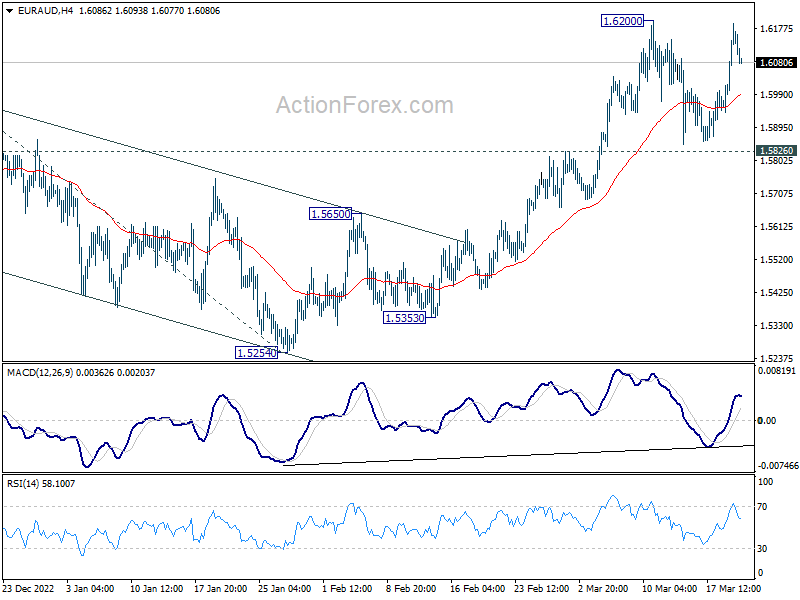

On the technical front, market-watchers are keen to see if Euro can maintain its momentum and extend this week’s robust rally. The surges past 1.0759 resistance in EUR/USD and break of 1.4780 resistance in EUR/CAD were bullish indicators. However, EUR/AUD encountered resistance at 1.6200, and EUR/GBP is grappling to surpass the 0.8842 minor resistance. Euro’s strength will be put to the test as it seeks to solidify its position in the markets.

{kind=link}

In Asia, at the time of writing, Nikkei is up 1.93%. Hong Kong HSI is up 1.88%. China Shanghai SSE is up 0.08%. Singapore Strait Times is up 1.50%. Japan 10-year JGB yield is up 0.319 at 0.724. Overnight, DOW rose 0.98%. S&P 500 rose 1.30%. NASDAQ rose 1.58%. 10-year yield rose 0.125 to 3.606.

Fed expected to hike 25bps, divided opinion on future path

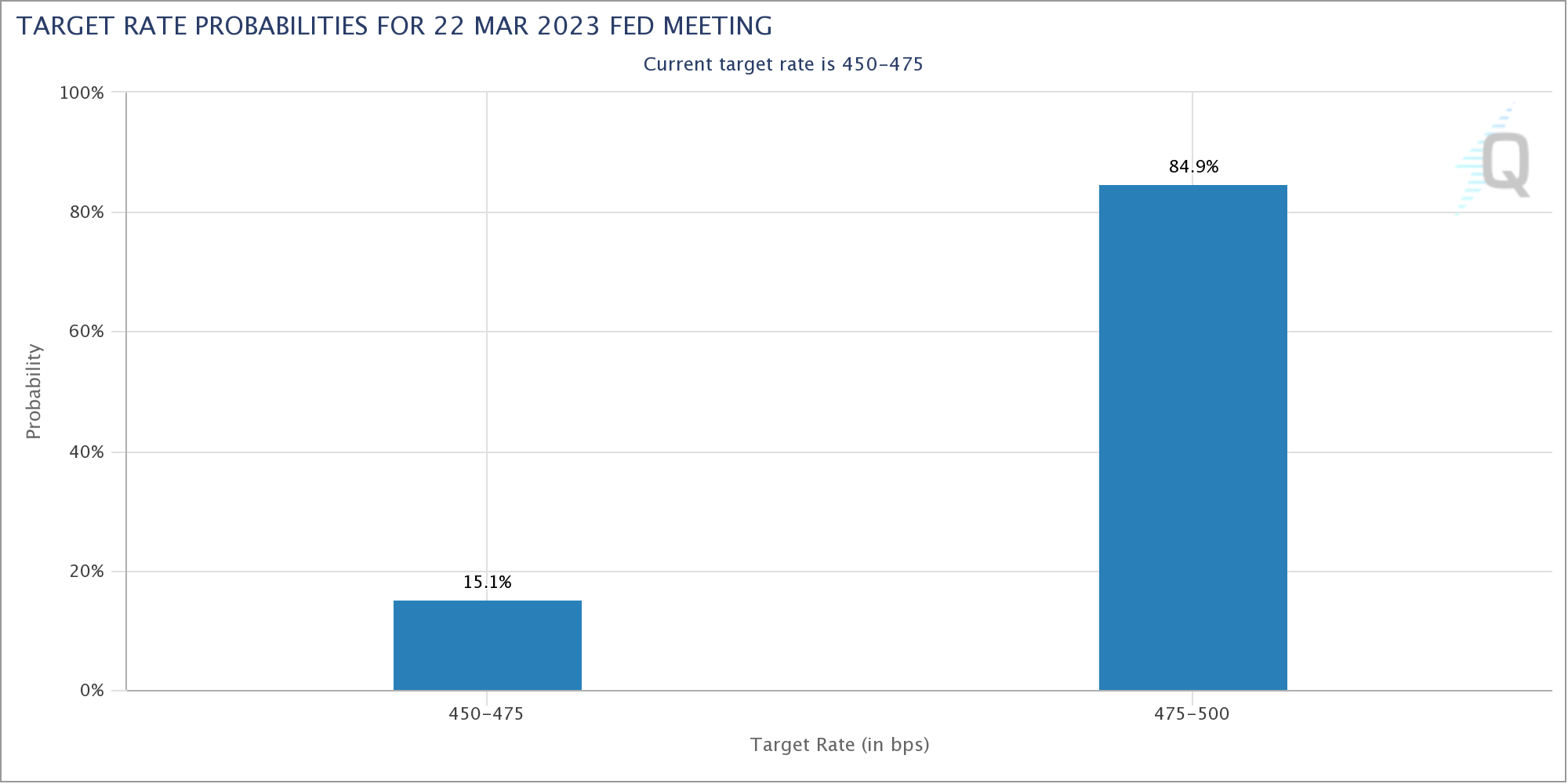

Today marks a significant moment as Fed is expected to continue with its tightening policy. Amid the recent banking crisis and market turmoil, it is widely anticipated that Fed will raise interest rates by 25bps to the 4.75-5.00% range, with around 85% probability. Fed Chair Jerome Powell is likely to stress the importance of bringing inflation back on target during the post-meeting conference, while acknowledging the current market turbulence.

{kind=link}

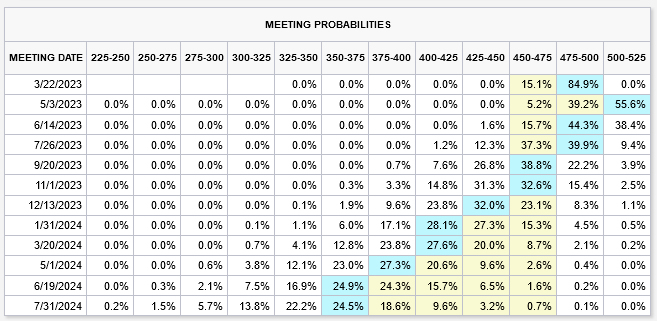

The Fed’s future rate path remains a hot topic of debate. According to Fed fund futures pricing, there is over 55% chance of an additional 25 basis point hike in May, bringing the interest rate to 5.00-5.25%. However, this is followed by a over 62% probability of a -25 basis point cut in June, reverting the rate back to 4.75-5.00%. This apparent contradiction reflects the divided opinions on whether there will be another rate move in May. But in more certainty, traders seem to be leaning more towards a rate cut in September, with around 75% chance of interest rate falling back into the 4.50-4.75% range.

{kind=link}

The new staff economic projections scheduled for release today were initially expected to provide some clarity on the future rate path. However, it is speculated that the Fed might choose to delay or suspend these projections, as it did in March 2020 during the onset of the pandemic, to avoid creating further confusion. As a result, a clear answer to the future rate path may remain elusive for now.

Here are some previews:

Australia Westpac leading index remains negative, indicating further slowdown

Australia’s Westpac Leading Index rose slightly from -1.04% to -0.94% in February, but it still marks the seventh consecutive month of negative growth rate, pointing to below-trend growth over the next 3-9 months. This is in line with Westpac’s forecast that growth in the Australian economy will be only 1% in 2023.

The slowdown reflects the lagged effects of rising interest rates, a deep shock to real wages, a bottoming out of the savings rate, and falling house prices. Westpac also expects the weakness to extend into 2024, with more negative readings likely.

RBA indicated in its March minutes that the board intends to consider a pause at its April meeting. However, Westpac does not expect that a decision to pause in April will mark the end of the cycle. It expects new information for the May meeting to indicate the need for a further response from the board, with a final 0.25% increase in the cash rate in May marking the end of the tightening cycle.

NZ consumer confidence rose slightly to 77.7, but well below long-term average

New Zealand’s Westpac McDermott Miller Consumer Confidence Index rose slightly by 2.1 points to 77.7 in March, but still remains well below the long-term average of 108.8. The President Conditions Index and the Expected Conditions Index also increased, but are still far below their long-term averages of 106.1 and 100.6, respectively.

Despite the slight uptick in confidence, Westpac notes that households across the country continue to grapple with the increasing costs of living, higher mortgage rates, and a downturn in the housing market. The Expected financial situation has improved, but remains negative at -3.8, while the 1-year economic outlook has only slightly improved to -41.1, and the 5-year economic outlook has dropped to -10.8.

The mounting financial pressures are already affecting household spending, and as they become more pronounced, Westpac expects to see an increasing number of households winding back their spending over the next year. This weakness in consumer confidence could have significant implications for the overall economy, as household spending is a major driver of economic growth.

Elsewhere

UK inflation data will also be watched closely in European session, with CPI, RPI and PPI featured. Eurozone will release current account. Canada will publish new housing price index.

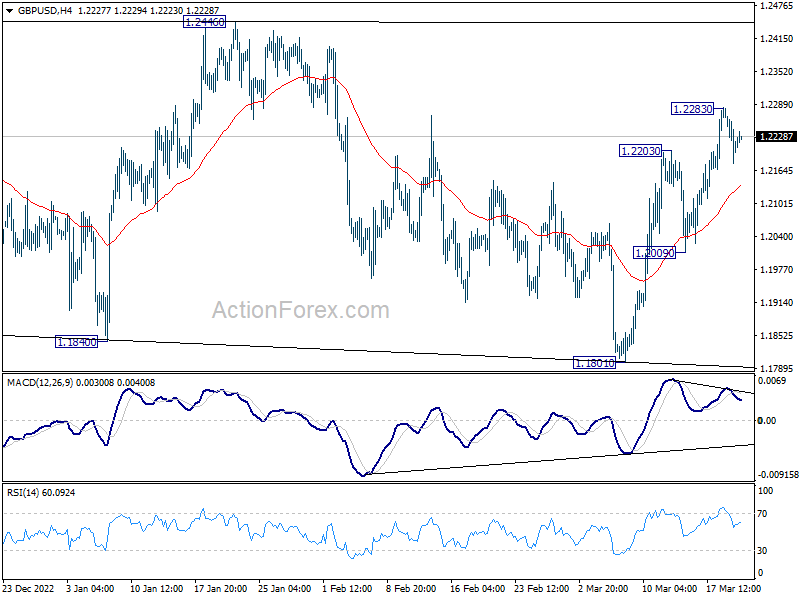

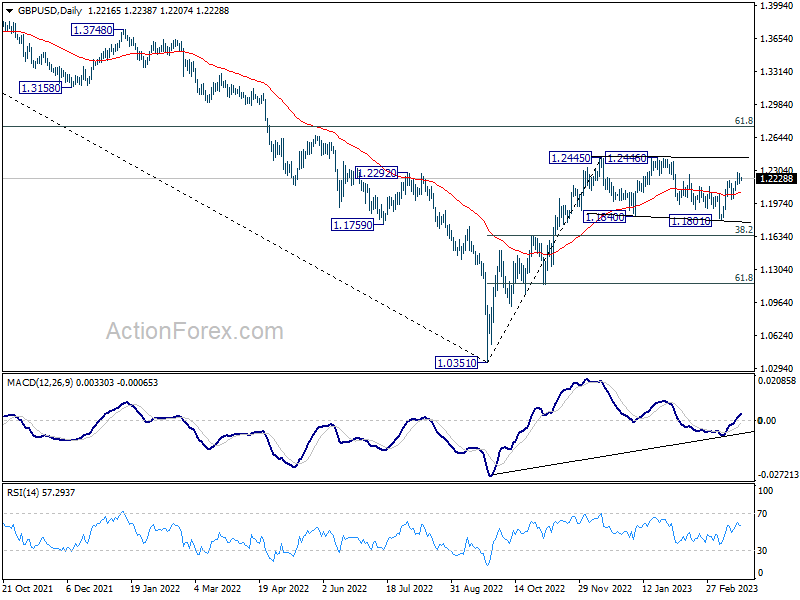

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2170; (P) 1.2226; (R1) 1.2274; More…

Intraday bias in GBP/USD is turned neutral first with current retreat. Some consolidations could be seen below 1.2283 temporary low. But outlook will stay cautiously bullish as long as 1.2009 support hold. As noted before, corrective pattern from 1.2445 could have completed with three waves to 1.1801 already. Above 1.2283 will extend the rise from 1.1801 to retest 1.2445/6 resistance. Firm break of 1.2445/6 will resume larger rise from 1.0351, and target 1.2759 fibonacci level.

{kind=link}

In the bigger picture, price action from 1.2445 are seen as a corrective pattern to rise from 1.0351 medium term bottom (2022 low). Resumption is expected as a later stage and firm break of 1.2446 will target 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759. This will remain the favored case as long as 38.2% retracement of 1.0351 to 1.2445 at 1.1645 holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Leading Index M/M Feb | -0.10% | -0.10% | ||

| 07:00 | GBP | CPI M/M Feb | 0.20% | -0.60% | ||

| 07:00 | GBP | CPI Y/Y Feb | 9.80% | 10.10% | ||

| 07:00 | GBP | Core CPI Y/Y Feb | 5.70% | 5.80% | ||

| 07:00 | GBP | RPI M/M Feb | 0.80% | 0.00% | ||

| 07:00 | GBP | RPI Y/Y Feb | 13.20% | 13.40% | ||

| 07:00 | GBP | PPI Input M/M Feb | 0.70% | -0.10% | ||

| 07:00 | GBP | PPI Input Y/Y Feb | 10.80% | 14.10% | ||

| 07:00 | GBP | PPI Output M/M Feb | 0.80% | 0.50% | ||

| 07:00 | GBP | PPI Output Y/Y Feb | 12.50% | 13.50% | ||

| 07:00 | GBP | PPI Core Output M/M Feb | 0.40% | 0.60% | ||

| 07:00 | GBP | PPI Core Output Y/Y Feb | 9.90% | 11.10% | ||

| 09:00 | EUR | Eurozone Current Account (EUR) Jan | 16.5B | 15.9B | ||

| 12:30 | CAD | New Housing Price Index M/M Feb | -0.10% | -0.20% | ||

| 14:30 | USD | Crude Oil Inventories | -1.7M | 1.6M | ||

| 18:00 | USD | Fed Interest Rate Decision | 5.00% | 4.75% | ||

| 18:30 | USD | FOMC Press Conference |