The currency markets have turned into consolidation mode temporarily. Sterling further stabilized after BoE said in a statement that the assessment of the government’s growth plan will be done at next “scheduled” meeting, ruling out an emergency meeting. Dollar is also taking a breather even though 10-year yield rose to the highest level since 2010. Yen is steady, awaiting traders to test Japan’s determination on intervention again.

Technically, while the currency markets turned steady, Gold is extending recent down trend. It now seems that 55 month EMA (now at 1651.12) couldn’t provide enough support for a bounce. Outlook will stay bearish as long as 1687.82 resistance holds. Next near term target is 61.8% projection of 2070.06 to 1680.83 from 1807.66 1567.11. Decisive break there could prompt downside acceleration to 100% projection at 1418.43. That could happen if US 10-year yield breaks through 4% handle firmly.

{kind=link}

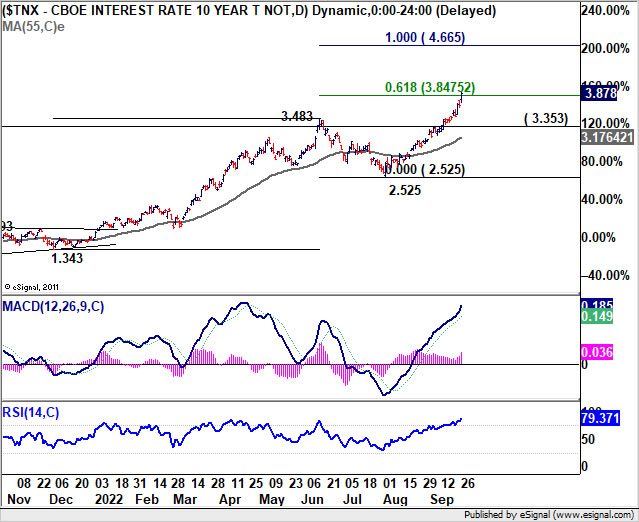

In Asia, at the time of writing, Nikkei is up 0.45%. Hong Kong HSI is down -1.06%. China Shanghai SSE is up 0.26%. Singapore Strait Times is down -0.57%. Japan 10-year JGB yield is up 0.0003 at 0.253. Overnight, DOW dropped -1.11%. S&P 500 dropped -1.03%. NASDAQ dropped -0.60%. 10-year yield rose 0.181 to 3.878.

{kind=link}

Fed Mester: Monetary policy needs to be in a restrictive stance

Cleveland Fed President Loretta Mester said yesterday, “when there is uncertainty, it can be better for policymakers to act more aggressively because aggressive and pre-emptive action can prevent the worst-case outcomes from actually coming about.”

“Further increases in our policy rate will be needed,” Mester said. “In order to put inflation on a sustained downward trajectory to 2%, monetary policy will need to be in a restrictive stance, with real interest rates moving into positive territory and remaining there for some time.”

“There will be some pain and bumps along the way as the growth in output and employment slow and the unemployment rate moves up,” Mester said. “But the current persistent high inflation is also very painful for many households and businesses.”

Fed Bostic: UK growth plan adds uncertainty to the economy

Atlanta Fed President Raphael Bostic said market reaction to UK government’s new growth plan, with sharp volatility in Sterling, was a “real concern”. There’s “a fear that the new actions will add uncertainty to the economy.”

The key question will be what does this mean for ultimately weakening the European economy, which is an important consideration for how the U.S. economy is going to perform,” he added.

But for now, Bostic gave no indication on how Fed could respond to the development in the UK. “The more important thing is that we need to get inflation under control,” he said. “Until that happens, we’re going to see I think a lot of volatility in the marketplace in all directions.”

SNB Maechler: More signs that price increases are spreading

SNB board member Andrea Maechler said yesterday, “We have tightened monetary policy and raised interest rates to send a clear signal that we will do everything to bring down inflation over time.”

“There are ever more signs that price increases are spreading to goods and services which have not been affected so far,” she said. “We are acting to make sure that inflation does not become entrenched.”

On the question of further rate hike, she said, “I never speak of interest rate expectations. I can only say what the market expects, and it expects the SNB and other central banks to further increase their rates.”

RBNZ Orr said tightening cycle very mature, AUD/NZD topping soon?

RBNZ Governor Adrian Orr today, “We believe we still have some work to do, but the good news is because we’ve done so much already, the tightening cycle is very mature, it’s well advanced.”

There’s s “a little bit more to do before we can drop to our normal happy place, which is to watch, worry and wait for signs of inflation up or down,” he said.

AUD/NZD’s rally picks up some momentum recently on expectations that RBA is catching up with RBNZ on tightening. However, the cross is now pressing medium term channel resistance, and in proximity to 61.8% projection of 1.0314 to 1.1168 from 1.0987 at 1.1515. Overbought condition could finally limit upside. Break of 1.1303 will argue that it has turned into a corrective phase.

Nevertheless, firm break of 1.1515 could prompt further upside acceleration to 100% projection at 1.1841.

{kind=link}

World Bank cut China growth forecasts to 2.8% in 2022

For 2022, the World Bank downgraded China’s growth forecasts sharply from 5.0% (April’s) to just 2.8%. On the other hand, ASEAN-5 growth forecasts was upgraded from 4.9% to 5.4%. East Asia & Pacific (excluding China) growth was upgraded from 4.8% to 5.3%. However, East Asia & Pacific as a whole was down graded from 5.0% to 3.2%,

The World Bank said in the release: “Growth in much of East Asia and the Pacific has been driven by recovery in domestic demand, enabled by a relaxation of COVID-related restrictions, and growth in exports. China, which constitutes around 86% of the region’s output, uses targeted public health measures to contain outbreaks of the virus, inhibiting economic activity.”

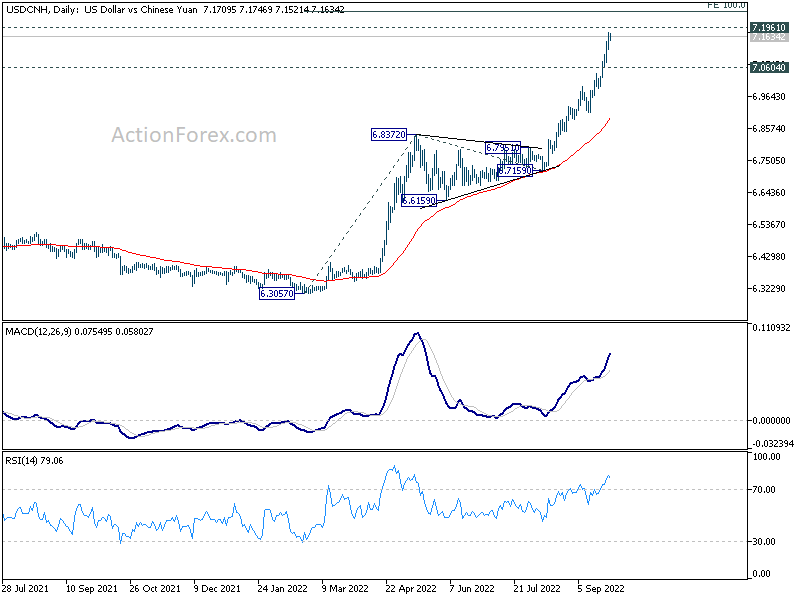

Selloff in Yuan is still in force, with USD/CNH approaching 2020 high at 7.1961. There is so far no clear support for the Yuan at 7 psychological level. Break of 7.1961 will mark the highest level for the pair, lowest for offshore Yuan, since 2008. Technically, USD/CNH might top only after hitting 100% projection of 6.3057 to 6.8372 from 6.7159 at 7.2474.

{kind=link}

On the data front

Japan corporate service price index rose 1.9% yoy in August, below expectation of 2.2% yoy. Eurozone will release M3 money supply today. US will release durable goods orders, house price index, consumer confidence and new home sales.

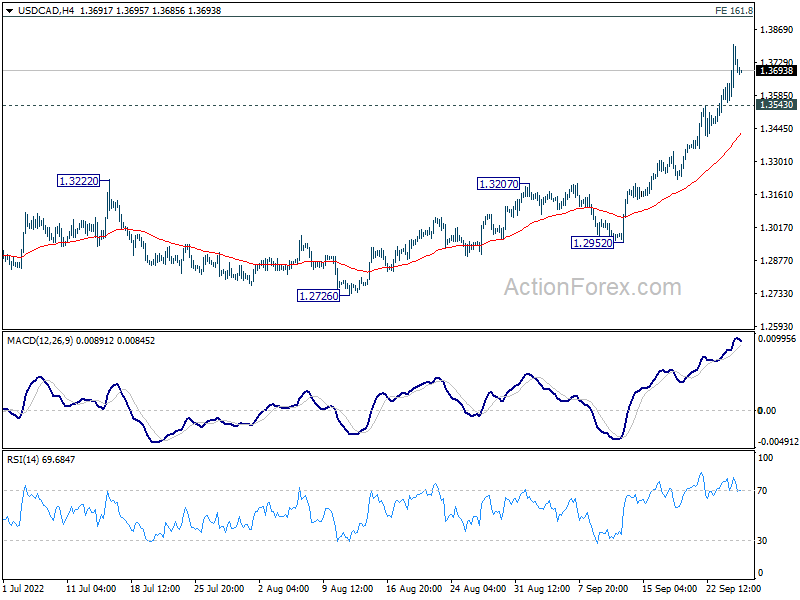

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3596; (P) 1.3703; (R1) 1.3845; More…

USD/CAD’s rally continued and hit as high as 1.3807 so far. Intraday bias stays on the upside for 161.8% projection of 1.2005 to 1.2947 from 1.2401 at 1.3925. Firm break there will target 200% projection at 1.4285. On the downside, below 1.3543 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

{kind=link}

In the bigger picture, up trend from 1.2005 (2021 low) is still in progress. 61.8% retracement of 1.4667 to 1.2005 (2021 low) at 1.3650 is already met. Next target is 1.4667 (2020 high). This will now remain the favored case as long as 1.3222 resistance turned support holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Aug | 1.90% | 2.20% | 2.10% | 2.00% |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Aug | 5.50% | 5.50% | ||

| 12:30 | USD | Durable Goods Orders Aug | -0.10% | -0.10% | ||

| 12:30 | USD | Durable Goods Orders ex Transportation Aug | 0.30% | 0.20% | ||

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Jul | 16.90% | 18.60% | ||

| 13:00 | USD | Housing Price Index M/M Jul | 0.00% | 0.10% | ||

| 14:00 | USD | Consumer Confidence Sep | 104.5 | 103.2 | ||

| 14:00 | USD | New Home Sales Aug | 500K | 511K |