Overall, the markets continue to trade in a mixed manner. US stocks declined for a second day overnight, but the selloff didn’t continue in Asia. Sentiment is somewhat supported by optimism of easing restrictions in China. In the currency markets, Yen is currently the worst performer for the week, followed by Aussie. Canadian Dollar is also soft as focus turns to BoC rate hike today. Dollar is recovering but lacks clear momentum, except versus Loonie. European majors are mixed, with Swiss Franc slightly stronger.

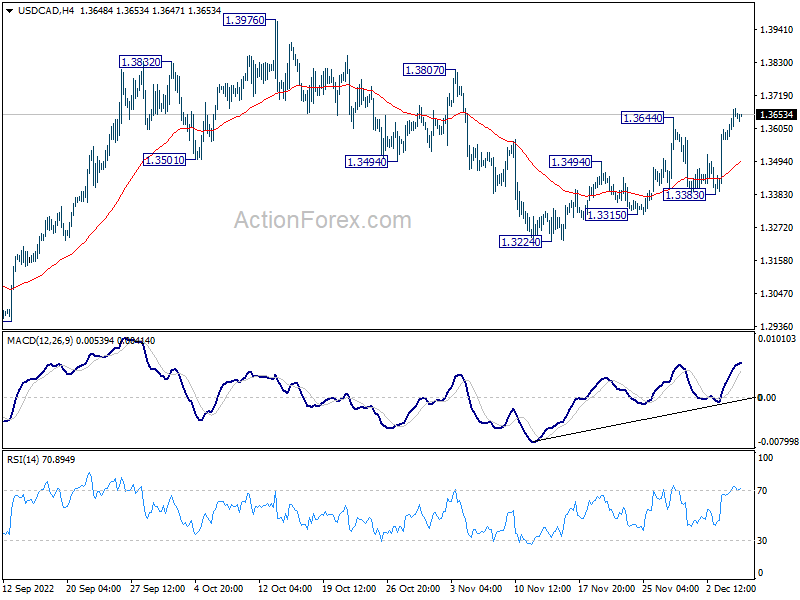

Technically, USD/CAD’s break of 1.3644 resistance indicates resumption of whole rise from 1.3224. Further rally is now in favor towards 1.3807 resistance next. But equivalent move is not seen in other Dollar pairs yet. Eyes will be on 0.6641 support in AUD/USD, 1.0427 minor support in EUR/USD, and 137.66 resistance in USD/JPY.

{kind=link}

In Asia, Nikkei dropped -0.64%. Hong Kong HSI is down -0.04%. China Shanghai SSE is down -0.39%. Singapore Strait Times is down -0.07%. Japan 10-year JGB yield is down -0.0025 at 0.250. Overnight, DOW dropped -1.03%. S&P 500 dropped -1.44%. NASDAQ dropped -2.00%. 10-year yield dropped -0.086 to 3.513.

BoJ Nakamura: Inflation not accompanied by wage increases yet

BoJ board member Toyoaki Nakamura said, “recent price rises aren’t accompanied by wage increases yet”. He added that Japan is far from the situation where wage inflation spiral becomes a concern. The central bank needs to continue with ultra-loose monetary policy for the time being.

“Tightening monetary policy at a time when demand continues to remain lower than supply would put huge pressure on corporate and household activity,” he warned.

He expects inflation to slow next year as energy and food price rises fade.

Australia AiG services fell to 45.6, deepening contraction

Australia AiG Performance of Services dropped -2.1 pts to 45.6 in November, signaling contraction for a third month. Sales rose 1.5 to 42.8. Employment dropped -6.1 to 47.8. New orders dropped -4.8 to 49.7. Input prices dropped -3.6 to 74.0. Selling prices rose 2.2 to 64.4. Average wages rose 3.8 to 68.6.

Innes Willox, Chief Executive of the national employer association Ai Group, said: “The deteriorating economic outlook is clearly weighing on Australia’s services sector. The Australian PSI indicated a deepening contraction in the services sector, with three months of declining results. Steep falls in indicators for employment and new orders in November reveal weakening demand for services, while ongoing labour shortages continue to constrain the supply side.”

Australia GDP grew 0.6% qoq in Q3, terms of trade deteriorated

Australia GDP grew 0.6% qoq in Q3, below expectation of 0.7% qoq. Household spending rose 1.1%, contributing 0.6% to GDP. Compensation of employees increased 3.2%, the strongest rise since December quarter 2006. Net trade detracted -0.2% from GDP, with a 2.7% increase in exports offset by a 3.9% rise in imports. The terms of trade fell -6.6%, the largest fall since June quarter 2009, as import prices increased and export prices fell.

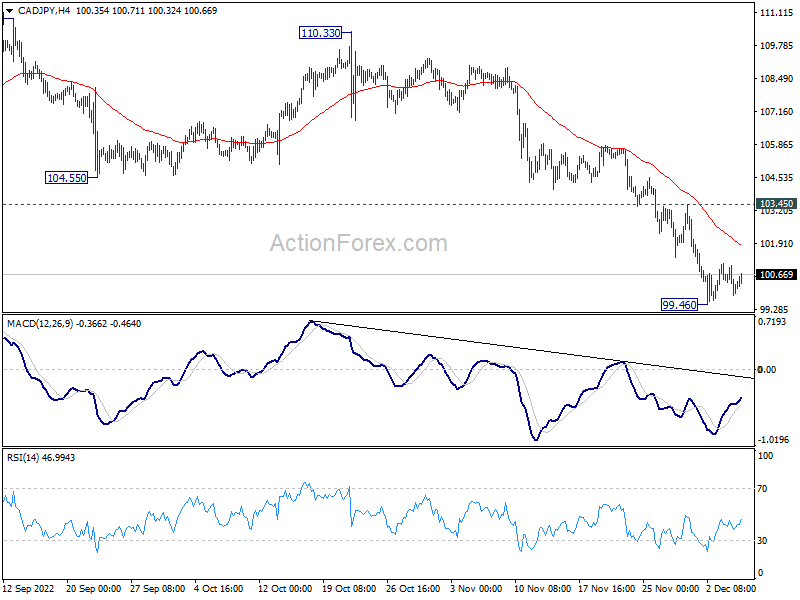

CAD/JPY struggling at 100, eyes on BoC hike

BoC is widely expected to continue with tightening today. But opinion on the size of the rate hike is split, with odds slightly in favor to 50 than 25. The main question, though, is not about how much the hike is, but how BoC would indicate the path forward. That is, how close interest is to the terminal rate. This is what the statement would be scrutinized for.

Some suggested readings on BoC:

{kind=link}

{kind=link}

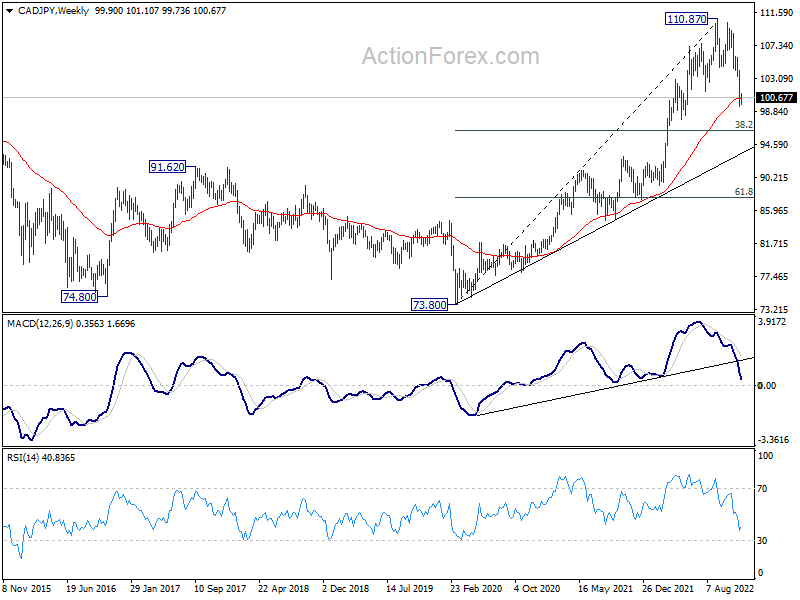

CAD/JPY’s decline halted last week after hitting 99.46, but it’s just struggling around 100 handle, with no momentum for a solid rebound. For now, deeper fall is expected as long as 4 hour 55 EMA (now at 101.88) holds. Break of 99.46 will resume the decline from 110.87 as a long term correction. CAD/JPY should have a take on 38.2% retracement of 73.80 to 110.87 at 96.70 before forming a bottom.

Elsewhere

Swiss unemployment rate and foreign currency reserves, Germany industrial production, France trade balance, Italy retail sales, Eurozone GDP final will be released in European session. US will release Q3 non-farm productivity later in the day.

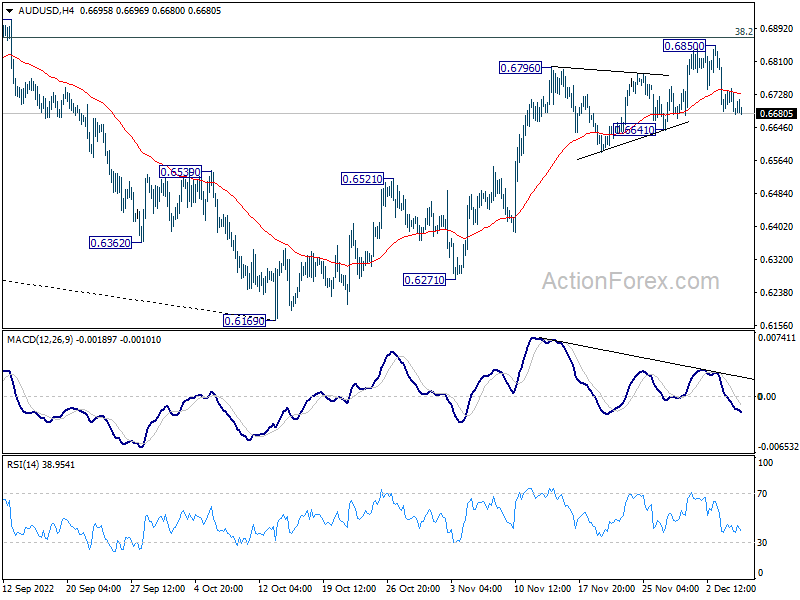

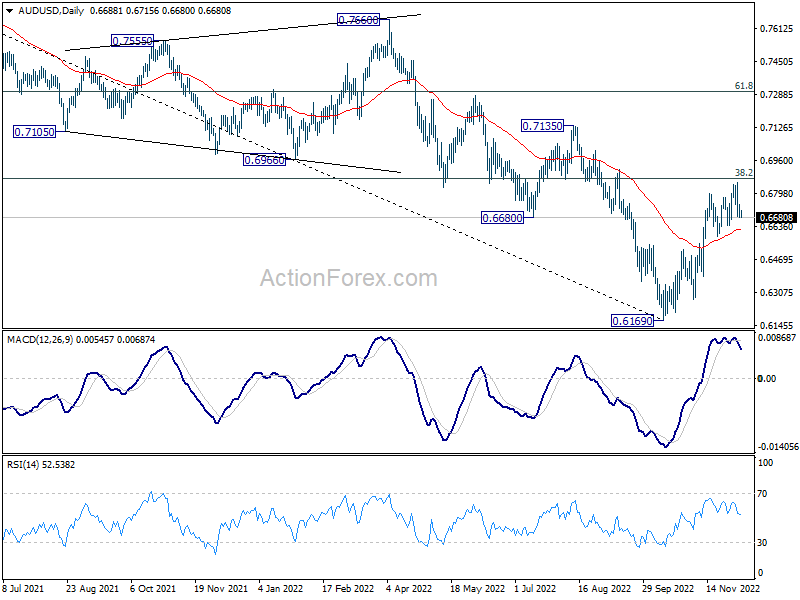

AUD/USD Daily Report

Daily Pivots: (S1) 0.6665; (P) 0.6704; (R1) 0.6728; More…

Intraday bias in AUD/USD remains neutral for the moment. Considering bearish divergence condition in 4 hour MACD, break of 0.6641 support should indicate short term topping, following rejection by 0.6871 fibonacci level. Intraday bias will be back on the downside for 0.6521 resistance turned support first.

{kind=link}

In the bigger picture, a medium term bottom is in place at 0.6160 already. But it’s too early to call for trend reversal. Nevertheless, even as a corrective move, rise from 0.6169 should target 38.2% retracement of 0.8006 to 0.6169 at 0.6871. Sustained trading above 55 week EMA (now at 0.6922) will raise the chance of the start of a bullish up trend. However, rejection by 0.6781 or 55 week EMA, followed by 0.6521 resistance turned support and retain medium term bearishness.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Services Index Nov | 45.6 | 47.7 | ||

| 00:30 | AUD | GDP Q/Q Q3 | 0.60% | 0.70% | 0.90% | |

| 03:00 | CNY | Trade Balance (USD) Nov | 69.8B | 79.1B | 85.2B | |

| 03:00 | CNY | Exports (USD) Y/Y Nov | -8.70% | -3.50% | -0.30% | |

| 03:00 | CNY | Imports (USD) Y/Y Nov | -10.60% | -6.00% | -0.70% | |

| 03:00 | CNY | Trade Balance (CNY) Nov | 494B | 580B | 587B | |

| 03:00 | CNY | Exports (CNY) Y/Y Nov | 0.90% | 7% | ||

| 03:00 | CNY | Imports (CNY) Y/Y Nov | -1.10% | 4.10% | 6.80% | |

| 05:00 | JPY | Leading Economic Index Oct P | 99.0 | 96.6 | 97.5 | |

| 06:45 | CHF | Unemployment Rate Nov | 2.10% | 2.10% | ||

| 07:00 | EUR | Germany Industrial Production M/M Oct | -0.60% | 0.60% | ||

| 07:45 | EUR | France Trade Balance (EUR) Oct | -15.9B | -17.5B | ||

| 08:00 | CHF | Foreign Currency Reserves (CHF) Nov | 817B | |||

| 09:00 | EUR | Italy Retail Sales M/M Oct | 0.10% | 0.50% | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q3 F | 0.20% | 0.20% | ||

| 10:00 | EUR | Eurozone Employment Change Q/Q Q3 F | 0.20% | 0.20% | ||

| 13:30 | USD | Nonfarm Productivity Q3 | 0.30% | 0.30% | ||

| 13:30 | USD | Unit Labor Costs Q3 | 3.50% | 3.50% | ||

| 15:00 | CAD | BoC Interest Rate Decision | 4.25% | 3.75% | ||

| 15:30 | USD | Crude Oil Inventories | -3.5M | -12.6M |