Australian Dollar is declining broadly as RBA minutes hinted at the possibility of a pause during their next meeting. Meanwhile, Yen has managed to hold on to the some gains it made earlier this week and appears poised for further rallying, particularly against commodity-based currencies.

Both Euro and Sterling have maintained their strength after being bought against Swiss Franc. However, their momentum seems to have slowed down a bit. Dollar is on the path to recovery from previous losses but all would depend on tomorrow’s FOMC rate decision. Canadian Dollar remains in a mixed state as market participants eagerly await the release of the Canada CPI data.

Elsewhere in the markets, the banking crisis seems to have reached a point of stabilization at last, with hope that this trend will continue. Asian stock markets are making a comeback, taking cues from the rebound in US markets. Benchmark treasury yields in both the US and Europe have also bounced back, signaling a halt in the flow of funds towards safe-haven assets.

Gold, after spiking higher yesterday, is currently in a consolidation phase. However, it remains poised to potentially break through the 2000 mark again in the near future.

In Asia, at the time of writing, Hong Kong HSI is up 0.33%. China Shanghai SSE is up 0.15%. Singapore Strait Times is up 1.31%. Japan is on holiday. Overnight, DOW rose 1.20%. S&P 500 rose 0.89%. NASDAQ rose 0.39%. 10-year yield rose 0.086 to 3.481.

RBA Minutes: To reconsider a pause at next meeting

The minutes of RBA’s meeting on March 7 indicate that the central bank is considering a more cautious approach in tightening monetary policy, as uncertainty surrounding the economic outlook persists. The RBA members observed that “further tightening of monetary policy would likely be required to ensure that inflation returns to target.” However, they also noted the restrictive nature of current monetary policy and the economic uncertainty, stating that “it would be appropriate at some point to hold the cash rate steady.”

During the meeting, RBA members agreed to “reconsider the case for a pause at the following meeting, recognizing that pausing would allow additional time to reassess the outlook for the economy.” The decision on when to pause will be determined by incoming data and the board’s assessment of the economic situation.

The RBA acknowledges that “the outlook for consumption remained a key source of uncertainty.” The central bank will closely monitor upcoming data releases on employment, inflation, retail trade, and business surveys, as well as developments in the global economy, to inform their decision-making.

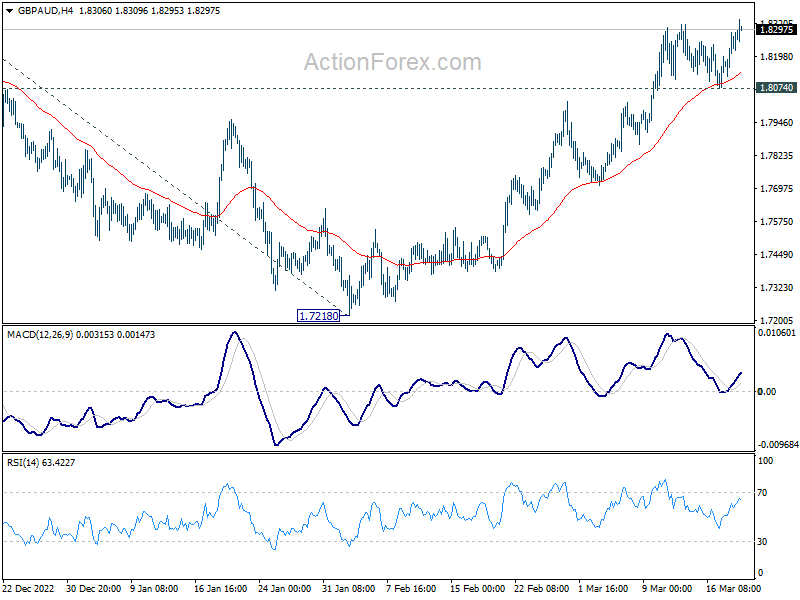

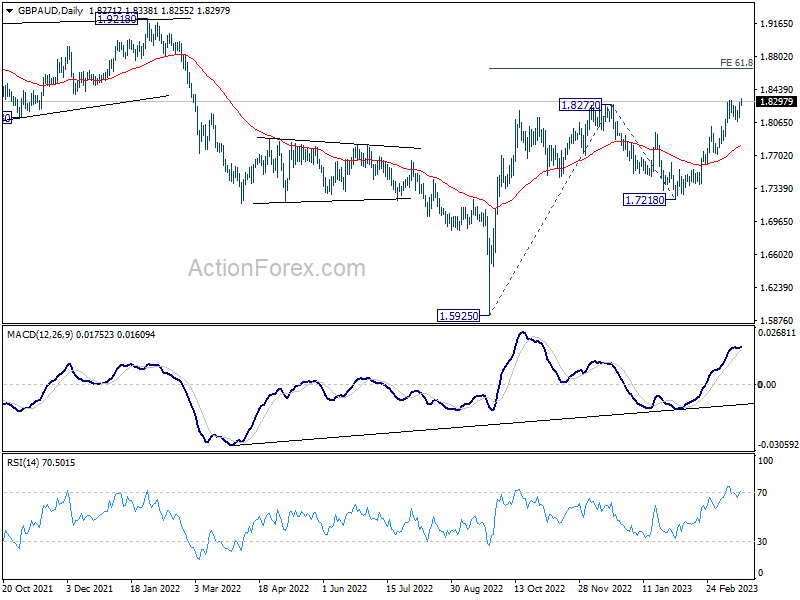

GBP/AUD resuming rally after dovish RBA minutes

Australian Dollar trades mildly lower after RBA minutes indicated the possibility of a pause in tightening at next meeting. On the other hand, Sterling (and Euro too) is supported by funds flow from Swiss Franc. But there are some uncertainties for the Pound ahead with UK CPI and BoE rate decisions scheduled later in the week.

Technically, GBP/AUD is resuming the near term rise by breaking last week’s high at 1.8316. At the same time, rise from 1.7218 is likely resuming the whole up trend from 1.5925. Near term outlook will stay bullish as long as 1.8074 support holds, even in case of retreat. Next target is 61.8% projection of 1.5925 to 1.8272 from 1.7218 at 1.8668. Nevertheless, break of 1.8074 support will delay the bullish case and bring some consolidations before another rally attempt.

{kind=link}

{kind=link}

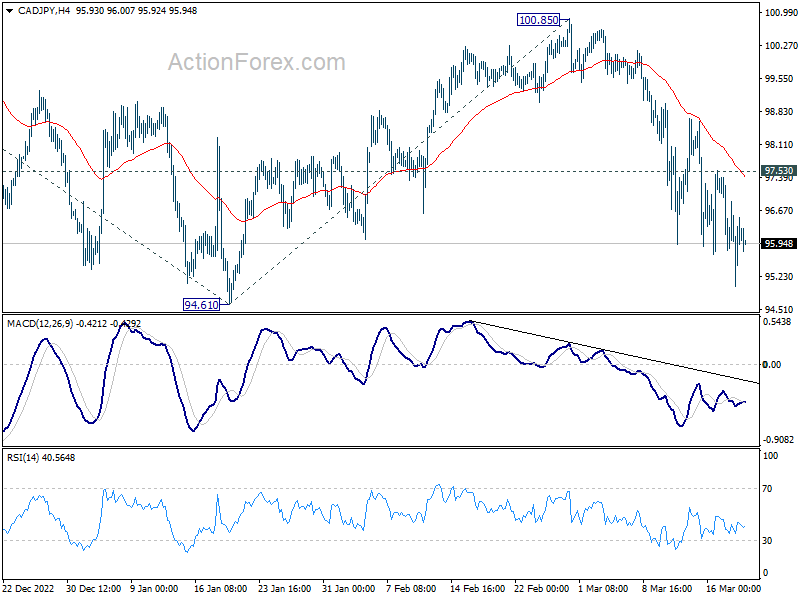

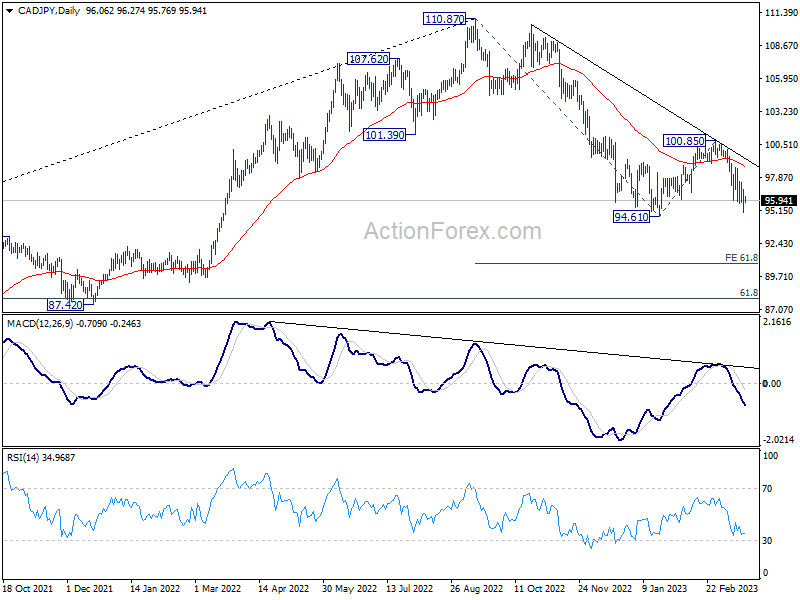

CAD/JPY ready for down trend resumption as Canada CPI looms

Today, Canada’s consumer inflation data takes center stage as markets anticipate a slowdown in headline inflation from 5.9% yoy to 5.4% yoy in February. If this decrease materializes, it would mark the lowest inflation reading in over a year. BoC’s preferred core inflation metrics, the trimmed and median CPI, are also projected to decelerate from 5.1% yoy to 4.8% yoy and from 5.0% yoy to 4.8% yoy, respectively.

BoC became the first major central bank to pause its tightening cycle last Wednesday, following eight consecutive rate hikes totaling 425 basis points. Market participants are still expecting one more rate increase this year, but these odds could dwindle if inflation continues to decline.

CAD/JPY is closely watching the 94.61 support level after a recent drop. A decisive break below this threshold would rekindle the broader downtrend from the 110.87 high and aim for a 61.8% projection of 110.87 to 94.61 from 100.85 at 90.80. However, if the cross breaks above 97.53 resistance, it could delay the bearish scenario and extend the corrective pattern from 94.61 with another upswing.

{kind=link}

{kind=link}

Looking ahead

Germany ZEW economic sentiment will be the man focus in European session. UK will release public sector net borrowing. Swiss will publish trade balance. Later in the day, Canada CPI will take center stage while US will release existing home sales.

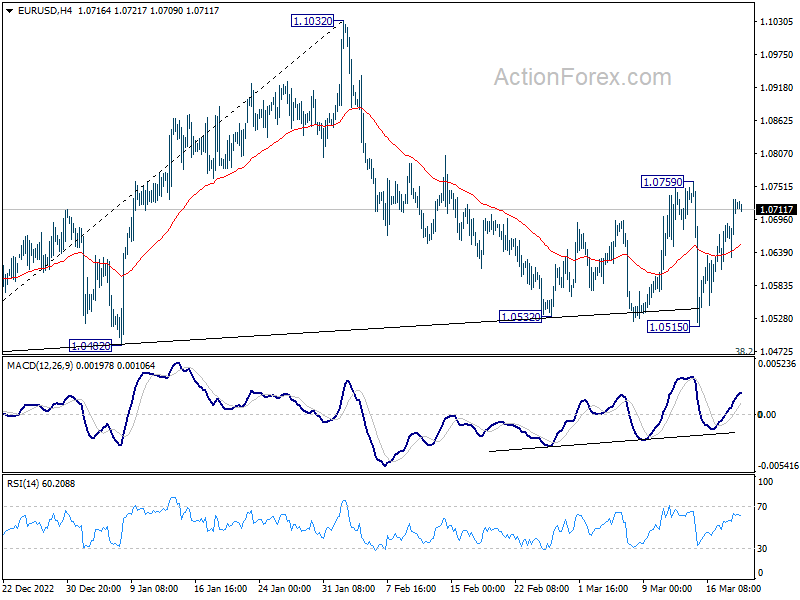

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0660; (P) 1.0696; (R1) 1.0759; More…

EUR/USD is holding inside range of 1.0515/0759 and intraday bias remains neutral. Focus stays on 1.0759 resistance. Firm break there will argue that corrective fall from 1.1032 has completed at 1.0515, ahead of 38.2% retracement of 0.9534 to 1.1032 at 1.0258. Intraday bias will be turned back to the upside for retesting 1.1032 high. Nevertheless, sustained break of 1.0258 will turn near term outlook bearish for 61.8% retracement at 1.0106.

{kind=link}

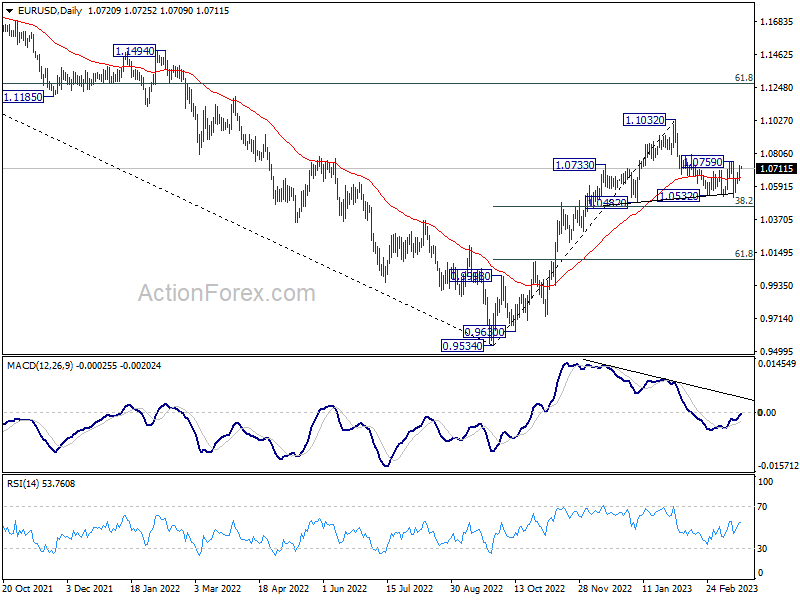

In the bigger picture, as long as 1.0482 support holds, rise from 0.9534 (2022 low) should continue to 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. However, sustained break of 1.0482 will bring deeper fall to 61.8% retracement of 0.9534 to 1.1032 at 1.0106, with risk of breaking through 0.9534 eventually.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Feb | -714M | -1800M | -1954M | -2113M |

| 00:30 | AUD | RBA Minutes | ||||

| 07:00 | CHF | Trade Balance (CHF) Feb | 3.45B | 5.08B | ||

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Feb | 10.5B | -6.2B | ||

| 10:00 | EUR | Germany ZEW Economic Sentiment Mar | 22.6 | 28.1 | ||

| 10:00 | EUR | Germany ZEW Current Situation Mar | -35.1 | -45.1 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Mar | 23.2 | 29.7 | ||

| 12:30 | CAD | CPI M/M Feb | 0.50% | 0.50% | ||

| 12:30 | CAD | CPI Y/Y Feb | 5.40% | 5.90% | ||

| 12:30 | CAD | CPI – Core M/M Feb | 0.10% | |||

| 12:30 | CAD | CPI Median Y/Y Feb | 4.80% | 5.00% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Feb | 4.90% | 5.10% | ||

| 12:30 | CAD | CPI Common Y/Y Feb | 6.50% | 6.60% | ||

| 14:00 | USD | Existing Home Sales Feb | 4.17M | 4.00M |