Euro rises broadly today partly as overall sentiment stabilized. Technical also play a role as the common currency defended near term support levels against both Sterling and Aussie. Poor Germany economic sentiment data was basically ignored by the markets. Market participants appeared to dismiss the poor economic sentiment data from Germany, with the belief that the decline could be temporary

Simultaneously, Swiss Franc and Dollar are making recoveries against other currencies. Canadian Dollar showed little response to lower-than-anticipated CPI readings, which essentially reinforced BoC’s decision to maintain the current interest rate levels, at least for the near future. Other commodity currencies, however, are exhibiting weakness. Australian Dollar, for instance, is facing pressure following the RBA minutes, suggesting a potential pause in their next meeting.

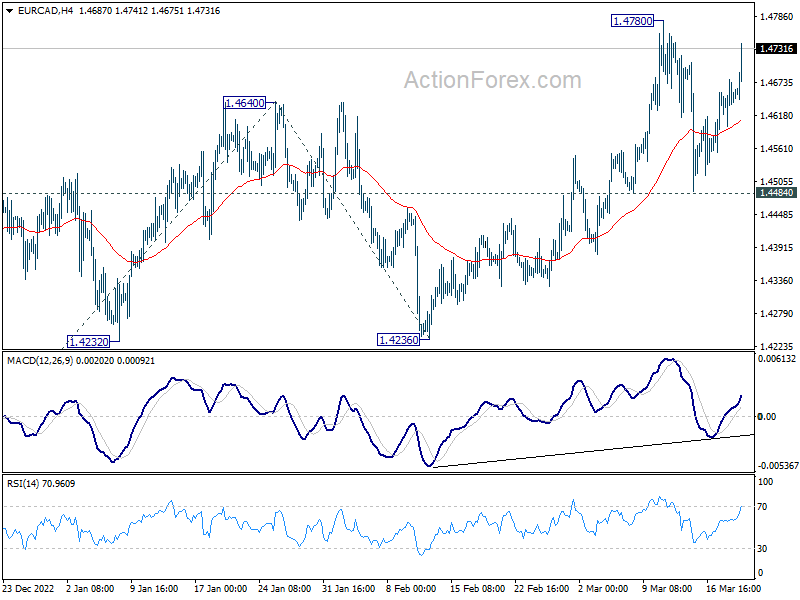

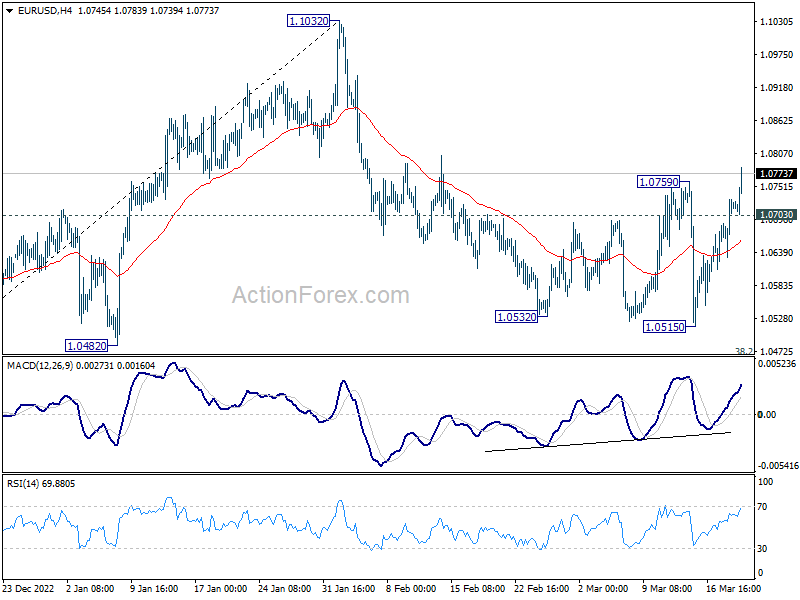

Technically, EUR/USD’s break of 1.0759 resistance is taken as an indication of near term reversal. That is, further rise is now likely to be seen back to retest 1.1032 high. Two focuses will now be on 1.4780 resistance in EUR/CAD and 1.6200 resistance in EUR/AUD. Break of these two levels should solidify Euro’s upside momentum.

{kind=link}

In Europe, at the time of writing, FTSE is up 1.81%. DAX is up 1.87%. CAC is up 1.82%. Germany 10-year yield is up 0.1525 at 0.273. Earlier in Asia, Hong Kong HSI rose 1.36%. China Shanghai SSE rose 0.64%. Singapore Strait Times rose 1.09%. Japan was on holiday.

Canada CPI slowed to 5.2% yoy in Feb, below expectation of 5.4% yoy

Canada CPI slowed from 5.9% yoy to 5.2% yoy in February, below expectation of 5.4% yoy. Excluding food and energy, CPI slowed slightly from 4.9% yoy to 4.8% yoy. All-items CPI excluding mortgage interest costs slowed from 5.4% yoy to 4.7% yoy.

On a monthly basis, CPI rose 0.4% mom, slowed from January’s 0.5% mom, and below expectation of 0.5% mom. Decline in energy prices were offset by rise in mortgage interest costs.

Meanwhile, CPI median decreased from 5.0% yoy to 4.9% yoy above expectation of 4.8% yoy. CPI trimmed fell from 5.1% yoy to 4.8% yoy, below expectation of 4.9% yoy. CPI common declined from 6.6% yoy to 6.4% yoy, below expectation of 6.5% yoy.

German ZEW fell sharply to 13 in Mar, reflecting financial markets pressure

German ZEW Economic Sentiment deteriorated sharply from 28.1 to 13.0 in March, below expectation of 14.9. Current Situation index also dropped from -45.1 to -46.5, below expectation of -44.3.

Eurozone ZEW Economic Sentiment dropped from 29.7 to 10.0, below expectation of 16.0. Eurozone Current Situation dropped -3 pts to -44.6.

ZEW President Professor Achim Wambach said: “The international financial markets are under strong pressure. This high level of uncertainty is also reflected in the ZEW Indicator of Economic Sentiment.

“The assessment of the earnings development of banks has deteriorated considerably, although it still remains slightly positive. The estimates for the insurance industry have also declined significantly.”

RBA Minutes: To reconsider a pause at next meeting

The minutes of RBA’s meeting on March 7 indicate that the central bank is considering a more cautious approach in tightening monetary policy, as uncertainty surrounding the economic outlook persists. The RBA members observed that “further tightening of monetary policy would likely be required to ensure that inflation returns to target.” However, they also noted the restrictive nature of current monetary policy and the economic uncertainty, stating that “it would be appropriate at some point to hold the cash rate steady.”

During the meeting, RBA members agreed to “reconsider the case for a pause at the following meeting, recognizing that pausing would allow additional time to reassess the outlook for the economy.” The decision on when to pause will be determined by incoming data and the board’s assessment of the economic situation.

The RBA acknowledges that “the outlook for consumption remained a key source of uncertainty.” The central bank will closely monitor upcoming data releases on employment, inflation, retail trade, and business surveys, as well as developments in the global economy, to inform their decision-making.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0660; (P) 1.0696; (R1) 1.0759; More…

EUR/USD’s break of 1.0759 resistance suggests that correction from 1.1032 has completed at 1.0515 already. That came after defending both 1.0482 support and 38.2% retracement of 0.9534 to 1.1032 at 1.0258. Intraday bias is back on the upside for retesting 1.1032 high next. On the downside, below 1.0703 minor support will turn intraday bias neutral again first.

{kind=link}

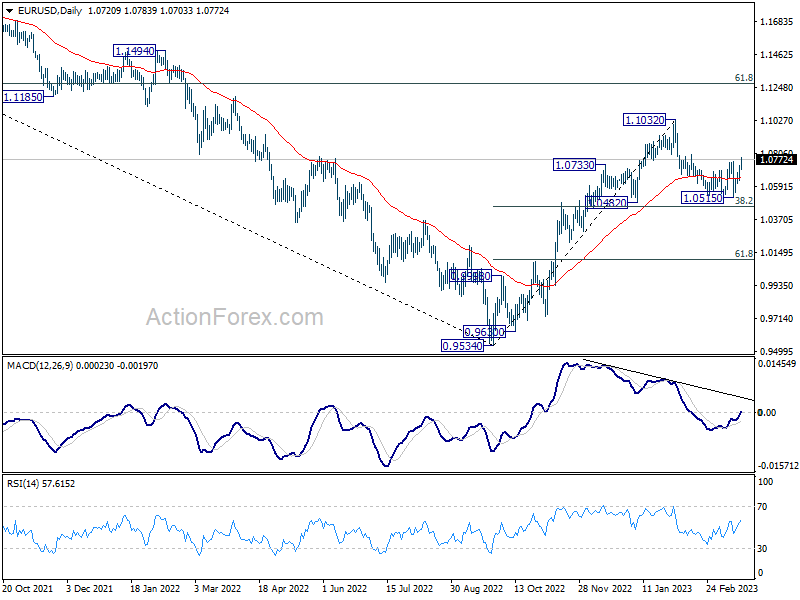

In the bigger picture, as long as 1.0482 support holds, rise from 0.9534 (2022 low) should continue to 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. However, sustained break of 1.0482 will bring deeper fall to 61.8% retracement of 0.9534 to 1.1032 at 1.0106, with risk of breaking through 0.9534 eventually.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Feb | -714M | -1800M | -1954M | -2113M |

| 00:30 | AUD | RBA Minutes | ||||

| 07:00 | CHF | Trade Balance (CHF) Feb | 3.31B | 3.45B | 5.08B | 4.85B |

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Feb | 15.9B | 10.5B | -6.2B | -9.1B |

| 10:00 | EUR | Germany ZEW Economic Sentiment Mar | 13 | 14.9 | 28.1 | |

| 10:00 | EUR | Germany ZEW Current Situation Mar | -46.5 | -44.3 | -45.1 | |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Mar | 10 | 16 | 29.7 | |

| 12:30 | CAD | CPI M/M Feb | 0.40% | 0.50% | 0.50% | |

| 12:30 | CAD | CPI Y/Y Feb | 5.20% | 5.40% | 5.90% | |

| 12:30 | CAD | CPI – Core M/M Feb | 0.30% | 0.10% | ||

| 12:30 | CAD | CPI Median Y/Y Feb | 4.90% | 4.80% | 5.00% | |

| 12:30 | CAD | CPI Trimmed Y/Y Feb | 4.80% | 4.90% | 5.10% | |

| 12:30 | CAD | CPI Common Y/Y Feb | 6.40% | 6.50% | 6.60% | |

| 14:00 | USD | Existing Home Sales Feb | 4.17M | 4.00M |