Canadian Dollar falls broadly after weaker than expected GDP data. Dollar and Swiss Franc are also weak on steady market sentiment. Australia and New Zealand Dollar are currently the strongest ones, followed by Sterling. But all three are just staying in range against the greenback. Euro is also relatively directionless with mixed trading with Yen together.

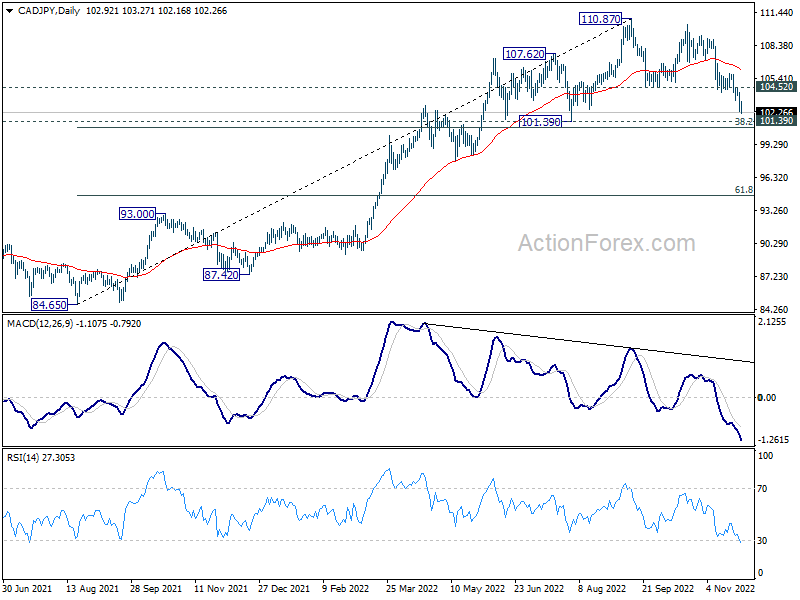

Technically, CAD/JPY is extending the fall from 110.87. Such decline is seen as a correction to the up move from 84.65. Downside could be contained by 101.39 support zone (38.2% retracement of 84.65 to 110.87 at 100.85) to bring rebound, at least on first attempt. But overall, further fall will remain in favor as long as 104.52 minor resistance holds.

{kind=link}

In Europe, at the time of writing, FTSE is up 0.67%. DAX is up 0.05%. CAC is up 0.18%. Germany 10-year yield is down -0.053 at 1.943. Earlier in Asia, Nikkei dropped -0.48%. Hong Kong HSI rose 5.24%. China Shanghai SSE rose 2.31%. Singapore Strait Times rose 1.12%. Japan 10-year JGB yield dropped -0.038 to 0.254.

Canada GDP grew 0.1% mom in Sep, to be unchanged in Oct

Canada GDP rose 0.1% mom in September, below expectation of 0.2% mom. Goods-producing industries grew 0.3% while services-producing industries were essentially unchanged.

Advance information indicates that real GDP was unchanged in October. Increases in the public, transportation and warehousing, construction and wholesale trade sectors were offset by decreases in the manufacturing and mining, quarrying and oil and gas extraction sectors.

BoE Mann: Medium-term inflation expectation important for next rate vote

BoE MPC member Catherine Mann said at an online event, “looking at medium-term expectations is a very important ingredient to my assessment of what the appropriate Bank Rate at the next vote might be.”

“Once inflation expectations have been managed, the bank rate can come off a future peak,” she added. At the same time, foreign exchange rate is also an “important ingredient” for inflation in the UK.

Eurozone economic sentiment rose to 93.7 in Nov, first increase since Feb

Eurozone Economic Sentiment Indicator rose from 92.7 to 93.7 in November, the first increase since February. Industrial confidence dropped from -1.2 to -2.0. Services confidence rose from 2.1 to 2.3. Consumer confidence rose from -27.5 to -23.9. Retail trade confidence was unchanged at -6.7. Construction confidence dropped from 2.6 to 2.3. Employment Expectation Indicator rose from 105.4 to 107.4. Economic Uncertainty Indicator dropped from 30.7 to 28.4.

EU ESI rose from 91.2 to 92.2. Amongst the largest EU economies, the ESI increased strongly in Italy (+4.1) and, to a lesser extent, the Netherlands (+1.2) and Germany (+1.1), while it eased in Spain (-1.7) and France (-1.6). Sentiment in Poland stayed broadly flat (+0.3). EEI rose from 104.9 to 106.3. EUI dropped from 29.8 to 27.8.

Swiss GDP grew 0.2% qoq in Q3

Swiss GDP grew 0.2% qoq in Q3, matched expectations. Looking at some details, manufacturing contracted -0.2%. Construction dropped -2.2%. Finance and insurance dropped -2.1%. But trade expanded 2.3% while accommodation and food rose 2.8%.

By expenditure approach, private consumption grew 0.7%. Equipment and software investment rose 2.1%. Exports excluding valuables rose 7.89%. But construction investment dropped -2.0%.

NZIER: RBNZ rate to peak at 5% next year

In the November Monetary Policy Statement, RBNZ projected that interest rate would peak at 5.5% while the economy would start contracting in Q2 2023 until Q1 2024.

NZIER said it expected the negative impact of higher interest rates on demand will “become more apparent around mid-2023”. With that, RBNZ “will not need to increase interest rates by as much as it currently expects to”.

“Nonetheless, we expect further increases in the OCR and for it to peak at 5 percent over the coming year,” NZIER added.

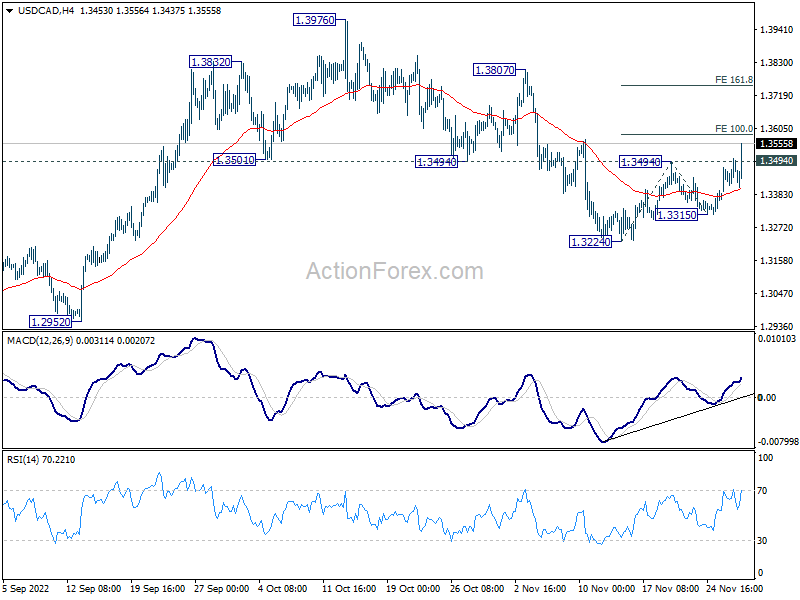

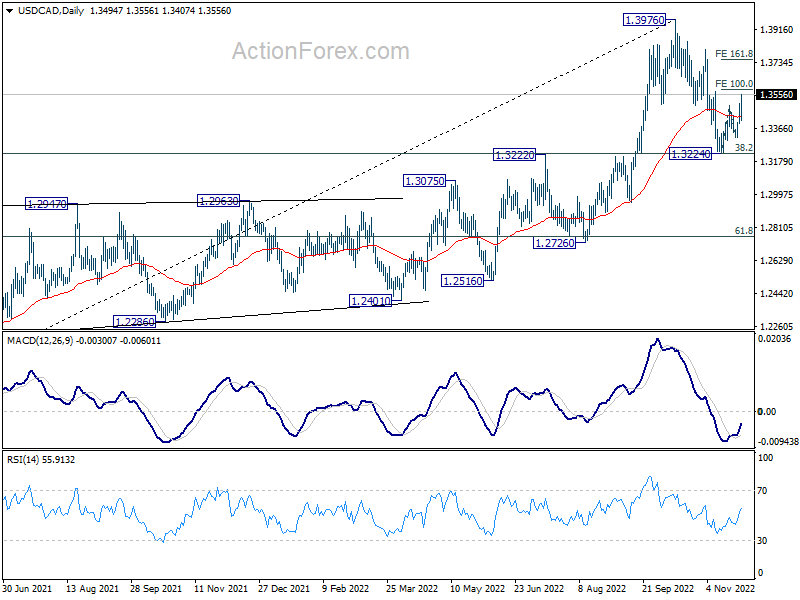

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3420; (P) 1.3462; (R1) 1.3539; More….

USD/CAD’s rise from 1.3224 resumed by breaking through 1.3494 resistance finally. The development adds to the case that correction from 1.3976 has completed at 1.3224. Intraday bias is now back on the upside. Further break of 100% projection of 1.3224 to 1.3494 from 1.3315 at 1.3585 should prompt upside acceleration to 161.8% projection at 1.3752. This will now remain the favored case as long as 1.3315 support holds, in case of retreat.

{kind=link}

In the bigger picture, as long as 1.3222 cluster support (38.2% retracement of 1.2005 to 1.3976 at 1.3223) holds, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 high at a later stage. However, firm break of 1.3222/3 will indicate that the trend might have reversed. Deeper fall would be seen to next cluster support at 1.2726 (61.8% retracement at 1.2758).

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Unemployment Rate Oct | 2.60% | 2.60% | 2.60% | |

| 23:50 | JPY | Retail Trade Y/Y Oct | 4.30% | 5.00% | 4.50% | 4.80% |

| 08:00 | CHF | GDP Q/Q Q3 | 0.20% | 0.20% | 0.30% | 0.10% |

| 09:30 | GBP | M4 Money Supply M/M Oct | 0.00% | 0.80% | 2.10% | |

| 09:30 | GBP | Mortgage Approvals Oct | 59K | 60K | 67K | |

| 10:00 | EUR | Eurozone Economic Sentiment Nov | 93.7 | 93 | 92.5 | 92.7 |

| 10:00 | EUR | Eurozone Industrial Confidence Nov | -2 | -0.8 | -1.2 | |

| 10:00 | EUR | Eurozone Services Sentiment Nov | 2.3 | 3.4 | 1.8 | |

| 10:00 | EUR | Eurozone Consumer Confidence Nov F | -23.9 | -23.9 | -23.9 | |

| 13:00 | EUR | Germany CPI M/M Nov P | -0.50% | 2.00% | 0.90% | |

| 13:00 | EUR | Germany CPI Y/Y Nov P | 10.00% | 10.90% | 10.40% | |

| 13:30 | CAD | GDP M/M Sep | 0.10% | 0.20% | 0.10% | |

| 14:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Sep | 10.70% | 13.10% | ||

| 14:00 | USD | Housing Price Index M/M Sep | -1.20% | -0.70% | ||

| 15:00 | USD | Consumer Confidence Nov | 100 | 102.5 |