Asian markets are very mixed today, with Nikkei trading lower, following US stocks overnight. But strong rebound is seen in Hong Kong and China. As a result, Dollar is paring some of the post-FOMC gains while commodity currencies recover. It’s also possible that traders are lighting up their positions ahead of non-farm payroll data form the US. In any case, much volatility is anticipated before the week comes to a close.

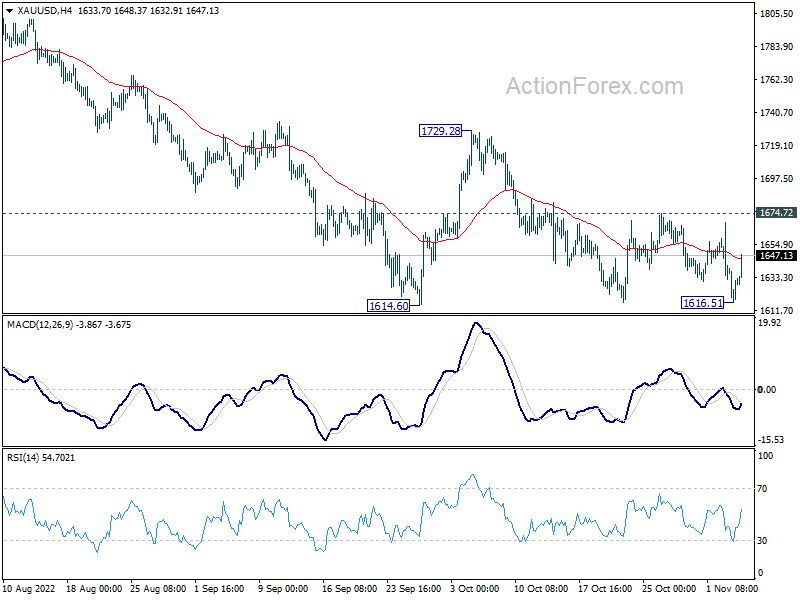

Technically, Gold recovered notably after dipping to 1616.51, ahead of 1614.60 low. On the downside, firm break of 1614.60 will confirm larger down trend resumption. On the upside, break of 1674.72 resistance will delay the bearish case, and extend the consolidation pattern from 1614.60 with another rising leg. Upside should be capped below 1729.28 resistance. Today’s move could be used to confirm the near term direction in Dollar.

{kind=link}

In Asia, at the time of writing, Nikkei is down -1.78%. Hong Kong HSI is up 6.78%. China Shanghai SSE is up 2.47%. Singapore Strait Times is up 0.83%. Japan 10-year JGB yield is up 0.0070 at 0.254. Overnight, DOW dropped -0.46%. S&P 500 dropped -1.06%. NASDAQ dropped -1.73%. 10-year yield rose 0.065 to 4.124.

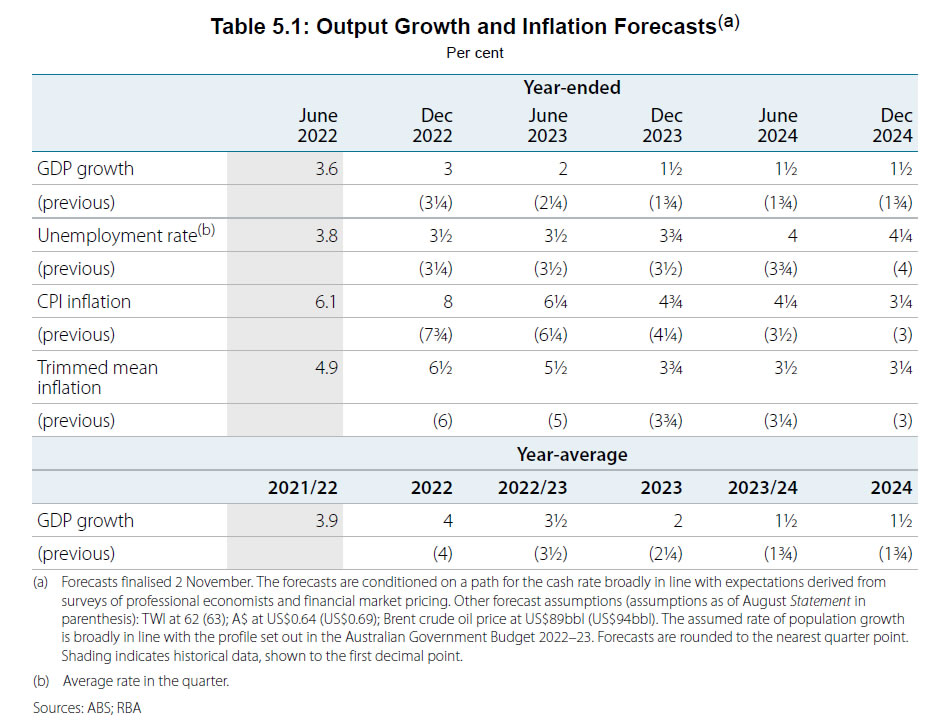

RBA downgrades 2023, 2024 growth forecast, raised inflation

In the Statement on Monetary Policy, RBA noted that after a sequence of 50bps and 24bps rate hikes, “the Board recognised that interest rates had already been increased significantly in a short period of time”.

“In an uncertain environment, slowing the adjustment of policy allows time to assess the effects of the increases to date and the evolving economic outlook,” it added.

The Board expects that “interest rates will need to increase further”, but “monetary policy is not on a pre-set path”. The size and timing of future interest rate hikes will be determined by incoming data and assessment of the outlook of inflation and labor market.

In the new economic projections, year-average GDP growth forecast for:

- 2022 was left unchanged at 4%.

- 2023 was downgraded from 2.25% to 2.00%.

- 2024 was downgraded from 1.75% to 1.50%.

Year-end forecasts for headline CPI for:

- 2022 was revised up from 7.75% to 8.00%.

- 2023 was revised up from 4.25% to 4.75%.

- 2024 was revised up from 3.00% to 3.25%.

Year-end forecasts for trimmed mean CPI for:

- 2022 was revised up from 6.00% to 6.25%.

- 2023 was left unchanged at 3.75%.

- 2024 was revised up from 3.00% to 3.25%.

Year-end forecasts for unemployment rate for:

- 2022 was revised up from 3.25% to 3.50%.

- 2023 was revised up from 3.50% to 3.75%.

- 2024 was revised up from 4.00% to 4.25%.

{kind=link}

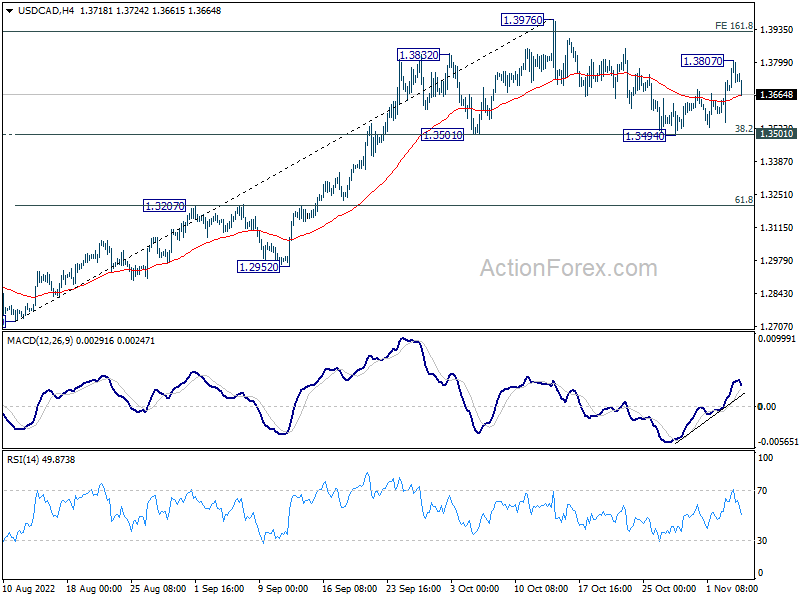

NFP in focus, USD/CAD forming head and shoulder top?

US non-farm payroll employment data is the major focus of the day. Markets are expecting the job market to grow 200k in October. Unemployment rate is expected to tick up from 3.5% to 3.6%.

Looking at related data, ADP report showed solid 239k growth in private employment. ISM manufacturing employment also improved from 48.7 to 50.0. However, ISM services employment dropped notably from 53.0 to contractionary reading of 49.1. Four-week moving average of initial jobless claims rose slightly from 207k to 219k. The set of data overall suggests that job market should remain tight.

As per market reaction, USD/CAD would be an interesting one to watch considering that Canada will also release job data. For now, near term outlook stays bullish for another rise through 1.3976 to resume larger up trend. However, break of 1.3494/3501 support will complete a head and should top pattern (ls: 1.3832; h:1.3976; rs: 1.3807). In the case, deeper correction would likely be seen back to 1.3207 resistance turned support, before USD/CAD find renewed buying.

{kind=link}

Elsewhere

Eurozone will release PMI services final and PPI. UK will release construction PMI. Canada will also release job data and Ivey PMI.

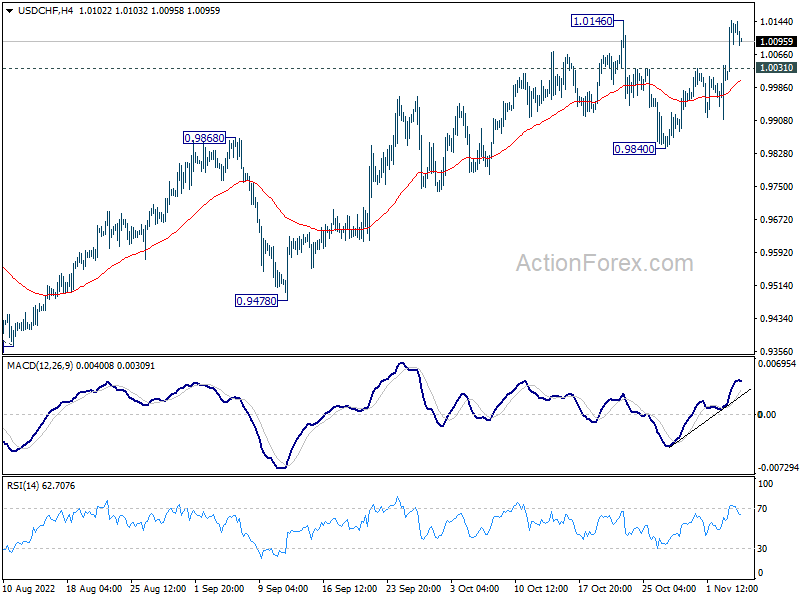

USD/CHF Daily Outlook

Daily Pivots: (S1) 1.0044; (P) 1.0095; (R1) 1.0187; More…

USD/CHF retreats mildly ahead of 1.0146 resistance, but intraday bias stays neutral first. On the upside, firm break of 1.0146 will resume larger up trend. Next target is 1.0283 projection level. On the downside, below 1.0031 minor support will turn intraday bias neutral first. But outlook will stay bullish as long as 0.9840 support holds, in case of retreat.

{kind=link}

In the bigger picture, current development suggests that up trend from 0.8756 (2021 low) is still in progress. Next target is 100% projection of 0.9149 to 1.0063 from 0.9369 at 1.0283, and then 1.0342 (2016 high). For now, this will remain the favored case as long as 0.9779 support holds, even in case of deep pull back.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Construction Index Oct | 43.3 | 46.5 | ||

| 07:00 | EUR | Germany Factory Orders M/M Sep | -0.60% | -2.40% | ||

| 07:45 | EUR | France Industrial Output M/M Sep | -1.00% | 2.40% | ||

| 08:45 | EUR | Italy Services PMI Oct | 48.5 | 48.8 | ||

| 08:50 | EUR | France Services PMI Oct F | 51.3 | 51.3 | ||

| 08:55 | EUR | Germany Services PMI Oct F | 44.9 | 44.9 | ||

| 09:00 | EUR | Eurozone Services PMI Oct F | 48.2 | 48.2 | ||

| 09:30 | GBP | Construction PMI Oct | 52.1 | 52.3 | ||

| 10:00 | EUR | Eurozone PPI M/M Sep | 1.70% | 5.00% | ||

| 10:00 | EUR | Eurozone PPI Y/Y Sep | 42.00% | 43.30% | ||

| 12:30 | USD | Nonfarm Payrolls Oct | 200K | 263K | ||

| 12:30 | USD | Unemployment Rate Oct | 3.60% | 3.50% | ||

| 12:30 | USD | Average Hourly Earnings M/M Oct | 0.30% | 0.30% | ||

| 12:30 | CAD | Net Change in Employment Oct | 11.0K | 21.1K | ||

| 12:30 | CAD | Unemployment Rate Oct | 5.30% | 5.20% | ||

| 14:00 | CAD | Ivey PMI Oct | 60.2 | 59.5 |