Dollar’s rebound stalled once again quickly, as risk markets appear to have stabilized. Overall, Swiss Franc is following the greenback as the second strongest for the week so far, then Canadian. Yen is the worst performer, followed by Aussie and Kiwi. Euro and Sterling are mixed with Sterling having an upper hand. Canadian retail sales will be a feature of the day while many central bankers will speak. Hopefully, there would be some more decisive market actions.

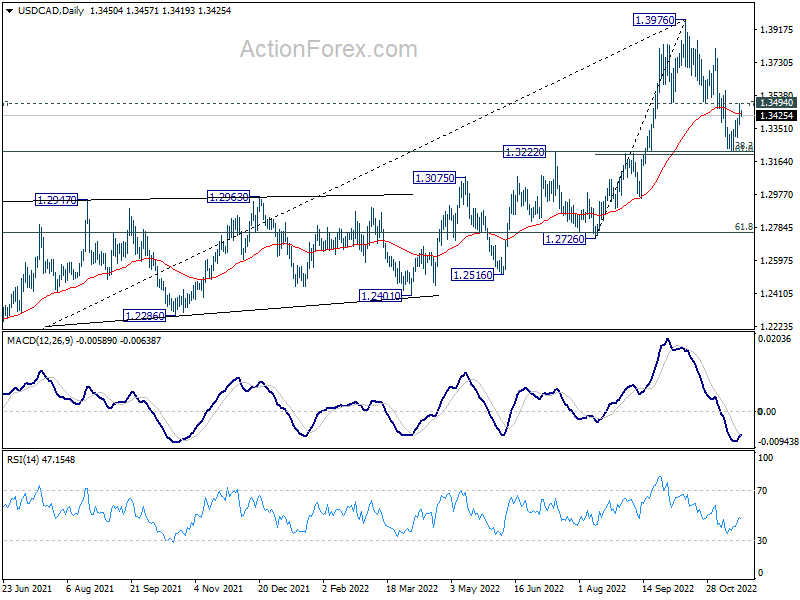

Technically, USD/CAD is now pressing 1.3494 support turned resistance. Decisive break there will indicate that correction from 1.3976 has completed with three waves down to 1.3224. More important, that would be successful defense of 1.3222 key resistance turned support, and reinforce medium term bullishness. In this case, there’s prospect of retesting 1.3976 high next.

{kind=link}

In Asia, at the time of writing, Nikkei is up 0.70%. Hong Kong HSI is down -0.39%. China Shanghai SSE is up 0.75%. Singapore Strait Times is up 0.51%. Japan 10-year JGB yield is up 0.0007 at 0.246. Overnight, DOW dropped -0.13%. S&P 500 dropped -0.39%. NASDAQ dropped -1.09%. 10-year yield rose 0.007 to 3.825.

Fed Mester: Makes sense that we can slow down a bit

Cleveland Fed President Loretta Mester said yesterday, “we’re at a point where we’re going to enter a restrictive stance of policy. At that point, I think it makes sense that we can slow down a bit the … pace of increases.”

“We’re still going to raise the funds rate, but we’re at a reasonable point now where we can be very deliberate in setting monetary policy,” she added.

“I think we can slow down from the 75 at the next meeting. I don’t have a problem with that, I do think that’s very appropriate,” Mester said. “But I do think we’re going to have to let the economy tell us going forward what pace we have to be at.”

“Right now my forecast is that we’re going to see some real, good progress on inflation next year,” Mester said. “We won’t be back to 2%, but we’ll see some meaningful progress next year. But if we don’t see that, then we’re going to have to make sure our policy really reacts to the incoming information. So I can’t tell you today what the path going forward will be.”

Fed Daly: Premature to take anything off the table

San Francisco Fed President Mary Daly said yesterday that “it’s premature in my mind to take anything off the table”, regarding the size of rate hike in December. She added. “I’m going into the meeting with the full range of adjustments that we could make on the table.

Daly also said recent CPI data was “way too early to cause a turning point on inflation… One month does not a victory make. It doesn’t give me comfort. We will need more good months of data before call this a turning point.”

“As we work to bring policy to a sufficiently restrictive stance — the level required to bring inflation down and restore price stability — we will need to be mindful,” Daly also said. “Adjusting too little will leave inflation too high. Adjusting too much could lead to an unnecessarily painful downturn.”

ECB Centeno: Many conditions in place for less than 75bps hike

ECB Governing Council member Mario Centeno was asked yesterday about whether the central bank should hike by less that 75bps in December. He said, “I think there are conditions in place — many conditions — for the increase to be less than that number”.

Centeno also noted that “rates in Europe continue to be roughly half those in the United States”, and that’s a good indicator of the difference between the economic fundamentals of the two regions. He also urged restraint in wage growth and company margins as that “could help the ECB a lot in combating inflation”.

NZ goods exports rose 14% yoy in Oct, imports surged 24% yoy

New Zealand goods exports rose 14% yoy to NZD 6.1B in October. Goods imports rose 24% yoy to NZD 8.3B. Trade deficit widened from NZD -1.7B to NZD -2.1B, much larger than expectation of NZD -1.7B.

Annual goods expects, comparing with the year ended October 2021, rose 14% to NZD 71.1B. Annual goods imports rose 25% to NZD 84.0B. Annual trade deficit swelled to fresh record of NZD -12.9B, comparing to NZD -4.9B a year ago.

Looking ahead

UK public sector net borrowing and Eurozone current account will be released in European session. Later in the day, Canada retail sales will take center stage, while new housing price index will also be published.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.1766; (P) 1.1837; (R1) 1.1895; More…

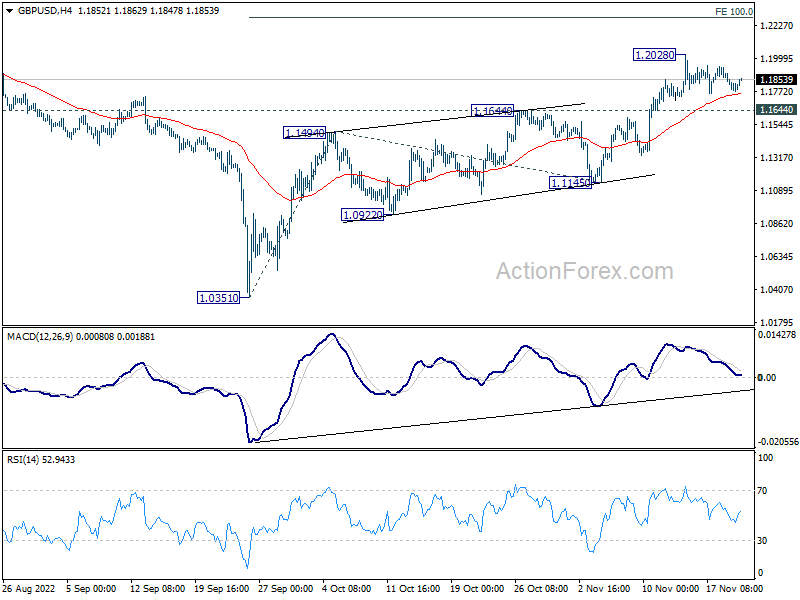

GBP/USD is staying inside tight range below 1.2028 as sideway consolidation continues. Intraday bias remains neutral first, and further rally is expected as long as 1.1644 resistance turned support holds. On the upside, break of 1.2028 will resume whole rise from 1.0351 to 100% projection of 1.0351 to 1.1494 from 1.1145 at 1.2288. However, sustained break of 1.1644 will bring deeper fall to 1.1145 support instead.

{kind=link}

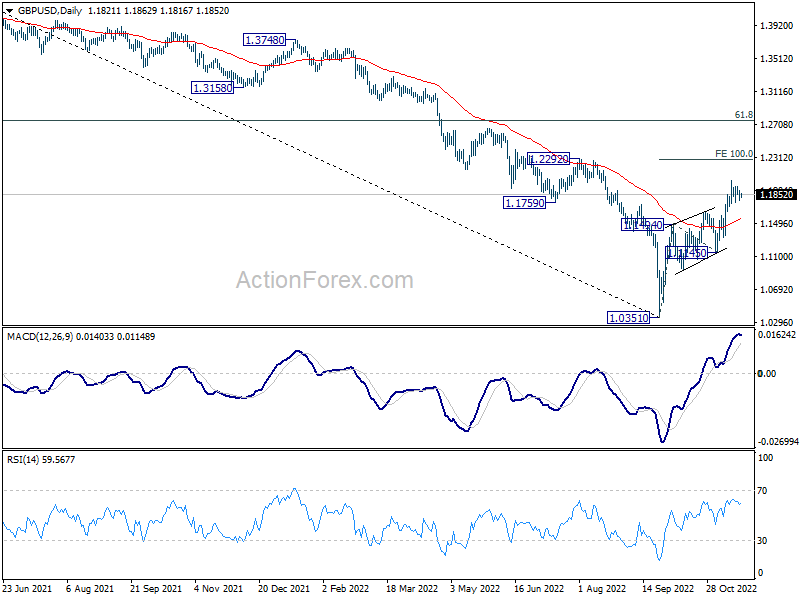

In the bigger picture, rise from 1.0351 medium term bottom is at least correcting whole down trend from 1.4248 (2021 high). Further rise is expected as long as 1.1145 support holds. Next target is 61.8% retracement of 1.4248 to 1.0351 at 1.2759.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Oct | -2129M | -1715M | -1615M | -1696M |

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Oct | 19.2B | |||

| 09:00 | EUR | Eurozone Current Account (EUR) Sep | -20.3B | -26.3B | ||

| 13:30 | CAD | New Housing Price Index M/M Oct | 0.20% | -0.10% | ||

| 13:30 | CAD | Retail Sales M/M Sep | 1.10% | 0.70% | ||

| 13:30 | CAD | Retail Sales ex Autos M/M Sep | 1.00% | 0.70% | ||

| 15:00 | EUR | Eurozone Consumer Confidence Nov P | -26 | -28 |