Yen and Dollar rise broadly in Asian session today while Australian Dollar leads commodity currencies lower. Markets are trading with risk-off sentiment, with deeper selloff in China and Hong Kong markets. Large scale protests were carried out in multiple cities in China over the weekend, and the theme has escalated from anti-lockdown to anti-President Xi Jinping and the Chinese Communist Party. The development in China will be a key factor for sentiment over the next few days, along with US job data and Eurozone inflation later in the week.

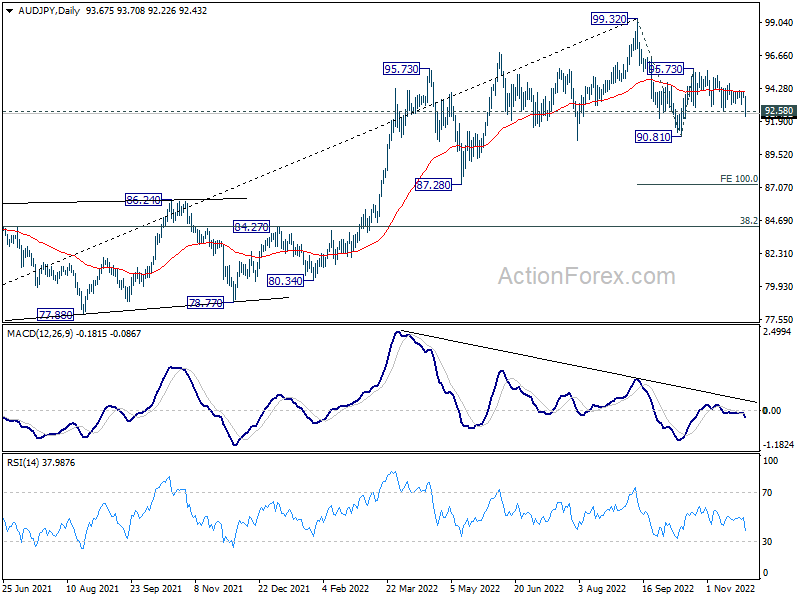

Technically, the break of 92.58 minor support in AUD/JPY suggests that recovery from 90.81 has completed after failing to sustain above 55 day EMA. Deeper decline is now in favor back to retest 90.81 first. Firm break there will extend the decline from 99.32, as a correction to larger up trend from 2020 low at 59.85. Next target is 100% projection of 99.32 to 90.81 from 95.73 at 87.22.

{kind=link}

In Asia, Nikkei dropped -0.42%. Hong Kong HSI is down -2.15%. China Shanghai SSE is down -1.39%. Singapore Strait Times is down -0.52%. Japan 10-year JGB yield dropped -0.0053 to 0.255.

Australia retail sales fell -0.2% mom in Oct, first decline this year

Australia retail sales turnover dropped -0.2% mom to AUD 35.02B in October, much worse than expectation of 0.5% mom rise. That’s also the first monthly decline in 2022.

Ben Dorber, ABS head of retail statistics said: “The October fall in retail turnover ends a run of nine straight monthly rises and suggests increased cost of living pressures including interest rate rises have started to weigh on consumer spending.”

“Turnover fell in all industries in October except for food retailing, which rose 0.4 per cent boosted by flood-related spending in parts of Australia and continued high food prices.”

RBA Lowe: Best outcome is for wages to pick up but not too much further

RBA Governor Philip Lowe told a parliamentary committee that the central bank is keeping an eye on electricity prices and housing. “If we can address those two issues then that will make a substantial contribution in bringing inflation back down over the next couple of years,” he said.

Also, he added that a massive spike in wages would make it harder to bring inflation down. “If wage growth was 7 or 8 per cent then inflation would be 6 or 7 per cent … we were in this world in the 1970s and it worked out very badly,” Lowe said. “The best outcome for the country is for wages to pick up but to not go too much further.”

RBNZ Silk: The persistence factor of inflation was most surprising

RBNZ Assistant Governor Karen Silk said in an interview, “What we have seen is actual inflation continue to surprise on the upside, but more importantly inflation expectations have moved higher as well… And it’s the persistence factor that has probably been the most surprising.”

On tightening, “obviously we started way earlier than other central banks, so other central banks had to move an awful lot faster basically to play catch up,” she said. “So no, I don’t believe that the MPC has dilly-dallied around on this at all.”

“If the information shows that we’ve reached that peak (5.5% interest rate) and we see that turn and we’re starting to see real impacts on inflation and inflation expectations, then that does offer us the opportunity to revisit,” she said.

US NFP and Eurozone CPI to confirm size of Dec rate hikes

Job data from the US and inflation data from Eurozone are the biggest events this week. Both could be the final piece of data that decide the size of rate hikes of Fed and ECB. In addition, US will release consumer confidence, ISM manufacturing, and PCE inflation.

Elsewhere data to be watched include Japan industrial production and retail sales, Swiss GDP and CPI, Canada GDP, New Zealand ANZ business confidence, and China PMIs.

Here are some highlights for the week:

- Monday: Australia retail sales; Eurozone M3 money supply; Canada current account.

- Tuesday: Japan unemployment rate, retail sales; Germany CPI flash; Swiss GDP; UK M4 money supply, mortgage approvals; Canada GDP; US house price index, consumer confidence.

- Wednesday: New Zealand ANZ business confidence; Australia building approvals, construction work done; Japan industrial production, housing starts; China PMIs; France consumer spending, GDP revision; Swiss KOF; Germany unemployment; Eurozone CPI flash; US ADP employment; GDP revision, goods trade balance, Chicago PMI, pending home sales, Fed Beige Book.

- Thursday: Australia AiG manufacturing, private capital expenditure; Japan PMI manufacturing final, capital spending, consumer confidence; China Caixin PMI manufacturing; Germany retail sales; Swiss CPI, retail sales; Eurozone PMI manufacturing final, unemployment rate; UK PMI manufacturing final; US Challenger job cuts, jobless claims, personal income and spending, ISM manufacturing, construction spending.

- Friday: New Zealand terms of trade; Japan monetary base; Germany import prices, trade balance; Eurozone PPI; Canada employment; US non-farm payroll.

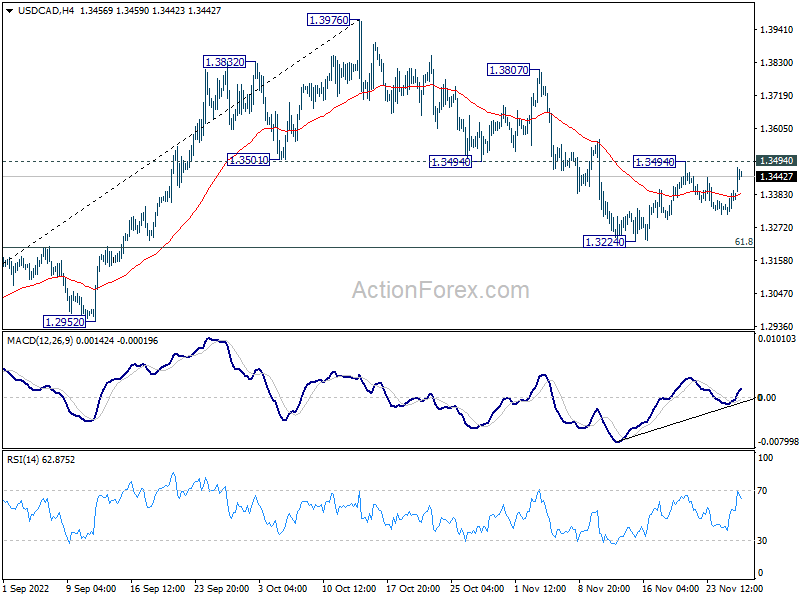

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3332; (P) 1.3366; (R1) 1.3414; More….

Intraday bias in USD/CAD stays neutral for the moment. On the upside, firm break of 1.3494 will indicate that correction from 1.3976 has completed at 1.3224, ahead of 1.3207 cluster support (61.8% retracement of 1.2726 to 1.3976 at 1.3204). Intraday bias will be turned back to the upside for 1.3807/3976 resistance zone. However, on the downside, sustained break of 1.3204/7 will carry larger bearish implication and target 1.2952 support next.

{kind=link}

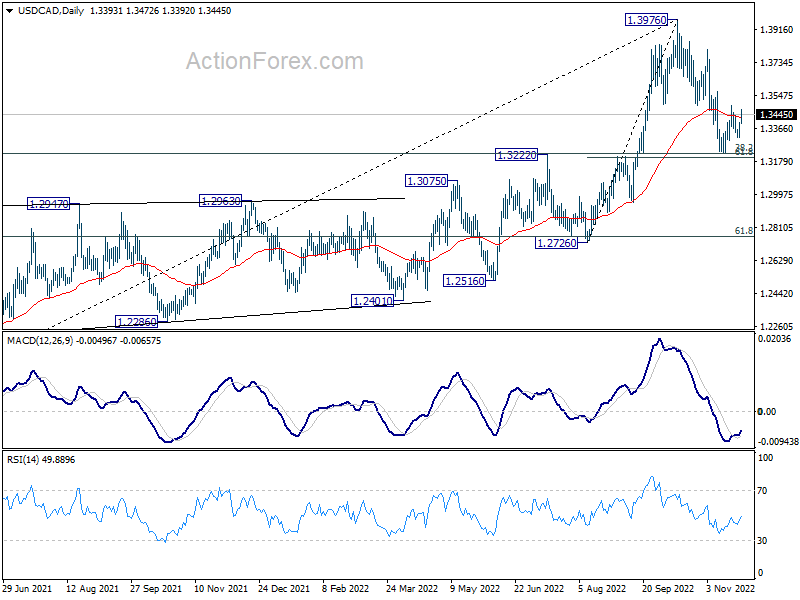

In the bigger picture, as long as 1.3222 cluster support (38.2% retracement of 1.2005 to 1.3976 at 1.3223) holds, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 high at a later stage. However, firm break of 1.3222/3 will indicate that the trend might have reversed. Deeper fall would be seen to next cluster support at 1.2726 (61.8% retracement at 1.2758).

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Retail Sales M/M Oct | -0.20% | 0.50% | 0.60% | |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Oct | 6.50% | 6.30% | ||

| 13:30 | CAD | Current Account (CAD) Q3 | -4.0B | 2.7B |