Sterling surges broadly today, shrugging off PMI data which indicates extended weakness in the economy. It’s even over-powering New Zealand Dollar, which was lifted by RBNZ’s jumbo rate hike. On the other hand, selling is focusing on Dollar, Canadian and Australia, while Yen is also on the weak side. Euro is mixed, and it’s clearly lagging behind both the Pound and Swiss Franc.

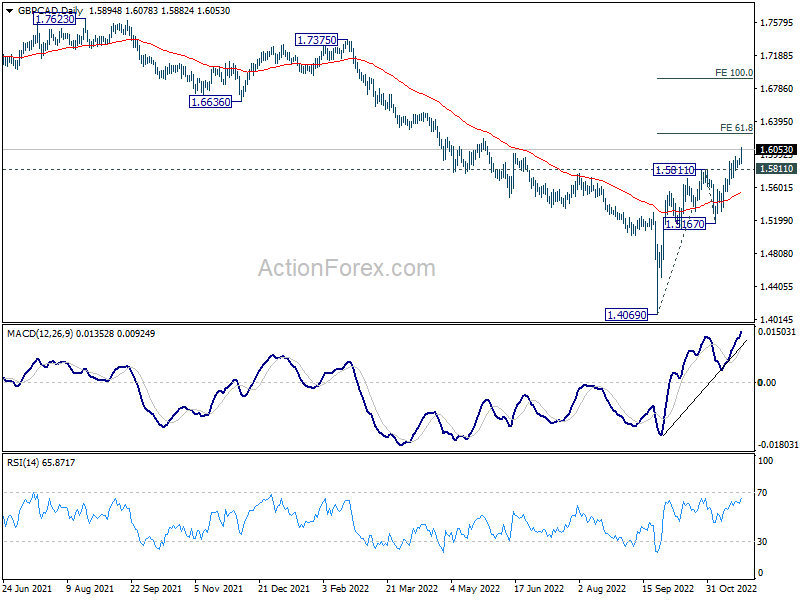

Technically, GBP/CAD is extending the rise from 1.4069 low, and further rally is expected as long as 1.5811 resistance turned support holds. Next target is 61.8% projection of 1.4069 to 1.5811 from 1.5167 at 1.6244. Decisive break there could prompt upside acceleration to 100% projection at 1.6909, and solidify the momentum for a medium term up trend, rather than a corrective rebound.

{kind=link}

In Europe, at the time of writing, FTSE is up 0.06%. DAX is down -0.31%. CAC is down -0.12%. Germany 10-year yield is down -0.003 at 1.982. Earlier in Asia, Japan was on holiday, Hong Kong HSI rose 0.57%. China Shanghai SSE rose 0.26% Singapore Strait Times dropped -0.11%.

US durable goods orders rose 1.0% mom in Oct, ex-transport orders up 0.5% mom

US durable goods orders rose 1.0% mom to USD 277.4B in October, above expectation of 0.4% mom. New orders were up seven of the last eight months. Ex-transport orders rose 0.5% mom to USD 179.6B, above expectation of 0.1% mom. Ex-defense orders rose 0.8 mom to USD 260.8B. Transportation equipment, up six of the last seven months, rose 2.1% mom to USD 97.8B.

US initial jobless claims rose to 240k, above expectation

US initial jobless claims rose 17k to 240k in the week ending November 19, above expectation of 224k. Four-week moving average of initial claims rose 4.4k to 227k.

Continuing claims rose 48k to 1551k in the week ending November 12. Four-week moving average of continuing claims rose 28k to 1510k.

Bundesbank: Inflation rate in double digits beyond turn of the year

In the monthly report, Bundesbank said “all in all, despite the higher than expected economic activity in the summer quarter, a recession in the German economy is to be expected in the winter half-year.” Downward forces should “clearly predominate in the coming months”. Weaker global economy will weigh on exports while high inflation is dampening private consumption.

“The inflation rate could remain in the double digits beyond the turn of the year,” it noted. There is still strong cost pressure, especially for industrial products on the upstream stages. Energy prices have recently been declining but are still at a very high level. Passing of raw material prices is not yet complete.

ECB de Guindos: We will continue to raise interest rates

ECB Vice-President Luis de Guindos said at a finance event, “we will continue to raise interest rates to a level that allows us to ensure that inflation converges towards our definition of price stability.”

“It is very important to look at the evolution of underlying inflation and possible second round effects because they will determine the response of monetary policy,” De Guindos said.

While he expect inflation to slow in Q1 or H1 of next year, “we also believe core inflation will be high in coming months.” Also, he noted, “it is very possible that in the fourth quarter and the first quarter of next year we will have negative growth rates.”

Eurozone PMI composite ticked up to 47.8, consistent with -0.2% GDP contraction in Q4

Eurozone PMI Manufacturing rose from 46.4 to 47.3 in November. PMI Services was unchanged at 48.6. PMI Composite rose from 47.3 to 47.8.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

“A further fall in business activity in November adds to the chances of the eurozone economy slipping into recession. So far, the data for the fourth quarter are consistent with GDP contracting at a quarterly rate of just over 0.2%.

“However, the November PMI data also bring some tentative good news. In particular, the overall rate of decline has eased compared to October. Most encouragingly, supply constraints are showing signs of easing, with supplier performance even improving in the region’s manufacturing heartland of Germany. Warm weather has also allayed some of the fears over energy shortages in the winter months.

“Price pressures, the recent surge of which has prompted further policy tightening from the ECB, are also now showing signs of cooling, most noticeably in the manufacturing sector. Not only should this help contain the cost of living crisis to some extent, but the brighter inflation outlook should take some pressure off the need for further aggressive policy tightening.

“However, it’s clear that manufacturing remains in a worryingly severe downturn, and service sector activity is also still under intense pressure, both largely as a result of the cost of living crisis and recent tightening of financial conditions. A recession therefore looks likely, though the latest data provide hope that the scale of the downturn may not be as severe as previously feared.”

Germany PMI Manufacturing improved from 45.1 o 46.7 in November. PMI Services dropped from 46.5 to 46.4. PMI Composite also recovered slightly from 45.1 to 46.4.

France PMI Manufacturing improved from 47.2 to 49.1 in November. But PMI Services dropped from 51.7 to 49.4, a 20-month low. PMI Composite dropped from 50.2 to 48.8, a 21-month low.

UK PMI composite ticked up to 48.3, downturn will deepen into new year

UK PMI Manufacturing was unchanged at 46.2 in November. PMI services was also unchanged at 48.8. PMI Composite ticked up from 48.2 to 48.3.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

“A further steep fall in business activity in November adds to growing signs that the UK is in recession, with GDP likely to fall for a second consecutive quarter in the closing months of 2022.

“If pandemic lockdown months are excluded, the PMI for the fourth quarter so far is signalling the steepest economic contraction since the height of the global financial crisis in the first quarter of 2009, consistent with the economy contracting at a quarterly rate of 0.4%. ”

Forward-looking indicators, notably an increasingly steep drop in demand for goods and services, suggest the downturn will deepen as we head into the new year.”

RBNZ hikes 75bps to 4.25%, tightening not finished

RBNZ raises the Official Cash Rate by a record 75bps to 4.25% as widely expected. The central bank maintained that “monetary conditions needed to continue to tighten further, so as to be confident there is sufficient restraint on spending to bring inflation back within its 1-3 percent per annum target range.”

During the meeting, increases of 50, 75 and 100bps were considered. But members agreed that “a larger increase in the OCR was appropriate, given the resilience of domestic spending, and the higher and more persistent actual and expected inflation outcomes.”

But on the “balances of risks”, a 75bps hike was “appropriate at this meeting”. Members highlights that “the cumulative tightening of monetary conditions delivered to date continues to pass through to the economy via the lagged transmission to effective retail interest rates.”

In the new forecasts, annual inflation is projected to rise further to 7.5% in Q4 and Q1, then stay above 5% throughout 2023. Inflation would then slowly drop back to 2.9% in Q3, 2024. Quarterly GDP is projected to contract from Q2 2023 to Q1 2024, turn flat in Q2 and Q3 2024, before returning to slight growth. OCR will continue to rise and peak at 5.5% in Q3 2023, before turning down in second half of 2024.

Australia PMI composite dropped to 47.7, deteriorating demand and worsening price pressures

Australia PMI Manufacturing dropped from 52.7 to 51.5 in November, a 29-month low. PMI Services dropped from 49.3 to 47.2, a 10-month low. PMI Composite also dropped from 49.8 to 47.7, a 10-month low.

Jingyi Pan, Economics Associate Director at S&P Global Market Intelligence said:

“The latest S&P Global Flash Australia Composite PMI data revealed that the private sector economy further contracted midway into the fourth quarter, faced with deteriorating demand conditions. In particular, the service sector continued to be affected by higher interest rates and capacity constraints, leading to a sharper fall in business activity.

“That said, with price inflation further climbing in November, the pressure remains on the central bank to keep tightening monetary policy to rein in prices. This is also amid indications of solid employment growth from the PMI data.

“The mix of deteriorating demand and worsening price pressures does not bode well for the near-term outlook, and this has also been reinforced by the decline in private sector confidence in November.”

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1834; (P) 1.1869; (R1) 1.1919; More…

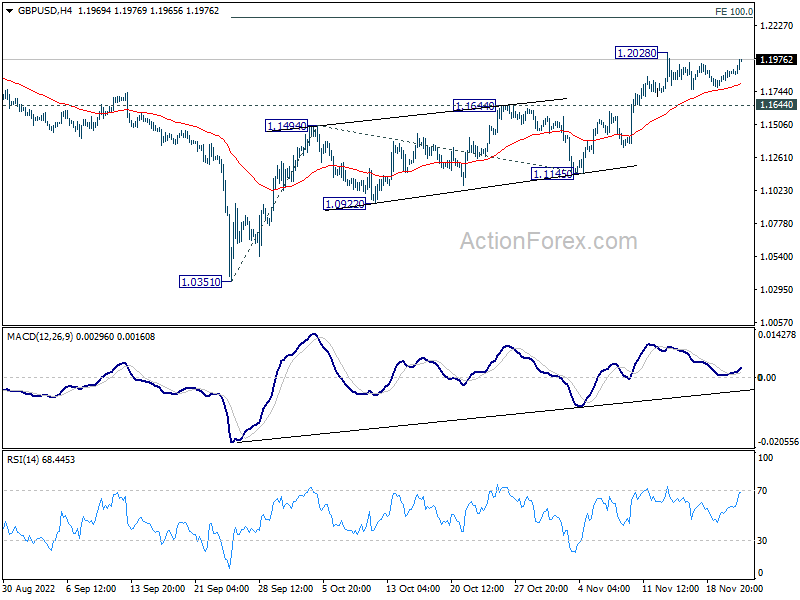

GBP/USD rises notably today but stays below 1.2028 resistance. Intraday bias remains neutral first. But overall, further rally is expected as long as 1.1644 resistance turned support holds. On the upside, break of 1.2028 will resume whole rise from 1.0351 to 100% projection of 1.0351 to 1.1494 from 1.1145 at 1.2288. However, sustained break of 1.1644 will bring deeper fall to 1.1145 support instead.

{kind=link}

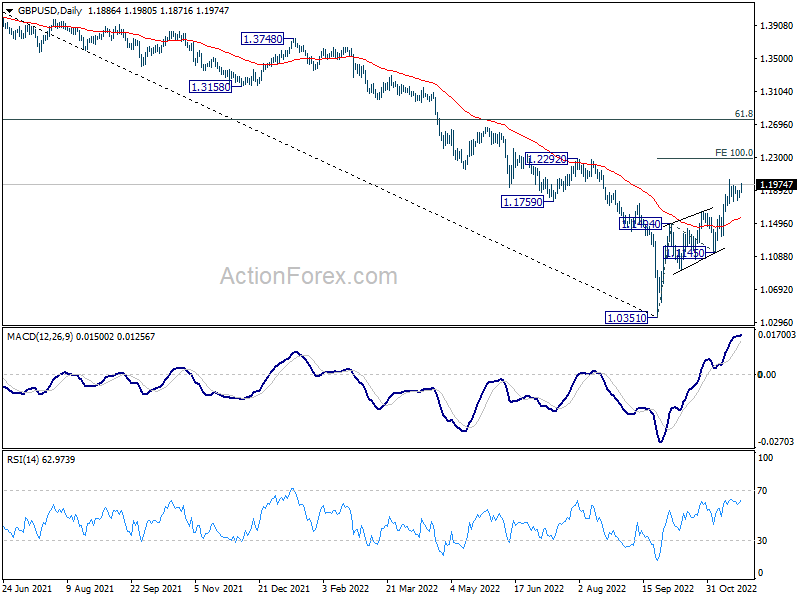

In the bigger picture, rise from 1.0351 medium term bottom is at least correcting whole down trend from 1.4248 (2021 high). Further rise is expected as long as 1.1145 support holds. Next target is 61.8% retracement of 1.4248 to 1.0351 at 1.2759.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:00 | AUD | Manufacturing PMI Nov P | 51.5 | 52.7 | ||

| 22:00 | AUD | Services PMI Nov P | 47.2 | 49.3 | ||

| 01:00 | NZD | RBNZ Rate Decision | 4.25% | 4.25% | 3.50% | |

| 08:15 | EUR | France Manufacturing PMI Nov P | 49.1 | 47 | 47.2 | |

| 08:15 | EUR | France Services PMI Nov P | 49.4 | 50.6 | 51.7 | |

| 08:30 | EUR | Germany Manufacturing PMI Nov P | 46.7 | 45.2 | 45.1 | |

| 08:30 | EUR | Germany Services PMI Nov P | 46.4 | 46.4 | 46.5 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Nov P | 47.3 | 46.5 | 46.4 | |

| 09:00 | EUR | Eurozone Services PMI Nov P | 48.6 | 48.4 | 48.6 | |

| 09:30 | GBP | Manufacturing PMI Nov P | 46.2 | 45.6 | 46.2 | |

| 09:30 | GBP | Services PMI Nov P | 48.8 | 48 | 48.8 | |

| 13:30 | USD | Initial Jobless Claims (Nov 18) | 240K | 224K | 222K | 223K |

| 13:30 | USD | Durable Goods Orders Oct | 1.00% | 0.40% | 0.40% | 0.30% |

| 13:30 | USD | Durable Goods Orders ex Transportation Oct | 0.50% | 0.10% | -0.50% | -0.90% |

| 14:45 | USD | Manufacturing PMI Nov P | 49.8 | 50.4 | ||

| 14:45 | USD | Services PMI Nov P | 47.7 | 47.8 | ||

| 15:00 | USD | Michigan Consumer Sentiment Nov F | 54.7 | 54.7 | ||

| 15:00 | USD | New Home Sales Oct | 575K | 603K | ||

| 15:30 | USD | Crude Oil Inventories | -2.6M | -5.4M | ||

| 17:00 | USD | Natural Gas Storage | 86B | 64B | ||

| 19:00 | USD | FOMC Meeting Minutes |