Risk sentiment improved slightly earlier in Asian session on rumors that China is going to exit its zero-Covid policy earlier. Yet the announcement of the National Health Commission on speeding up vaccination for the elderly was a big let-down. After all, Dollar, and Swiss Franc are on the softer side today so far, with Euro. New Zealand, Australian and Canadian Dollar are on the firmer side. Sterling and Yen are mixed. Focuses will partly stay on unrest in China, and partly back on economic data and comments from central bankers.

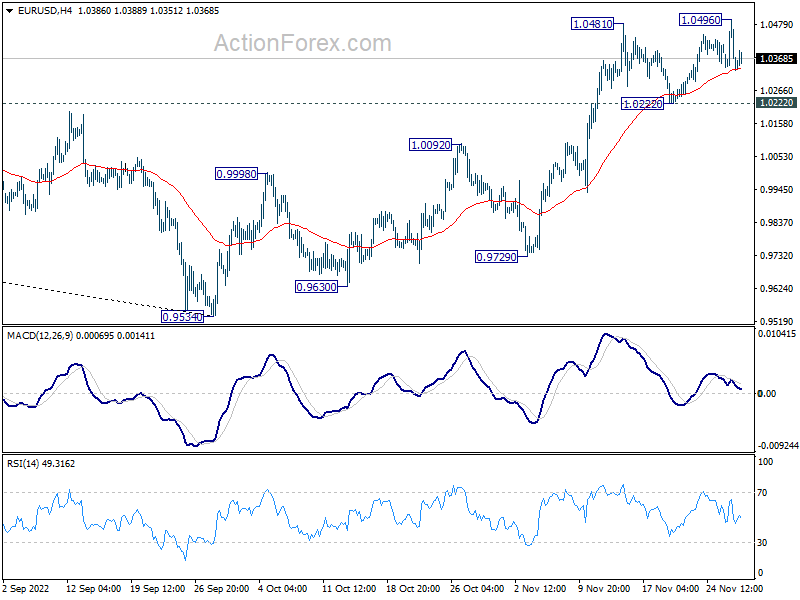

Technically, EUR/USD’s rally overnight was cut short, reflecting much indecisiveness in the markets. There could be some more volatility ahead in the week with Eurozone inflation and US employment data featured. But after all, near term outlook will stay mildly bullish as long as 1.0222 support holds and rise from 0.9534 should resume sooner or later. However, break of 1.0222 will complete a double top pattern (based on current structure 1.0481 and 1.0496), and indicate near term bearish reversal.

{kind=link}

In Asia, Nikkei dropped -0.48%. Hong Kong HSI is up 3.79%. China Shanghai SSE is up 2.31%. Singapore Strait Times is up 1.00%. Japan 10-year JGB yield is down -0.001 at 0.257. Overnight, DOW dropped -1.45%. S&P 500 dropped -1.54%. NASDAQ dropped -1.58%. 10-year yield rose 0.012 to 3.703.

Fed Barkin supportive of slower, but probably longer and potentially high tightening

Richmond Fed President Thomas Barkin said in an interview yesterday, “I’m very supportive of a (tightening) path that is slower, probably longer and potentially higher than where we were before.”

“It is helpful to be somewhat more cautious as you are in restrictive territory,” he said. “It is a better risk-management approach.”

“Inflation has been stubborner than I would like,” he said. “As long as inflation stays elevated, that makes the case to me that we need to do more.”

Fed Bullard: Strong labor market gives us license to pursue disinflationary strategy

St. Louis Fed President James Bullard reiterated yesterday that interest rate has to be raised to at least 5.00-5.25%, from the current 3.75-4.00%, to be “sufficiently restrictive” to curb inflation. The interest rate will have to stay at that level “all during 2023 and into 2024”.

But regarding the size of the next hike in December, Bullard said he would leave the exact tactics to Chair Jerome Powell. “In macroeconomic terms I’m not sure it matters that much at exactly which date we get there or what meeting we get there (the terminal rate)”, he said. “Generally speaking I have advocated that sooner is better, that you do want to get to the right level of the policy rate for the current data and the current situation, but I would defer to the chair as to how he wants to play the tactics on this.”

“I do think that the fact that the labor market is so strong gives us license to pursue our disinflationary strategy now and try to get the inflation under control right now so we don’t replay the 1970s where the FOMC at that time took 15 years to get inflation under control,” Bullard noted.

Fed Williams: Restrictive policy to continue through at least next year

New York Fed President John Williams said yesterday, “Inflation is far too high, and persistently high inflation undermines the ability of our economy to perform at its full potential… There is still more work to do.”

“I do think we’re going to need to keep restrictive policy in place for some time; I would expect that to continue through at least next year,” he added.

Nevertheless, “at some point, nominal interest rates will need to come down. Otherwise real interest rates will be going up and that would just be tightening policy further and further in terms of its effects on the economy… I do see a point, probably in 2024, that we’ll start bringing down nominal interest rates because inflation is coming down and we would want to have real interest rates appropriately positioned.”

NZIER: RBNZ rate to peak at 5% next year

In the November Monetary Policy Statement, RBNZ projected that interest rate would peak at 5.5% while the economy would start contracting in Q2 2023 until Q1 2024.

NZIER said it expected the negative impact of higher interest rates on demand will “become more apparent around mid-2023”. With that, RBNZ “will not need to increase interest rates by as much as it currently expects to”.

“Nonetheless, we expect further increases in the OCR and for it to peak at 5 percent over the coming year,” NZIER added.

Looking ahead

Swiss GDP will be released in European session. UK will release M4 money supply and mortgage approvals. Eurozone will release economic sentiment indicator. Germany will publish CPI flash. Later in the day, Canada will release GDP. US will release consumer confidence and house price index.

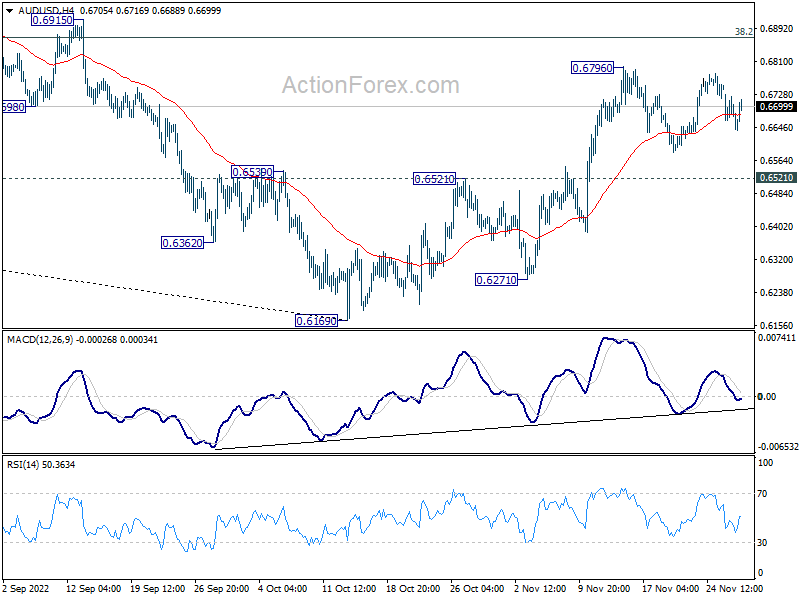

AUD/USD Daily Report

Daily Pivots: (S1) 0.6620; (P) 0.6675; (R1) 0.6708; More…

Range trading continues in AUD/USD and intraday bias stays neutral at this point. Further rise is expected as long as 0.6521 resistance turned support holds. On the upside, break of 0.6796 will resume the rise from 0.6169 to 0.6871 fibonacci level. However, sustained break of 0.6521 will argue that whole rebound from 0.6169 is over, and bring deeper fall to retest this low.

{kind=link}

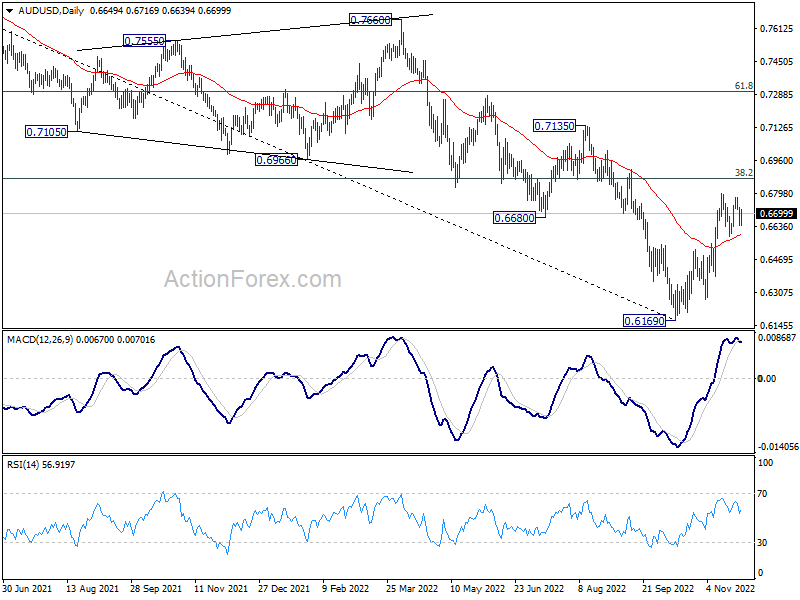

In the bigger picture, a medium term bottom is in place at 0.6160 already. But it’s too early to call for trend reversal. Nevertheless, even as a corrective move, rise from 0.6169 should target 38.2% retracement of 0.8006 to 0.6169 at 0.6871. Sustained trading above 55 week EMA (now at 0.6927) will raise the chance of the start of a bullish up trend. This will now remain the favored case as long as 0.6521 resistance turned support holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Unemployment Rate Oct | 2.60% | 2.60% | 2.60% | |

| 23:50 | JPY | Retail Trade Y/Y Oct | 4.30% | 5.00% | 4.50% | 4.80% |

| 08:00 | CHF | GDP Q/Q Q3 | 0.20% | 0.30% | ||

| 09:30 | GBP | M4 Money Supply M/M Oct | 0.80% | 2.10% | ||

| 09:30 | GBP | Mortgage Approvals Oct | 60K | 67K | ||

| 10:00 | EUR | Eurozone Economic Sentiment Nov | 93 | 92.5 | ||

| 10:00 | EUR | Eurozone Industrial Confidence Nov | -0.8 | -1.2 | ||

| 10:00 | EUR | Eurozone Services Sentiment Nov | 3.4 | 1.8 | ||

| 10:00 | EUR | Eurozone Consumer Confidence Nov F | -23.9 | -23.9 | ||

| 13:00 | EUR | Germany CPI M/M Nov P | 2.00% | 0.90% | ||

| 13:00 | EUR | Germany CPI Y/Y Nov P | 10.90% | 10.40% | ||

| 13:30 | CAD | GDP M/M Sep | 0.20% | 0.10% | ||

| 14:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Sep | 10.70% | 13.10% | ||

| 14:00 | USD | Housing Price Index M/M Sep | -1.20% | -0.70% | ||

| 15:00 | USD | Consumer Confidence Nov | 100 | 102.5 |