Dollar dives sharply in early US session after lower than expected CPI readings. CPI might have really started to turn around, and that would support Fed to start slowing the pace of tightening. For now, Sterling, Aussie and Yen are the strongest ones while Swiss Franc and Euro are lagging behind. But it will take some more time to find out whole’s the biggest beneficiary of the Dollar selloff.

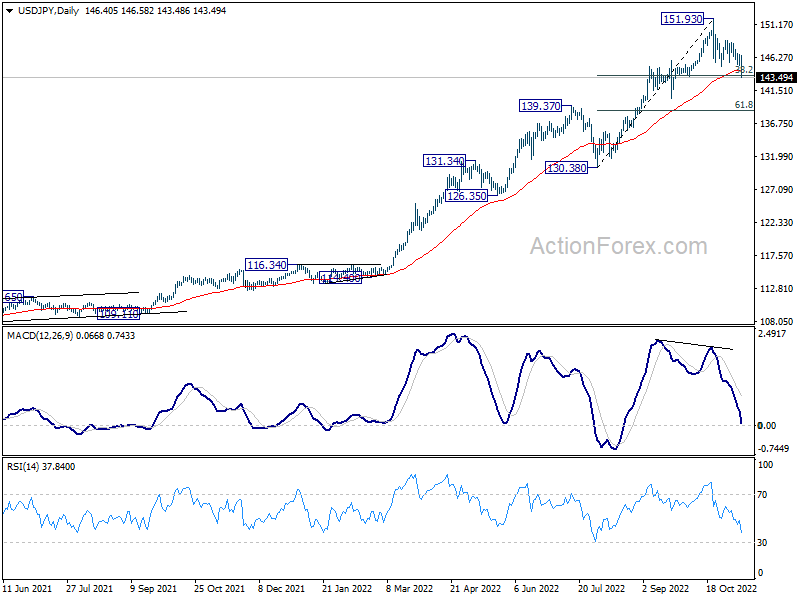

Technically, USD/JPY will be the most interesting one to watch as it’s now pressing 38.2% retracement of 130.38 to 151.93 at 143.69. Sustained break there will argue that fall from 151.93 is not just correcting the rise from 130.38, but also a larger up trend. If that’s true, there is prospect of deeper decline, as a medium term correction, back to 130.38/139.37 support zone.

{kind=link}

In Europe, at the time of writing, FTSE is up 1.15%. DAX is up 2.33%. CAC is up 1.16%. Germany 10-year yield is down -0.167 at 2.004. Earlier in Asia, Nikkei dropped -0.98%. Hong Kong HSI dropped -1.70%. China Shanghai SSE dropped -0.39%. Singapore Strait Times rose 0.24%. Japan 10-year JGB yield is down -0.0128 at 0.246.

US CPI slowed to 7.7% yoy, CPI core slowed to 6.3% yoy, below expectations

US CPI rose 0.4% mom in October, below expectation of 0.7% mom. Core CPI rose 0.3% mom, below expectation of 0.5% mom. Energy rose 1.8% mom while food rose 0.6% mom.

Over the last 12 months, CPI slowed from 8.2% yoy to 7.7% yoy, below expectation of 8.0% yoy. That’s the lowest rate since January this year. Core CPI slowed from 6.6% yoy to 6.3% yoy, below expectation of 6.5% yoy. Energy index was up 17.6% yoy while food was up 10.9% yoy.

US initial jobless claims rose 7k to 225k

US initial jobless claims rose 7k to 225k in the week ending November 5. Four-week moving average of initial claims rose 250 to 218.75k.

Continuing claims rose 6k to 1493k in the week ending October 29. Four-week moving average of continuing claims rose 32k to 1450k.

ECB bulletin: Further weakening of economy into beginning of 2023

In the monthly economic bulletin, ECB said the Governing Council expects a “further weakening” of economic activity “in the remainder of 2022 and the beginning of 2023”.

High inflation continues to “dampen spending and production” and severe disruptions in gas supply “have worsened the situation further”.

Additionally, “worsening terms of trade”, with imports prices rising faster than exports prices, are “weighing on incomes in the euro area”.

Risks to the economic growth outlook are “clearly on the downside, especially in the near term”. Risks to the inflation outlook are “primarily on the upside”.

ECB’s future policy rate decisions will continue to be “data dependent” and follow a “meeting-by-meeting approach”.

BoJ Kuroda: Premature to lay out details of exit strategy

BoJ Governor Haruhiko Kuroda told the parliament, “it’s premature to lay out details of an exit strategy. But one major factor of debate will be the pace of increase in the BoJ’s short-term policy rate, now set at -0.1%.”

“Another factor would be how to adjust its balance sheet,” he said, noting that other major central banks adopted the sequence of interest rate hike first, then shrinking balance sheet.

“It’s extremely important for the BOJ to underpin the economy with ultra-loose monetary policy and ensure the necessary environment is falling into place for companies to hike wages,” Kuroda emphasized.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 0.9975; (P) 1.0031; (R1) 1.0070; More…

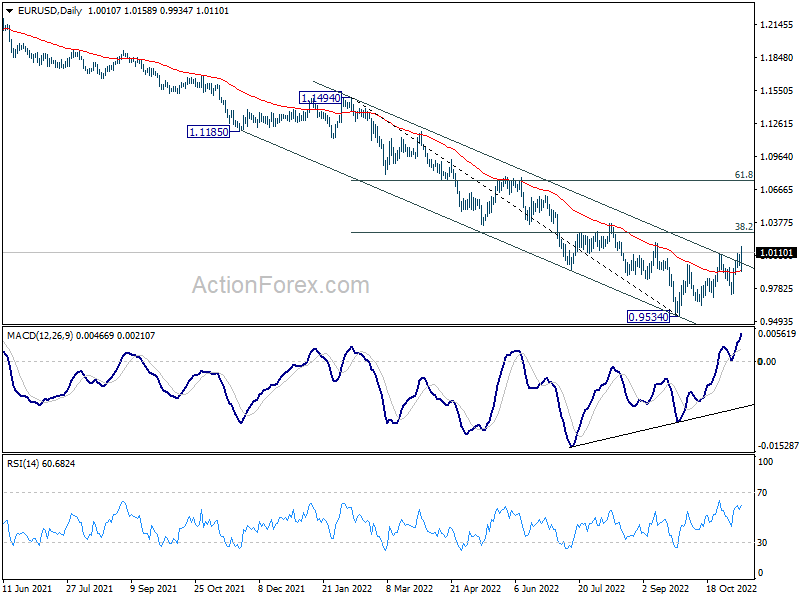

EUR/USD’s break of 1.0092 resistance now confirms resumption of whole rebound from 0.9534. Intraday bias is back on the upside for 38.2% retracement of 1.1494 to 0.9534 at 1.0283, even as a corrective rise. Sustained break there will target 55 week EMA (now at 1.0567). On the downside, break of 0.9934 will dampen the bullish case and turn intraday bias neutral first.

{kind=link}

In the bigger picture, break of the medium term channel resistance, bullish convergence condition in daily MACD, as well as some support from 55 day EMA are bullish signs. A medium term bottom should be in place at 0.9534. Stronger rebound should be seen back towards 55 week EMA (now at 1.0567). It’s still early to conclude that the medium term trend is reversing, at least until sustained break of 55 week EMA.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y Oct | 3.10% | 3.40% | 3.30% | |

| 00:00 | AUD | Consumer Inflation Expectations Nov | 6.00% | 5.40% | ||

| 00:01 | GBP | RICS Housing Price Balance Oct | -2% | 28% | 32% | |

| 09:00 | EUR | Italy Industrial Output M/M Sep | -1.80% | 1.70% | 2.30% | |

| 09:00 | EUR | ECB Economic Bulletin | ||||

| 12:30 | USD | Initial Jobless Claims (Nov 4) | 225K | 221K | 217K | 218K |

| 12:30 | USD | CPI M/M Oct | 0.40% | 0.70% | 0.40% | |

| 12:30 | USD | CPI Y/Y Oct | 7.70% | 8.00% | 8.20% | |

| 12:30 | USD | CPI Core M/M Oct | 0.30% | 0.50% | 0.60% | |

| 12:30 | USD | CPI Core Y/Y Oct | 6.30% | 6.50% | 6.60% | |

| 15:30 | USD | Natural Gas Storage | 92B | 107B |