Sterling’s rebound extended further overnight as sentiment towards it continued to stabilized. Indeed, the Pound is trading up against Aussie and Canadian for the month. Sterling looks set to have a strong close for the week too. Commodity currencies are generally pressured today, together with steep decline in Japan Nikkei. But there is little risk aversion support to Yen. Dollar is mixed for now, overwhelmed by the comeback of Euro too.

Technically, GBP/CAD is now pressing an important cluster resistance. The levels include 1.5296 resistance, 55 day EMA (now at 1.5292), and 38.2% retracement of 1.7375 to 1.4069 at 1.5332. Rejection by this cluster resistance, followed by break of 1.4728 minor support, will argue that the rebound from 1.4069 has completed. That will also maintain medium term bearishness for down trend resumption through 1.4069 at a later stage. However, sustained break of this cluster should add to the case that the worst is over for the Pound, and open up stronger rise back to 61.8% retracement at 1.6112. We’ll probably find out which way next week.

{kind=link}

In Asia, at the time of writing, Nikkei is down -2.26%. Hong Kong HSI is down -0.25%. China Shanghai SSE is down -0.32%. Singapore Strait Times is down -0.43%. Japan 10-year JGB yield is down -0.014 at 0.245. Overnight, DOW dropped -1.54%. S&P 500 dropped -2.11%. NASDAQ dropped -2.84%. 10-year yield rose 0.042 to 3.747.

BoE Pill: A significant and necessary monetary policy response in November

BoE Chief Economist Huw Pill said in a speech, “on the basis of the fiscal easing announced last week, the macroeconomic policy environment looks set to rebalance. Taken in conjunction with the macroeconomic impact of ensuing market developments, it is hard to avoid the conclusion that the fiscal easing announced last week will prompt a significant and necessary monetary policy response in November.”

The MPC forecasts will be the “vehicle” for making ” necessarily comprehensive assessment” on recent developments. The assessments will “embody recent evidence of weakness in economic activity, as well as the impact of the Government’s Energy Price Guarantee on headline inflation and wage and price setting behaviour.” They will factor in “the evolution of international commodity prices, not least developments in wholesale natural gas markets” and “impact of the Government’s Growth Plan and other fiscal announcements in detail.”

As for the gilt interventions announced by BoE this week, Pill emphasized it’s a “temporary and targeted financial stability operation”. It was “not a monetary policy operation”.

Fed Daly: Going to take restrictive policy at least through next year

San Francisco Fed President Mary Daly said yesterday she’s “quite comfortable” with the economic projections that interest rate will rise to 4-4.5% by the end of this year, and 4.5-5% next.

“It’s going to take restrictive policy for a duration of time to get clear and convincing evidence that inflation is getting back to 2% — so from my mind, that’s at least through next year,” she added.

“If inflation continues to print very high and we get no easing of inflation and only modest easing of labor markets, then that’s basically an economy that’s still got a lot of momentum, and inflation is still too high — we’re going to have to keep moving up because we are going to understand that the terminal rate isn’t as close as it would be,” she said.

Japan industrial production rose 2.7% mom in Aug, to grow further in Sep and Oct

Japan industrial production rose 2.7% mom in August, much better than expectation of -0.2% decline. That’s also the third consecutive month of growth. The Ministry of Economy, Trade and Industry expects production to rise further by 2.9% mom in September and then 3.2% mom in October.

Retail sales rose 4.1% yoy in August, well above expectation of 2.8% yoy. Unemployment rate dropped from 2.6% to 2.5%, matched expectations. Housing starts rose 4.6% yoy in August, versus expectation of -4.1% yoy. Consumer confidence index dropped from 32.5 to 30.8, below expectation of 33.6.

China PMI manufacturing rose to 50.1, but Caixin PMI manufacturing dropped to 48.1

China’s official PMI Manufacturing rose from 49.4 to 50.1 in September, above expectation of 49.2. PMI Non-Manufacturing dropped from 52.6 to 50.6, below expectation of 52.0.

Senior NBS statistician Zhao Qinghe said, “In September, with a series of stimulus packages continuing to take effect, coupled with the impact of hot weather receding, the manufacturing boom has rebounded. The PMI returned to the expansionary range… [The non-manufacturing index] remained above the threshold, with the overall expansion of the non-manufacturing sector decelerating.”

On the other hand, Caixin PMI Manufacturing dropped from 49.5 to 48.1, below expectation of 49.9. Caixin said production fell for the first time in four months amid quicker dropped in sales. Firms cut back on purchasing activity and inventories. Selling prices fell at quickest rate since December 2015.

Looking ahead

UK Q2 GDP final, current account, and mortgage approvals will be released in European session. Also featured include Swiss retail sales and KOF economic barometer, France consumer spending, Germany unemployment, Eurozone unemployment and CPI flash.

later in the day, US personal income and spending, with PCE price index will be released, as well as Chicago PMI.

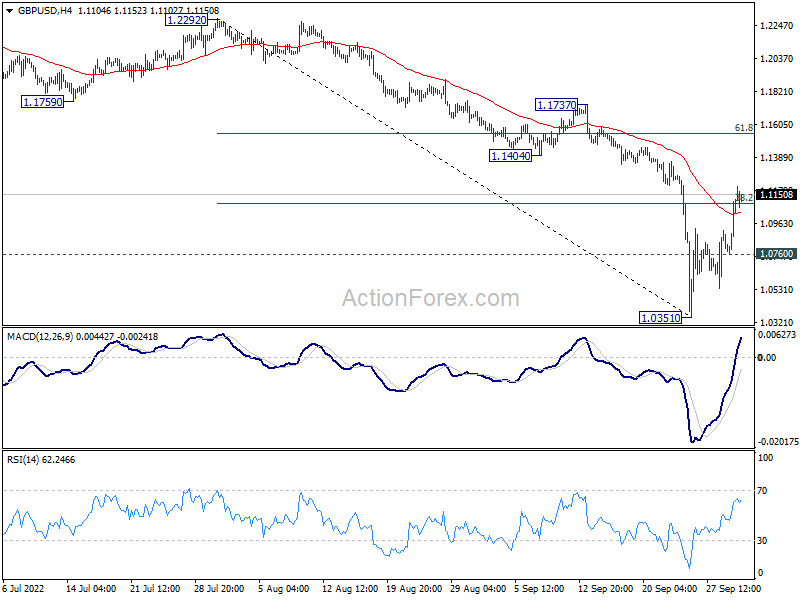

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.0881; (P) 1.1000; (R1) 1.1238; More…

GBP/USD’s rebound from 1.0351 extended higher today and the break of 4 hour 55 EMA (now at 1.1037) is a positive sign. For now, intraday bias is mildly on the upside for further rise to 61.8% retracement of 1.2292 to 1.0351 at 1.1551. On the downside, break of 1.0760 minor support will indicate that the rebound is over, and bring retest of 1.0351 low.

{kind=link}

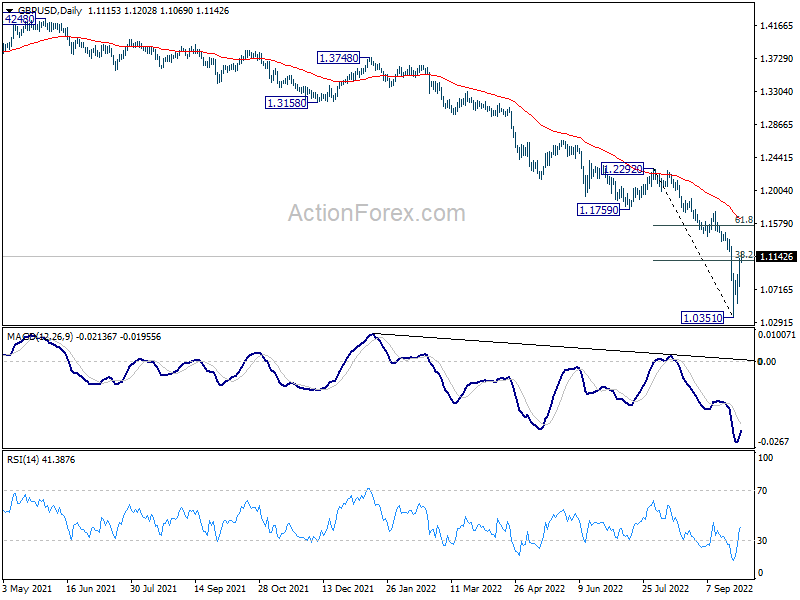

In the bigger picture, fall from 1.4248 (2018 high) is resuming long term down trend from 2.1161 (2007 high). Next target is 100% projection of 2.1161 to 1.3503 from 1.7190 at 0.9532. There is no scope of a medium term rebound as long as 1.1759 support turned resistance holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Aug | -1.60% | 5.00% | 4.90% | |

| 23:30 | JPY | Unemployment Rate Aug | 2.50% | 2.50% | 2.60% | |

| 23:50 | JPY | Industrial Production M/M Aug P | 2.70% | -0.20% | 0.80% | |

| 23:50 | JPY | Retail Trade Y/Y Aug | 4.10% | 2.80% | 2.40% | |

| 01:30 | AUD | Private Sector Credit M/M Aug | 0.80% | 0.80% | 0.70% | 0.80% |

| 01:30 | CNY | NBS Manufacturing PMI Sep | 50.1 | 49.2 | 49.4 | |

| 01:30 | CNY | Non-Manufacturing PMI Sep | 50.6 | 52 | 52.6 | |

| 01:45 | CNY | Caixin Manufacturing PMI Sep | 48.1 | 49.9 | 49.5 | |

| 05:00 | JPY | Housing Starts Y/Y Aug | 4.60% | -4.10% | -5.40% | |

| 05:00 | JPY | Consumer Confidence Index Sep | 30.8 | 33.6 | 32.5 | |

| 06:00 | GBP | GDP Q/Q Q2 F | -0.10% | -0.10% | ||

| 06:00 | GBP | Current Account (GBP) Q2 | -43.9B | -51.7B | ||

| 06:30 | CHF | Real Retail Sales Y/Y Aug | 2.80% | 2.60% | ||

| 06:45 | EUR | France Consumer Spending M/M Aug | 0.00% | -0.80% | ||

| 07:00 | CHF | KOF Leading Indicator Sep | 86.2 | 86.5 | ||

| 07:55 | EUR | Germany Unemployment Change Sep | 20K | 28K | ||

| 07:55 | EUR | Germany Unemployment Rate Sep | 5.50% | 5.50% | ||

| 08:00 | EUR | Italy Unemployment Aug | 7.90% | 7.90% | ||

| 08:30 | GBP | Mortgage Approvals Aug | 63K | 64K | ||

| 08:30 | GBP | M4 Money Supply M/M Aug | 0.50% | 0.50% | ||

| 09:00 | EUR | Eurozone Unemployment Rate Aug | 6.60% | 6.60% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Sep P | 9.10% | 9.10% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Sep P | 4.70% | 4.30% | ||

| 12:30 | USD | Personal Income M/M Aug | 0.30% | 0.20% | ||

| 12:30 | USD | Personal Spending Aug | 0.20% | 0.10% | ||

| 12:30 | USD | PCE Price Index M/M Aug | 0.30% | -0.10% | ||

| 12:30 | USD | PCE Price Index Y/Y Aug | 6.60% | 6.30% | ||

| 12:30 | USD | Core PCE Price Index M/M Aug | 0.10% | |||

| 12:30 | USD | Core PCE Price Index Y/Y Aug | 5.20% | 4.60% | ||

| 13:45 | USD | Chicago PMI Sep | 51.9 | 52.2 | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Sep F | 59.5 | 59.5 |