Dollar traded with an undertone in Asian session together with Yen and Swiss Franc. The pull back in US stocks overnight turned out to be shallow and brief. Major indexes managed to pare back much of earlier losses to close just slightly lower. Investors seemed to be just cautious ahead of Friday’s job report. Meanwhile, commodity currencies are strengthening in Asian session, while Euro and Sterling are mixed.

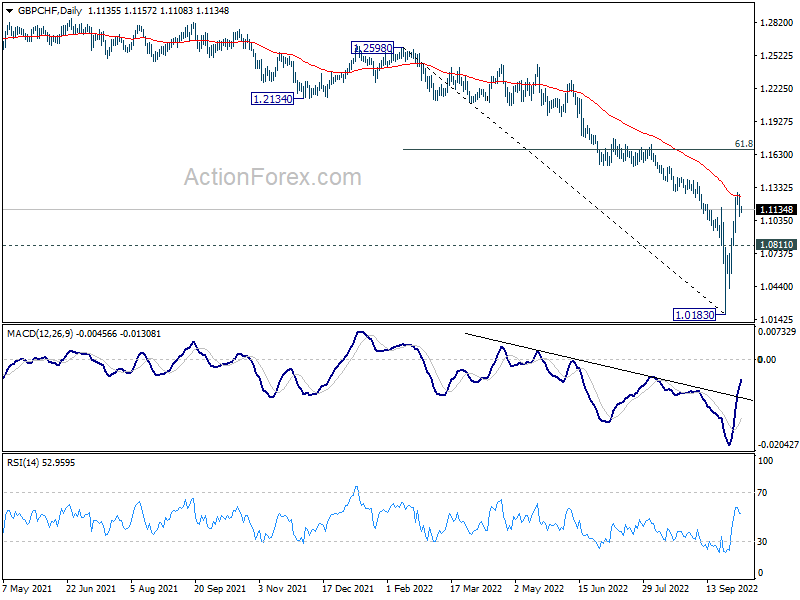

Technically, in addition to Dollar’s next move, development in Sterling is also worth a note. After two volatile weeks, both EUR/GBP and GBP/CHF are now pressing 55 day EMA (from opposite sides of course). The Pound appears to be finding it difficult to break through the EMAs decisively. Rejection from there could prompt sellers to come back and push it back towards the near term spike low. As for GBP/CHF, break of 1.0811 minor support will argue that rebound from 1.0183 has completed, and bring deeper fall back towards there.

{kind=link}

In Asia, at the time of writing, Nikkei is up 1.01%. Hong Kong HSI is down -0.17%. Singapore Strait Times is up 0.32%. Japan 10-year JGB yield is up 0.004 at 0.254. Overnight, DOW dropped -0.14%. S&P 500 dropped -0.20%. NASDAQ dropped -0.25%. 10-year yield rose 0.142 to 3.759

Fed Bostic: Lowering rates in 2023? Not so fast

Atlanta Fed president Raphael Bostic said yesterday, “I would like to reach a point where policy is moderately restrictive –between 4 and 4 1/2 percent by the end of this year — and then hold at that level and see how the economy and prices react,”

There is “considerable speculation already that the Fed could begin lowering rates in 2023 if economic activity slows and the rate of inflation starts to fall,” Bostic said. “I would say: not so fast.”

“We should not let the emergence of (economic) weakness deter our push to lower inflation,” he added. “We must remain vigilant because this inflation battle is likely still in early days.”

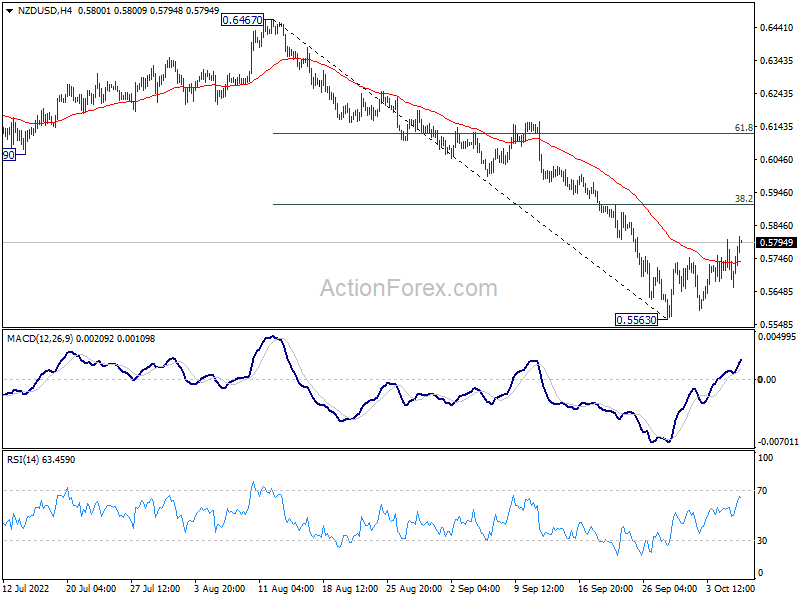

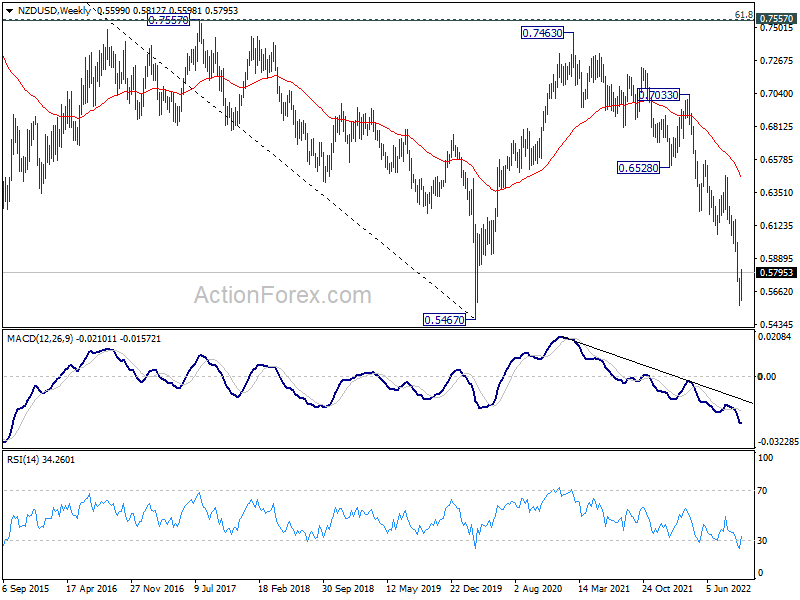

NZ Robertson not concerned with NZD outlook, NZD/USD extending recovery

New Zealand Deputy Prime Minister Grant Robertson said today that it’s going to be a “challenging year” with “global slowdown”. New Zealand would see “less demand and some slowdown”. But, “that doesn’t mean, to me, a recession. There is balance to struck here.”

“Monetary and fiscal policies need to be coordinated, to work together,” he said. “As interest rates rise they’ll restrict demand.” He also said that he’s “not concerned on the long-term outlook for the New Zealand dollar.”

NZD/USD is extending the recovery from 0.5563, but after all, that’s seen as a corrective move in a down trend. Upside should be limited by 38.2% retracement of 0.6467 to 0.5563 at 0.5908. Larger down trend is still expected to resume at a later stage to 2020 low at 0.5467.

{kind=link}

{kind=link}

On the data front

Australia AiG performance of construction dropped from 47.9 to 46.5 in September. Goods and services trade surplus narrowed from AUD 8.97B to AUD 8.32B in August, below expectation of AUD 10.0B.

Looking ahead, Germany factor orders, UK PMI construction, Eurozone retail sales, and ECB meeting accounts will be featured in European session. US Challenger job cuts, jobless claims and Ivey PMI will be released later in the day.

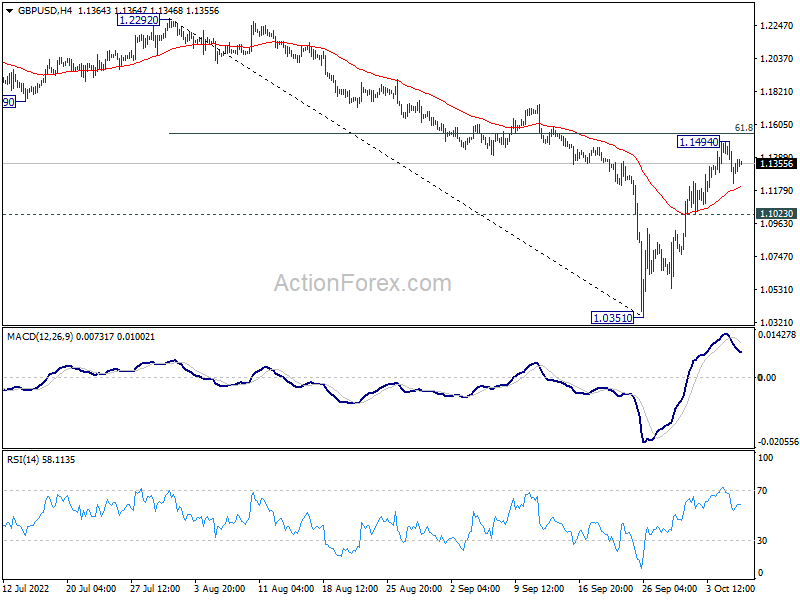

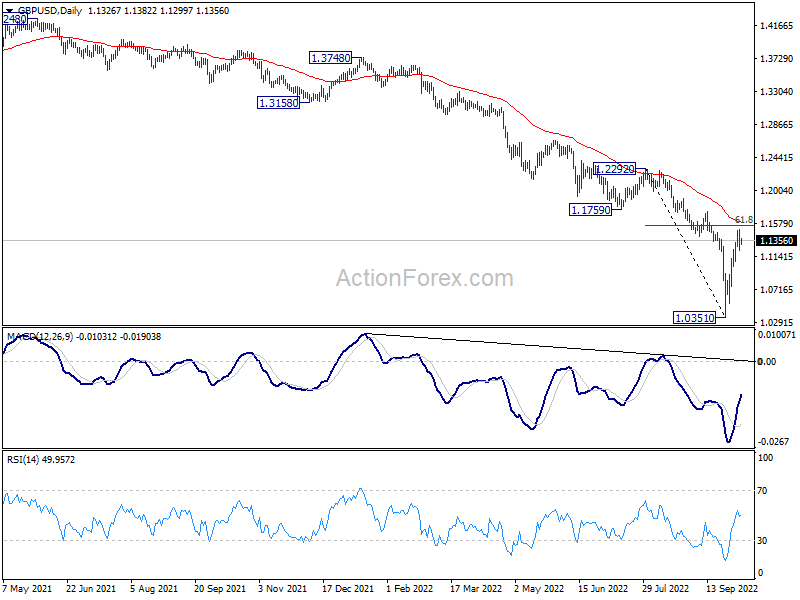

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.1206; (P) 1.1350; (R1) 1.1473; More…

Intraday bias in GBP/USD remains neutral for the moment. On the downside, break of 1.1023 minor support will indicate that rebound from 1.0351 is over. Intraday bias will be back on the downside for retesting 1.0351. On the upside, firm break of 61.8% retracement of 1.2292 to 1.0351 at 1.1551 will pave the way to 1.2292 resistance.

{kind=link}

In the bigger picture, fall from 1.4248 (2018 high) is resuming long term down trend from 2.1161 (2007 high). Next target is 100% projection of 2.1161 to 1.3503 from 1.7190 at 0.9532. There is no scope of a medium term rebound as long as 1.1759 support turned resistance holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Construction Index Sep | 46.5 | 47.9 | ||

| 00:30 | AUD | Trade Balance (AUD) Aug | 8.32B | 10.00B | 8.73B | 8.97B |

| 06:00 | EUR | Germany Factory Orders M/M Aug | -0.50% | -1.10% | ||

| 08:30 | GBP | Construction PMI Sep | 48.1 | 49.2 | ||

| 09:00 | EUR | Eurozone Retail Sales M/M Aug | -0.30% | 0.30% | ||

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 11:30 | USD | Challenger Job Cuts Y/Y Sep | 30.30% | |||

| 12:30 | USD | Initial Jobless Claims (Sep 30) | 205K | 193K | ||

| 14:00 | CAD | Ivey PMI Sep | 62.3 | 60.9 | ||

| 14:30 | USD | Natural Gas Storage | 125B | 103B |