Dollar rebounds broadly today as US futures turn south, pointing to a lower open. Yen is back under some selling pressure. But Euro is also weak despite stronger than expected consumer inflation data, while Sterling and Swiss Franc are also soft. Commodity currencies are mixed with Canadian Dollar on the weaker side. But overall, traders are probably just repositioning ahead of RBA, FOMC and BoE rate decisions.

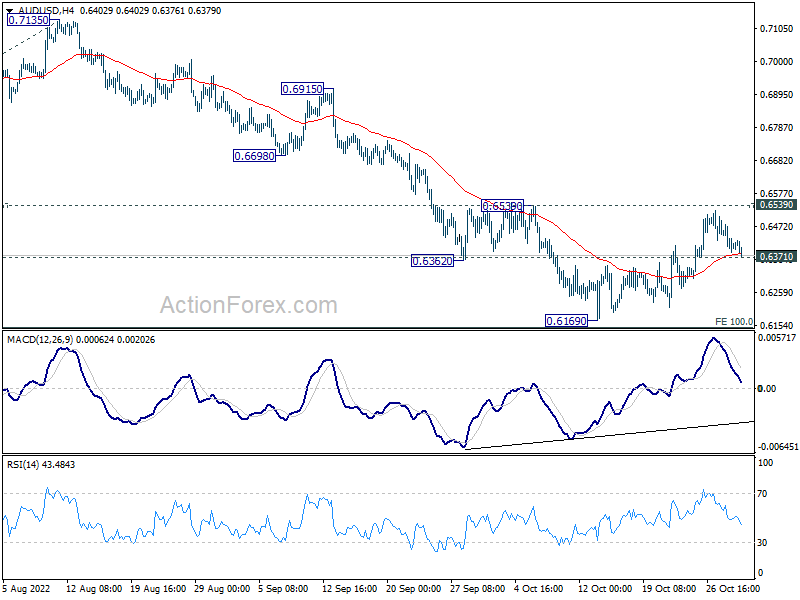

Technically, with Dollar’s rebound, one immediate focus is now on 0.6371 minor support in AUD/USD. Break will indicate that rebound from 0.6169 has completed and bring retest of this low. The move could come as reaction to RBA rate decision, or even before. And, if happens, that could be a pre-signal of more upside in the greenback.

{kind=link}

In Europe, at the time of writing, FTSE is up 0.22%. DAX is up 0.24%. CAC is down -0.16%. Germany 10-year yield is up 0.01 at 2.110. Earlier in Asia, Nikkei rose 1.78%. Hong Kong HSI dropped -1.18%. China shanghai SSE dropped -0.77%. Singapore Strait Times rose 1.11%. Japan 10-year JGB yield rose 0.0027 to 0.245.

ECB Visco: High uncertainty calls for gradual tightening

ECB Governing Council member Ignazio Visco said that interest rate will have to rise further to reduce the risk of persistent high inflation

However, he’s uncertain on the pace of tightening, in face of economic risks. Also, the terminate rate of “can’t be predetermined” due to the uncertain nature of economic forecasting amid Russia’s war in Ukraine.

“The high level of uncertainty calls for a gradual approach, carefully assessing the appropriateness of the monetary stance on the basis of evidence as it becomes available,” he said.

Eurozone GDP growth slowed to 0.2% qoq in Q3

Eurozone GDP grew 0.2% qoq in Q3, slightly above expectation of 0.1% qoq, but much slower than Q2’s 0.8% qoq. EU GDP grew 0.2% qoq too, slowed from Q2’s 0.7% qoq.

Among the Member States for which data are available for the third quarter of 2022, Sweden (+0.7%) recorded the highest increase compared to the previous quarter, followed by Italy (+0.5%), Portugal and Lithuania (both +0.4%). Declines were recorded in Latvia (-1.7%) as well as in Austria and Belgium (both -0.1%). The year-on-year growth rates were positive for all countries except for Latvia (-0.4%).

Eurozone CPI rose to 10.7% yoy in Oct, core CPI up to 5.0% yoy

Eurozone CPI accelerated from 9.9% yoy to 10.7% yoy in October, above expectation of 9.9% yoy. CPI core (all-items ex energy, food, alcohol & tobacco also rose from 4.8% yoy to 5.0% yoy, above expectation of 4.8% yoy.

Looking at the main components, energy is expected to have the highest annual rate in October (41.9%, compared with 40.7% in September), followed by food, alcohol & tobacco (13.1%, compared with 11.8% in September), non-energy industrial goods (6.0%, compared with 5.5% in September) and services (4.4%, compared with 4.3% in September).

Japan industrial production dropped -1.6% mom, as auto-related production dived

Japan industrial production declined -1.6% mom in September, below expectation of -1.0% mom. That’s also the first contract in four months. The fall was driven by -12.4% mom decline in auto-related production, the steepest fall in eight months.

Manufacturers surveyed by the Ministry of Economy, Trade and Industry (METI) expected output to fall another -0.4% in October and then rise 0.8% in November.

Retail sales rose 4.5% yoy in September, above expectation of 4.1% yoy. Housing starts rose 1.0% yoy, below expectation of 2.3% yoy.

In October, consumer confidence dropped from 30.8 to 29.9, below expectation of 31.5.

Australia retail sales rose 0.6% mom in Sep

Australia retail sales rose 0.6% mom in September, matched expectations.

Ben Dorber, ABS head of retail statistics said, “This month’s rise was again driven by the combined strength in the food industries. Food retailing rose 1.0 per cent, while cafes, restaurants, and takeaway food services rose 1.3 per cent.

“Many retailers remained open for the National Day of Mourning, an additional one-off public holiday in September, and this boosted spending on food, alcohol and dining out.”

China PMI manufacturing and services fell to contraction

China PMI Manufacturing fell from 50.1 to 49.2 in October, below expectation of 50.0.

PMI Non-Manufacturing dropped from 50.6 to 48.7, below expectation of 50.2. Both readings were below 50-mark which separates growth from contraction on a monthly basis.

“In October, affected by the spread of the pandemic and other factors within the country, China’s PMI fell, with the manufacturing PMI, non-manufacturing PMI and comprehensive PMI standing at 49.2 per cent, 48.7 per cent and 49.0 per cent, respectively, and the foundation of China’s economic recovery needs to be further consolidated,” said senior NBS statistician Zhao Qinghe.

“In October, the composite PMI stood at 49.0 per cent, down 1.9 percentage points from the previous month, falling below the critical point, indicating a general slowdown in the production and operating activities of Chinese enterprises.”

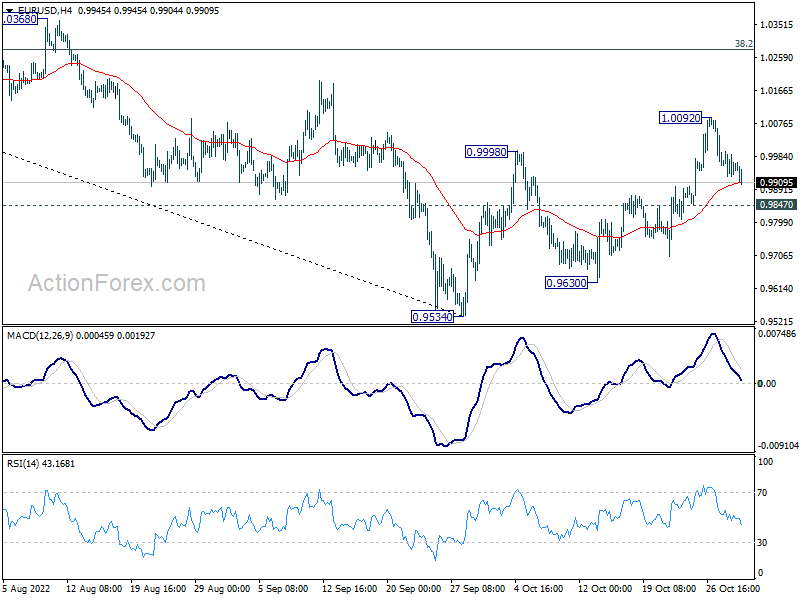

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 0.9930; (P) 0.9964; (R1) 1.0001; More…

Intraday bias in EUR/USD remains neutral for the moment. Further rise is in favor as long as 0.9847 minor support holds. Break of 1.0092 will target 38.2% retracement of 1.1494 to 0.9534 at 1.0283. However, break of 0.9847 will turn bias back to the downside for 0.9534/9630 support zone instead.

{kind=link}

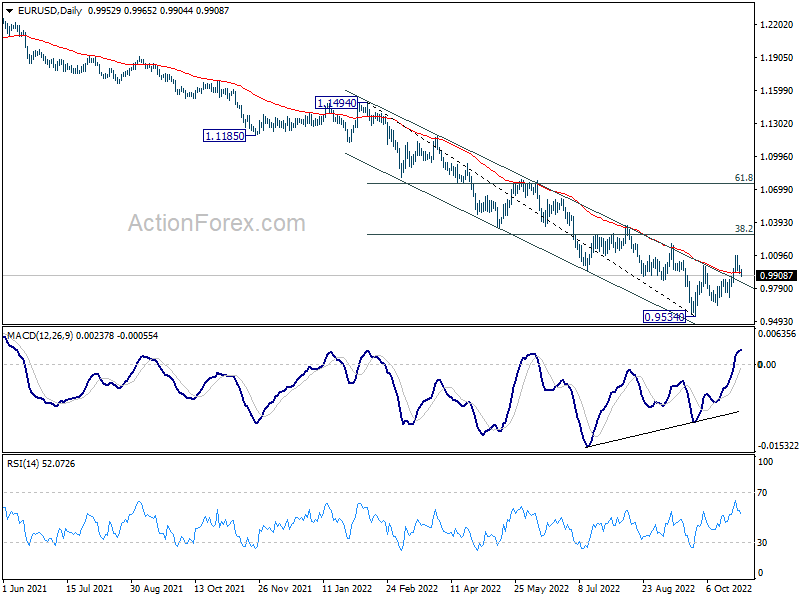

In the bigger picture, the case of medium term bottoming at 0.9534 building up, with bullish convergence condition in daily MACD. While it is too early to call for trend reversal, firm break of 0.9998 opens up stronger rebound back to 55 week EMA (now at 1.0630) even as a corrective rise. However, sustained trading back below 55 day EMA (now at 0.9938) will revive medium term bearishness for another fall through 0.9534 low.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Industrial Production M/M Sep P | -1.60% | -1.00% | 3.40% | |

| 23:50 | JPY | Retail Trade Y/Y Sep | 4.50% | 4.10% | 4.10% | |

| 00:00 | AUD | TD Securities Inflation M/M Oct | 0.40% | 0.50% | ||

| 00:30 | AUD | Private Sector Credit M/M Sep | 0.70% | 0.80% | 0.80% | |

| 00:30 | AUD | Retail Sales M/M Sep | 0.60% | 0.60% | 0.60% | |

| 01:00 | CNY | Manufacturing PMI Oct | 49.2 | 50 | 50.1 | |

| 01:00 | CNY | Non-Manufacturing PMI Oct | 48.7 | 50.2 | 50.6 | |

| 05:00 | JPY | Consumer Confidence Oct | 29.9 | 31.5 | 30.8 | |

| 05:00 | JPY | Housing Starts Y/Y Sep | 1.00% | 2.30% | 4.60% | |

| 07:00 | EUR | Germany Retail Sales M/M Sep | 0.90% | -0.50% | -1.30% | -1.40% |

| 07:30 | CHF | Real Retail Sales Y/Y Sep | 3.20% | 3.30% | 3.00% | |

| 09:00 | EUR | Italy GDP Q/Q Q3 P | 0.50% | -0.10% | 1.10% | |

| 09:30 | GBP | M4 Money Supply M/M Sep | 2.10% | 0.10% | -0.20% | -0.10% |

| 09:30 | GBP | Mortgage Approvals Sep | 67K | 66K | 74K | |

| 10:00 | EUR | Eurozone GDP Q/Q Q3 P | 0.20% | 0.10% | 0.80% | |

| 10:00 | EUR | Eurozone CPI Y/Y Oct P | 10.70% | 9.90% | 10.00% | 9.90% |

| 10:00 | EUR | Eurozone CPI Core Y/Y Oct P | 5.00% | 4.80% | 4.80% | |

| 13:45 | USD | Chicago PMI Oct | 47.1 | 45.7 |